Middle Eastern banks are looking for merger and acquisition opportunities to help them bolster their balance sheets and expand into new product areas and markets.

In response to lower oil prices, governments throughout the Middle East are addressing fiscal shortfalls by cutting back on expenditures. As a result, consumer sentiment has suffered, and business growth has fallen, which is impacting growth rates for banks in the region. Net profit for banks in the region is estimated to have declined by around 3% last year.

Given the increased risk environment for credit and financing due to lowereconomic growth, banks are more circumspect in their business activities. Indeed, much of the reduced net profit in 2016 was due to increased loan-loss provisions on impairments. Most banks in the region are budgeting for only single-digit growth in 2017. Loan defaults have risen in some Middle East markets, particularly in the consumer and the small and mid-size business areas. However, banks’ nonperforming-loans ratios for the region generally are low and are backed by very high provisioning, particularly in Gulf Cooperation Council banking sectors.

Tightening bank liquidity has been a key theme in the region’s banking sector since the onset of low crude oil prices. Moreover, governments in most of the regional markets have attempted to boost economic and investment activity through large-scale infrastructure projects, which have reduced government deposits at banks.

The deposit market is very competitive throughout the Middle East (particularly so in more-developed markets such as the UAE and Saudi Arabia). At the same time as liquidity buffers have fallen, funding costs have risen through higher cost retail and corporate deposits and wholesale funding, thereby impacting banks’ bottom lines. If liquidity continues to be an issue for Middle East markets in 2017, then this will likely have an impact on both private-sector consumer credit and small and mid-size companies’ credit growth.

HIGH-GROWTH MARKETS

Liquidity conditions improved slightly in the latter part of 2016, partly due to an uptick in oil prices and regional governments’ debt issuances ($9 billion for Qatar in late May and $17.5 billion for Saudi Arabia in October). It is notable that even with the challenging conditions last year, both government and private bond as well as sukuk (Islamic bond) issuances from the region attracted considerable investor interest and were oversubscribed. It was a good year overall for debt issuance from the region in 2016; and this trend may continue, especially if the region’s large sovereigns bring to market possible Islamic tranches.

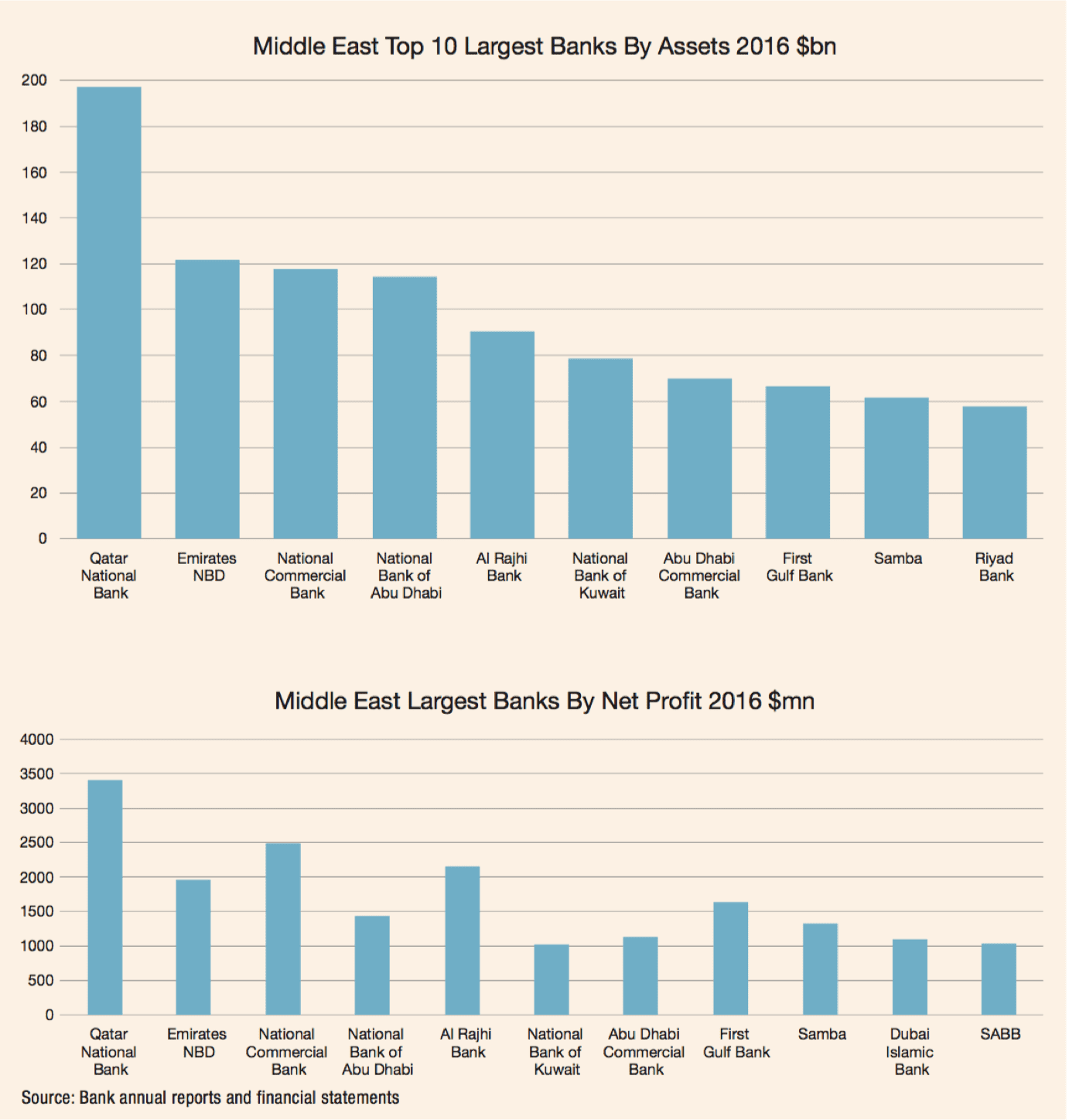

Lower growth in the region, tighter margins and reduced liquidity have resulted in increased bank consolidation. Moreover, the increased regulatory burden for banks is also a catalyst for consolidation. Although the region’s population is young and growing quickly, the size of most markets is quite small. The opportunities for meaningful organic growth are therefore limited. This is one of the main reasons why leading banks in the region, such as Qatar National Bank and Kuwait Finance House, have been looking for both regional and international opportunities.

In 2016, QNB completed the acquisition of Turkey’s Finansbank, the fifth-largest privately owned bank in Turkey. QNB paid $3 billion in cash for Finansbank. “This transaction is a breakthrough in QNB’s vision to becoming a Middle East and Africa icon by 2017,” stated QNB’s CEO, Ali Ahmed Al Kuwari. “Our strategy is to focus on high-growth markets where we see a competitive advantage. Turkey, with its significant market size, population, growth track record, strong economic and banking sector and strategic location as a gateway between Europe, Asia and Africa, represents such a market.”

The Finansbank transaction follows QNB’s acquisition of a stake in pan–African bank Ecobank International in 2014 and its $2 billion purchase of Societe Generale’s Egyptian business in 2013. QNB has probably the greatest asset base outside its relatively small home market and is aiming to become a leading global bank by 2030. It has banking operations in more than 30 countries, including UAE, Iraq, Tunisia and Jordan.

Turkey is a target market for Middle Eastern financial institutions. Kuwait Finance House owns the largest Islamic lender in Turkey, Kuveyt Turk. National Commercial Bank of Saudi Arabia owns Turkiye Finans Participation Bank, and Bahrain-based Al Baraka Banking Group owns Al Baraka Turk. Other Middle Eastern institutions have targeted Islamic countries in Asia, including Malaysia (Saudi’s Al Rajhi Bank) and Indonesia (Dubai Islamic Bank, through its large stake in Bank Panin Syariah).

Egypt remains a country of interest for Middle East banks. It is a large market of some 95 million people, and increased stability and economic growth have created good business opportunities. Moreover, with the floating of the Egyptian pound and subsequent fall in its value, the market is attractive for foreign investors.

Some Middle Eastern institutions are already active in Pakistan, including Al Baraka and Dubai Islamic Bank. But it is expected that more will look for opportunities in a large market with proximity to the Middle East, particularly if further progress is made on security.

Iran is currently on a political roller-coaster ride. Optimism was high a year ago; but with the United States’s Donald Trump administration taking a hard line—and vice versa from the Iranian side—banks are not currently pursuing opportunities there, as it is not considered to be the right time.

MEGAMERGERS

The region’s biggest merger, between the UAE’s National Bank of Abu Dhabi (NBAD) and First Gulf Bank (FGB), was announced in 2016 and is scheduled to be finalized at the end of the first quarter. The two banks’ combined $175 billion in assets will make it the region’s second largest institution, just behind QNB. “The new, well-balanced bank will be an engine of UAE growth, driving further investment and economic diversification, and advancing the ambitions of entrepreneurs and the people they employ,” stated Tahnoon Bin Zayed Al Nahyan, chairman of FGB. “The bank will have the strength and expertise to support the development of the UAE’s private sector, from SMEs to large companies gathering strength to expand beyond their national borders. It is well positioned to be the strategic banking partner to the government and its agencies.”

Nasser Ahmed Alsowaidi, chairman of NBAD stated that the combined bank “will have the capital, expertise and international networks to be the preferred financial partner for

anyone doing business along the West-East corridor.” The combined NBAD and FGB will invest in distribution and focus on cross-selling wealth-management products and services. It will also look to access new high-growth segments such as nonresident Indians.

The combined bank is better positioned than most of its peers to meet increasing regulatory demands; it has a solid capital position from the outset, with a diversified business mix and funding profile, and allows good scope for growth going forward. Cost savings from the merger are estimated to be 500 million Emirati dirham ($136 million) per year, with an estimated “one-time integration cost” of 600 million dirham.

There is also ongoing discussion on a possible three-way bank merger in Qatar between Masraf Al Rayan, Barwa Bank and International Bank of Qatar (IBQ). If successful, it would create the largest Islamic financial institution in Qatar. Both Al Rayan and Barwa Bank are shariah-compliant lenders, while IBQ is a conventional lender; but the combined bank would be fully shariah compliant. The entity would also have the financial muscle and sufficient liquidity to help support Qatar’s economic growth and to finance development initiatives in line with Qatar’s Vision 2030.

Dubai-based Shuaa Capital and Bahrain’s GFH Financial Group recently announced a possible merger. The financial groups are active in investment banking, retail banking, brokerage and real estate. GFH is specifically focused on Islamic investment banking. Both institutions were highly successful and much larger prior to the 2008–2009 global financial crisis, but their balance sheets subsequently contracted and funding became more difficult. The merger would see the combined group become more active in M&A in the region and increase its capital markets and investment banking activity. Again, this illustrates that mergers are probably the easiest way to grow meaningfully in this more challenging period of lower oil prices.

Abu Dhabi Financial Group (ADFG) is the largest shareholder of both Shuaa and GFH, which have developed closer ties in the past year or so. In 2016, ADFG and GFH announced they were setting up a new Islamic investment bank, ADCorp, in Abu Dhabi.

Following ADFG acquiring its stake in Shuaa, Shuaa acquired 14% of Bahrain’s Khaleeji Commercial Bank, in which GFH owns 47%. ADFG CEO and managing director and chairman of Shuaa Capital, Jassim Alseddiqi, revealed a new strategy for Shuaa that will focus on growing assets under management, leveraging its balance sheet and developing its business in Saudi Arabia and Egypt. The investment bank’s assets under management are forecast to nearly double to 9 billion Emirati dirham ($2.5 billion) by 2020 because of the strategy.

“We are seeking to build Shuaa’s legacy as the region’s premier financial intermediary and adviser to corporates and investors by focusing on bolt-on acquisitions and leveraging the firm’s balance sheet,” says Alseddiqi. “Our long-term objective is to not only increase our assets under management, but to establish greater synergies across the operation and expand our offering of investment products and services.”

In the UAE, Bahrain’s Ahli United Bank (AUB) obtained a Category 1 Dubai International Financial Centre license. AUB is the first bank in the GCC region to obtain such a license, which will allow it to conduct all forms of wholesale banking on

a conventional and shariah-compliant basis. The key exclusion is dirham-based transactions and dealing with the retail market. An onshore acquisition is needed to achieve these capabilities.

Saudi Arabia is also an attractive market for regional banks. The Saudi banking sector is large, and the population is young and growing rapidly. ‘’The kingdom has a significant development plan, which will require substantial financing,” says Adel El-Labban, group CEO and managing director at Ahli United Bank.

GOING DIGITAL

For banks focused on organic growth, Middle Eastern institutions are ramping up their efforts in private banking and facilities for high net worth individuals. And it is not only conventional banks that are achieving good rates of growth in private banking. Fast-growing Dubai-based Islamic bank, Noor Bank, has seen good results from its priority banking (private banking) operations, which provide customers with

certified and dedicated priority relationship managers. “Priority banking has always been one of our core businesses and will continue to be a strategic focus for us going forward,” says Hussain Al Qemzi, CEO at Noor Bank. “We strive to provide our affluent customers with the best solutions to suit their individual financial requirements.” Consumer banking, although having experienced some pressure in terms of growth in 2016, still offers opportunities as bankable populations in the area grow. Mortgages, credit cards and personal loans are experiencing increased demand. Islamic financing is also registering good rates of growth in retail, trade, construction and real estate.

Banks are focused on enhancing customer-service quality and extending servicing of products through online, mobile and social channels. They continue to invest in digital banking to differentiate themselves.

Larger banks are also launching digital platforms in corporate and transaction banking to raise customer service. Particularly for retail banking customers, banks have recognized the importance of linking them toward Internet and mobile banking channels.

Despite gaps in technology and smartphone penetration, banks have tapped into consumer segments eager to adopt digital channels. “The cost and revenue position of banks that do not act to improve their digital offering may weaken relative to peers that shift more business to digital channels,” says Vinayak HV, a partner at McKinsey Singapore and leader of its digital banking practice in Asia Pacific. HV works closely with leading organizations across Southeast Asia, India and the Middle East.

The financial technology (fintech) boom that is sweeping most developed banking markets and putting pressure on banks to digitize their business, is still relatively nascent in the Middle East. According to a recent fintech survey conducted in the GCC region by EY, 79% of participants doubted whether fintech players could cause any noticeable disruption in the region’s banking sector in the next one to two years. Yet, the same survey found that 70% of bankers believe GCC banks are open to integrating innovations by fintech providers.

Two-thirds of survey respondents say GCC banks are highly likely to collaborate with or invest in fintech companies to meet consumers’ needs for digital solutions. “The pace of fintech innovation in the GCC has been extremely rapid over the past few years, but still requires more work on the ground to truly revolutionize the banking industry,” says Gordon Bennie, MENA financial services leader at EY. “The variety of ways in which fintech innovations are being adopted by the banking sector is increasing and we may even see banks collaborating to build ‘shared-cost fintech solutions’ in the future.”