|

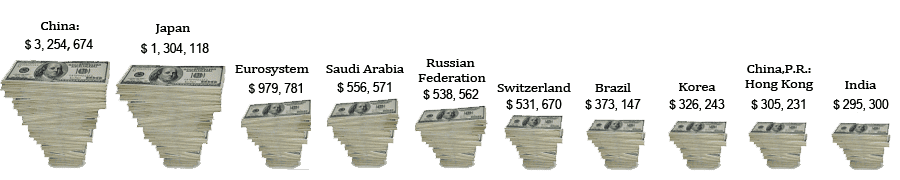

International reserves are a country’s “external assets”—including foreign currency deposits and bonds held by central banks and monetary authorities, gold and SDRs. The top 10 holders of international reserves account for nearly two-thirds of the world’s total foreign currency reserves. China, with US$3.3 trillion at the end of 2011, tops the list. Twenty years ago it had only US$18 billion, and ten years ago US$146 billion. Second is Japan with US$1.3 trillion (as of December 2012.) They are the only two countries with reserves above US$1trillion. |

|

Top Ten Countries with the Largest International Reserves (in US$ Millions)

|

|

International Reserves of Countries Worldwide (in US$ Millions)

Darker red: higher reserves |

|

Full Chart:

Note/1: See footnotes on the Official Reserve Assets and the Other Foreign Currency Assets topic views. |

|

The foreign currency portion of international reserves (IRs) is held in “reserve currencies”—mostly US dollars, but also euros, UK pounds and Japanese yen. SDRs (“special drawing rights”) are international reserve assets created by the International Monetary Fund (IMF), which member countries can add to their foreign currency reserves and gold reserves to use for payments requiring foreign exchange. The SDR’s value is set daily using a basket of four major currencies: the euro, Japanese yen, pound sterling and US dollar. Making Sense of SDRs

Ample IRs allow a government to manipulate exchange rates—usually to stabilize rates and provide a more favorable economic environment or to purchase its domestic currency to protect the country from an attack by speculators. IRs are also an important indicator of a country’s ability to repay foreign debt and are a factor in determining a country’s credit rating. In fact, the fragile global recovery in 2012, says the World Bank, and related decreasing exports by developing countries, forced some of them to dip into their international reserves to support their currencies. In general, it is believed that reserves are “adequate” if they can cover approximately three months of a country’s imports or all of the external debt maturing over the coming year. According to the same World Bank report, “the proportion of crude oil and industrial commodities exporters where international reserves were less than the critical three months of imports rose from 6.3 percent to 9.4 percent between January 2011 and September 2012 and the share of countries with less than five months of import cover rose from 12.5 percent to 25 percent. But in the group of non-oil noncommodities dependent countries, the share of countries with less than three months of import cover rose from 14 percent to 25 percent in the same period, and those with less than five months of import cover rose from 44.4 percent of the total to 58.3 percent.” Very high reserves, while assuring in the recent financial downturn, can also have negative implications for the holder of the reserves and for the global monetary system. For one thing, by investing heavily in foreign reserves, a country invests less in its own economy—possibly spending less on education, healthcare and infrastructure—which may have otherwise offered a route to longer-term growth. For another, with most reserves held in US dollars, a stronger US dollar has been supported despite high current account deficits in the US, contributing to global economic imbalances. |