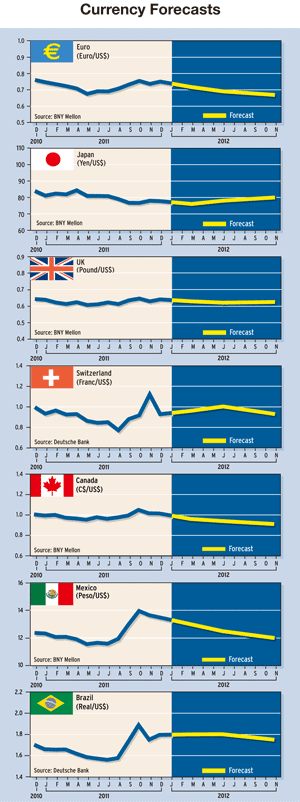

CORPORATE FINANCING NEWS: FOREIGN EXCHANGE

By Gordon Platt

Another EU summit ended in December with agreement on a new fiscal compact for the eurozone, but like previous efforts to rescue the common currency, the accord was less than comprehensive, and it failed to include the backing of Britain.

The euro rebounded and Italian and Spanish bond yields fell initially as market sentiment improved on news of the accord, which was reached in the early hours of the morning on December 9, 2011. While the agreement lacked shock and awe, analysts said it was an important step toward greater fiscal coordination.

“While a plan was presented that promises a lot, market participants can be forgiven for having a healthy dose of skepticism surrounding these summits and the promises that result,” says Brendan McGrath, senior analyst at Western Union Business Solutions in Victoria, British Columbia, Canada. The euro’s direction is still unclear, he says.

“So the summit that everyone was waiting for has come and gone, leaving many with a disappointed feeling that not enough has actually been done to contain the crisis that has now been raging for the better part of two years,” McGrath says. “While many promises were made to stick to the rules of keeping debt at manageable levels, et cetera, there were no tools offered that would supply an immediate and tangible benefit to the area,” he says.

PROMISES TO KEEP

The main aspects of the latest plan, which is supposed to be ready by March, consist mostly of promises to keep debt down, although this was already part of the European Union treaty from the start, and expansion of the capacity to fight crises, says McGrath.

“It does not seem that the crisis will end anytime soon, and there is very little to provide relief to those countries that need assistance now,” McGrath adds.

A lot of investors were hoping for a US-style policy of allowing the central bank to expand their bond-buying capacity and flood the market with euros, but the European Central Bank has resisted such calls so far. “This has dashed the hopes of a quick resolution, leaving the EU with a very long and difficult road back to financial stability,” says McGrath.

The ECB lowered its main interest rate by a quarter point to 1% at its December 8 meeting and took other steps to ease funding pressures in Europe, but European Central Bank president Mario Draghi made it clear that the central bank had no intentions of significantly increasing bond purchases in return for a fiscal compact from EU leaders. “I really wish all our leaders the best,” Draghi said at a press conference hours before the start of the summit. “What is happening is a redesigning of the fiscal agreement in a way that would enhance, rebuild confidence in the euro area.”

THREE PILLARS

Draghi said the proposed fiscal compact would consist of three pillars, the first of which would be national economic policies geared to fiscal stability, as well as growth and competitiveness. The second pillar would be rules at the EU level that would limit government debt, and the third leg would be a stabilization mechanism.

“I always find it somewhat puzzling that this [stabilization mechanism] is actually where most of the attention is focused, when we know that the lack of credibility or lack of confidence stems from the other two pillars,” Draghi commented. The ECB’s only mandate is to manage inflation, Draghi said, and EU treaties forbid it from financing governments. The rate cut was the second by the ECB since Draghi took over the presidency of the central bank in November.The central bank staff’s 2012 forecast calls for growth of negative 0.4% to positive 1%. “This is sobering—the prospect of a more prolonged downturn that leads to negative growth for the entire year, and the risks are on the down side,” says Marc Chandler, global head of currency strategy at Brown Brothers Harriman, based in New York.

“We do not think the ECB is done cutting interest rates,” Chandler says. “The 1% floor was reached previously, but there is nothing cast in stone there.” A weaker growth outlook will feed the negative feedback loop of worsening government debt-to-GDP ratios, leading to calls for more fiscal austerity and thus a deeper recession, according to Chandler.

EURO WILL SURVIVE

The most important point is that there will be no European joint bond and no substantial change in the ECB’s sovereign bond purchase program, but that the euro will survive, according to Chandler.

“At the same time, it does not change our view of the euro’s outlook,” he says. “Our stance is bearish on the euro on macro fundamental grounds, but we believe that EMU eventually will emerge stronger than when the crisis began.”

Europe is building the scaffolding of a closer fiscal union, Chandler says. The 17 eurozone central banks will loan 150 billion euros to the International Monetary Fund, and the other EU countries are expected to lend 50 billion euros.

New fiscal rules with automatic sanctions will be part of a new intergovernmental treaty, including a cap of 0.5% of GDP on countries’ annual structural deficits. The European Stability Mechanism will be accelerated and brought into force in July 2012.

UK Prime Minister David Cameron had insisted on an exception for his country from some regulations that could have threatened London’s preeminent position as a financial center. Cameron said he did not agree to the deal because it was not in Britain’s interests.

The City of London is a key national interest that the UK needs to defend from constant attack from directives from Brussels, he warned earlier.

Many investors will be disappointed that the measures adopted by the EU leaders were not the big bazooka they had hope for, Chandler says. “Yet, they were important steps that will cede more fiscal sovereignty than has been ceded previously,” he says. “It is the beginning of a process, not the end of it.”