Digital and mobile technologies are rapidly transforming the way Asians use financial services. Is competition or collaboration the answer for traditional banks?

From Southeast Asia to China to India, fintech is transforming Asian banking by creating new ways for businesses to raise money, modernize cumbersome service channels and bring in once-excluded customers.

For the region’s traditional banks, this is both an opportunity and a challenge. “Innovative solutions by fintechs are fast changing the customer journey for the financial-services industry, driven by stiffer competition and rising customer expectations,” says Bidyut Dumra, head of innovation at DBS Bank.

“Banks have to re-evaluate their customer-acquisition and outreach strategies” for the digital era, Dumra says. To tap into the rapid growth in internet and smartphone users, DBS recently launched digibank, a mobile-banking app, in its core markets of India and Indonesia. “Digibank is paperless and signatureless; and it brings together an entire suite of innovative technology, from biometrics to artificial intelligence, to enable customers to enjoy a whole new way of banking,” says Dumra.

Arguably, however, the revolution began without the likes of DBS. The socio-economic benefits of new financial technology innovations are already making themselves felt. SoCash, a Singapore-based provider of cash-management solutions, increases access to cash in remote areas of Southeast Asia and India, for example; Digiasia Bios makes easy online payments systems available in rural Indonesia; and trading-platform Funderbeam uses the blockchain to widen access to the capital market and open new sources of investment capital to startups.

“Small to medium-size enterprises are the backbone of Southeast Asia’s economy,” says Prashant Gokarn, co-founder and CEO of Digiasia, and an investor in Indonesian fintech. “But many are credit constrained, as financial incumbents are risk averse and disproportionately favor larger and more-reputable enterprises—meaning that it can be hard for smaller players to secure the financing they need to grow their business, or even start it.”

That’s changing rapidly. Startup Genome’s Global Startup Ecosystem Report 2017 found that five of the top 20 cities ranked by their startup ecosystems—incorporating such factors as stability, funding, transparency and talent—are in the Asia-Pacific region. China secured the top two places on the 2018 Fintech100 list and three of the top five, outperforming the US. Notably, China’s mobile-payments market is already about 50 times larger than its US counterpart, highlighting the aggressive payments landscape in which many Asian fintechs play. Besides payments, other areas of interest are lending, personal wealth management and insurance.

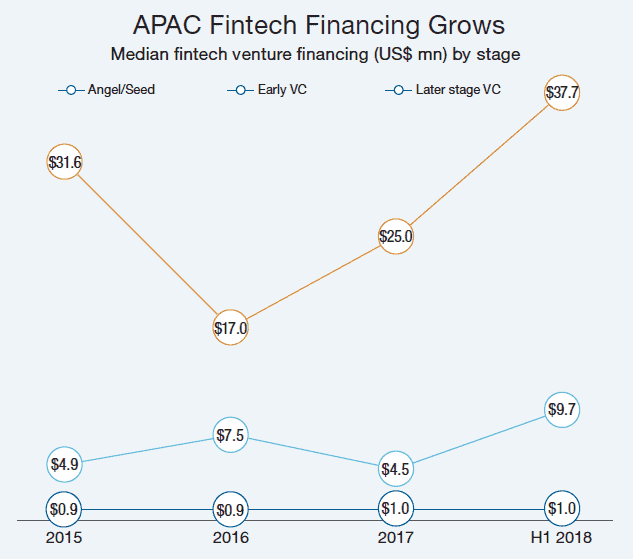

Private investors like WaterBridge Ventures and RHL Ventures are sensing opportunity. In a Series C round of funding last June, Ant Financial raised a record-breaking $14 billion from institutional investors such as Canadian Pension Plan Investment board and Khazanah Nasional Berhad; and from private investors via The Carlyle Group, Janchor Partners and others. Even without that outlier, regional fintech funding in the first half of 2018 was a robust $2.8 billion. Later stages of fundraising are raising ever-higher amounts (see chart below), a sign of the sector’s maturation. “Asia, being the world’s strongest internet and smartphone-savvy region, is ripe for fintech to plug the hole left unfilled by states and financial incumbents,” says Hari Sivan, CEO of soCash.

But regional investors are not the only ones eyeing Asia’s fintech growth; the region is home to new tech hubs across China, India, Singapore and Hong Kong, whose development is projected to soon match (or even outpace) traditional tech hotbeds such as Silicon Valley, drawing US giants such as Alphabet, Facebook and Intel—not to mention their Wall Street backers—to stake a claim in Asia.

Chinese companies are already playing a key role. “Companies such as Tencent, Baidu and Alibaba have led the innovation charge and made tremendous headway, inspiring other countries in areas such as mobile payments, fintech, drone manufacturing and the ‘internet of things’,” says Pranav Seth, OCBC Bank’s head of e-business.

Why Asia?

Armodio Corrado, formerly at Verdoso Investments, comes to Asia because it is “unexplored territory” adopting new technology much faster than Europe or the US and with a greater appetite for digital disruption. Now global vice president of operations for Difitek, a global provider of digital infrastructure aimed at new players in finance, he spends 80% of his time in Asia.

The potential to expand the footprint of financial services via fintech is enormous, says Corrado, noting that 430 million people in emerging Asia—around 70% of the adult population, excluding China—are unbanked. “So there is a huge opportunity now, not in five years,” he says. Companies like Difitek are the backbone for a new finance system and to date have attracted interest in Japan, Singapore, Indonesia and Vietnam, mainly focused on nonbank lending platforms that give the unbanked access to needed services. Difitek has launched more than 150 platforms on five continents.

In Asia, fintech has the upper hand, Corrado says. For traditional banks, compliance requirements—especially know your customer (KYC) rules—create significant delay. “An incumbent bank takes, on average, seven weeks to onboard a customer,” says Corrado, “whilst Difitek can run a KYC check in minutes using GPS-selected data points to verify client particulars (Do they spend time where they claim to live?) and digitization to research and record documents and transactions. This is a decisive advantage.”

Difitek is also helping to incubate native digital banks: nonlegacy lenders that can piggyback on infrastructure and test and launch new products. “Because we charge a transaction fee, their investment is limited and their cost base very scalable,” Corrado says, “and they can now serve client segments they wouldn’t have been able to serve with the traditional model.”

An End to Traditional Banking?

Some now prophesy the end of traditional banking as more nimble operators, unencumbered by legacy costs and strict compliance demands, take aim at customers, banked and unbanked. But some experienced banking voices see the future as essentially collaborative, as leading incumbents partner with fintechs to build joint solutions that offer scalable services across Asia. DBS sees advantages in a collaborative approach.

“We have had considerable success in collaborating with fintechs as opposed to viewing them only as competitors,” says Dumra, citing Startup Xchange, a new DBS program that matches startups to the bank’s clients. It has helped launch around 20 startups during its pilot phase up to the launch on October 30, including Jim, Southeast Asia’s first virtual bank-recruiter.

Agriculture and commodities firms have shown special interest in integrating blockchain into their supply chains. DBS has worked with several agricultural clients to create end-to-end blockchain platforms. These solutions typically track how and where products are farmed, providing end customers with the information in real time so they can transact deals in line with their environmental, social and governance (ESG) objectives.

“Innovation will continue to be a driving force in Asia, as fintechs, in collaboration with banks, continue to develop new service platforms for the increasingly connected consumers,” says Dumra, adding that democratization of technology and talent heralds a potent combination of speed and scalability to both large and small players. “It makes for exciting times.”

The region’s large traditional banks expect to still play a vital role in this transformation. “We have embraced fintechs as co-innovators and as agents of change,” says OCBC’s Seth. “Banking is all about trust; and most fintech players do not have the brand, the customer trust and the skills to deal with the ever-changing regulatory landscape. Banks are here to stay.”