Banks have created 1,400 new unsponsored ADR programs to meet-and hopefully generate-growing demand, particularly from investors in separately managed accounts.

The long drought in initial public offerings has slowed the pace of raising capital in the form of depositary receipts, but trading in these instruments is growing rapidly as investors continue to diversify their portfolios with securities of some of the biggest companies worldwide. As risk appetite returns, many investors are also seeking to gain at least some exposure to the faster-growing emerging markets.

The long drought in initial public offerings has slowed the pace of raising capital in the form of depositary receipts, but trading in these instruments is growing rapidly as investors continue to diversify their portfolios with securities of some of the biggest companies worldwide. As risk appetite returns, many investors are also seeking to gain at least some exposure to the faster-growing emerging markets.

Depositary receipts enable investors to purchase and sell interests in foreign shares without experiencing the settlement delays and other problems that can crop up when dealing with unfamiliar trading systems in distant countries. Trading in American depositary receipts (ADRs) and global depositary receipts (GDRs) increased by 34% last year to a record $4.4 trillion. Some of the activity reflects volatile market conditions, with investors fleeing and re-entering foreign markets as economic conditions changed in the wake of the global financial crisis.

US investors are able to trade receipts reflecting ownership in shares denominated in dollars in more non-US companies than ever before. More than 1,400 new unsponsored ADR programs have been created since October 2008, when the US Securities and Exchange Commission relaxed rules for trading depositary shares of major overseas companies in the over-the counter market. US depositary banks can now register unsponsored ADRs on the equity securities of any non-US company that automatically qualifies by meeting certain ongoing trading and online disclosure requirements. Unsponsored ADRs are securities issued by one or more depositary banks in response to market demand, without a formal agreement with the company whose shares are being traded.

Michael Cole-Fontayn, chief executive of The Bank of New York Mellon’s depositary receipt division, says growing demand from US investors for wider access to international equities for portfolio diversification convinced the bank to move aggressively to set up new unsponsored ADR programs. These programs have proved especially popular with managers of separately managed accounts (SMAs) that are restricted to investing in dollar-denominated securities. Most SMA platforms are not designed to handle foreign currency transactions. Also known as separate accounts, or wrap accounts, SMAs are similar to mutual funds aimed to include particular asset classes. The major difference is that the SMA manager purchases the securities for individual clients rather than a fund. SMAs are sold to high-net-worth individuals through major brokerage houses.

The Bank of New York Mellon has issued more than $1.4 billion of unsponsored ADRs since the SEC implemented rule changes last October to make it easier to establish these securities. “Institutional and retail investors alike can no longer ignore this segment of the ADR universe,” Cole-Fontayn says. The bank has created 715 new unsponsored programs from 35 countries, far more than any other depositary bank.

“The regulatory change was signaled by the SEC fairly clearly in advance, which enabled us to be in active dialogue with the overseas companies that were good candidates for unsponsored programs even before the rule was issued,” Cole-Fontayn says. The bank’s staff put in many hours doing the appropriate due diligence, he says. “We had to make sure that the websites of these companies fulfilled the SEC requirement that certain disclosures are made available on a timely basis in English,” he explains. “We also had to make sure we were in compliance with know-your-client regulations.”

Of the bank’s 715 new unsponsored programs, 164 are actively traded, Cole-Fontayn says. “Of the thousands of non-US companies without ADR programs, we selected those likely to attract the most interest from investors,” he says. These included companies that are constituents of local indexes that investors like to benchmark and companies that were suggested by major investor clients of the bank.

“Despite turbulent market conditions, we are not surprised at the significant investor interest in these securities,” Cole-Fontayn says. “For years US investors have insisted upon a more complete roster of international equities for greater portfolio diversification.”

In May The Bank of New York Mellon introduced a Classic ADR Index that expands the investable constituents of the bank’s well-known ADR index to include all publicly traded ADRs, including those that trade in the over-the-counter market. The new index includes 34 subindexes and offers much greater coverage. When added to existing sponsored ADRs, the new unsponsored programs enable investors to better replicate many of the world’s leading foreign equity indexes in US-traded, dollar-denominated securities, the bank says.

Some 15 to 20 companies contacted by The Bank of New York Mellon about setting up unsponsored ADR programs decided to create sponsored programs with the bank instead. Since then, another handful of companies switched from unsponsored to sponsored programs, and an additional 60 are considering making the change, according to Cole-Fontayn.

Some 15 to 20 companies contacted by The Bank of New York Mellon about setting up unsponsored ADR programs decided to create sponsored programs with the bank instead. Since then, another handful of companies switched from unsponsored to sponsored programs, and an additional 60 are considering making the change, according to Cole-Fontayn.

Edwin Reyes, global product manager for depositary receipts at Deutsche Bank, says that, in the past, initial public offerings were a good source of new sponsored DR issues and that the current drought in IPOs has been challenging for all of the depositary banks.

Despite these challenging times, the SEC rule change has created a timely opportunity for the depositary banks to be more active in opening unsponsored programs, Reyes says. Of the approximately 435 new unsponsored ADR programs introduced by Deutsche Bank since last October, more than 130 are for companies based in Japan, far more than in any other country. “Historically, year after year, Japan-based companies have had more unsponsored as opposed to sponsored programs,” he says.

The approach of Deutsche Bank has been to vet proposed programs with the issuing companies, even though this is not required, Reyes points out. “We try to educate the companies, and we work closely with them by offering seminars and working with third parties, such as law firms,” he says. “This is favorable for the issuing companies.” Some of the new unsponsored programs are gaining traction and are actively traded, he notes. “We are happy with what we are seeing, and we are optimistic,” he says.

|

|

|

|

||||

|

|

|

|

“Some companies with unsponsored programs opened by other banks have told Deutsche Bank they do not want such programs and asked the bank not to open any,” Reyes says. “In such circumstances, the bank always respects their wishes,” he says. He adds that he is comfortable with unsponsored programs for the same issuers being introduced by multiple depositary banks. “We have been working successfully with unsponsored programs for decades,” he points out.

Nancy Lissemore, global head of depositary receipt services at Citi, says that well over half of the 231 new unsponsored ADR programs introduced by the bank since October 2008 have become actively traded. Citi is also the depositary bank for 82 unsponsored programs that were created before the SEC’s relaxed new registration rules came into effect. “Our decisions on which new programs to open are driven by investor demand,” Lissemore says. “We are in communication with large investors, so we know their needs, and we select issues that are widely held in non-dollar-denominated portfolios,” she adds.

“The success of these programs has highlighted to issuers that there is pent-up demand among US investors for blue-chip companies listed on overseas exchanges,” Lissemore says. Some of the new unsponsored ADR programs already have converted to sponsored programs. One notable example is Iberdrola Renovables, based in Bilbao, Spain, which is the world’s largest wind-power generator and has interests in other forms of renewable energy.

Banks Target Japan

A significant proportion of Citi’s unsponsored programs are for companies based in Japan, the second-largest economy in the world. “There are a large number of attractive companies based in Japan,” Lissemore says. Of the more than 3,800 stocks that trade on Japanese stock exchanges, only 19 are listed on the New York Stock Exchange.

Meanwhile, Citi entered into an agreement last December with Mitsubishi UFJ Trust and Banking to jointly develop, market and offer Japanese depositary receipt (JDR) services. The JDR services will target issuers based outside of Japan that wish to raise capital in the Japanese financial market. Citi already has some similar experience in the region, having been the first bank to announce the launch of Hong Kong depositary receipts (HKDRs) in July 2008.

“Citi has a strong culture of relationship banking and only opens new programs after discussions with issuers,” Lissemore says. If a foreign company were to stop publishing the required information in English in a timely manner on its website, Citi would stop issuing new ADRs into the program, she says.

Recent initial public offerings have been few and far between as a result of market conditions, but there is still a need for capital to be raised in the form of sponsored depositary receipts, Lissemore says. “I do see the market starting to simmer,” she says. “Once the IPO market comes back, you will see some issues from Brazil, India and elsewhere in Asia. You can include issuers from the Middle East, as well,” she adds.

Some major banks have been slower to jump on the unsponsored ADR bandwagon. J.P. Morgan has introduced fewer than 20 programs since the SEC rule change last October. The bank has been adamant that new programs should be opened in a controlled manner and only with the full consent of the issuing companies. “This mirrors our strategy with sponsored ADR programs, where we work more selectively with issuers that would expect to attract meaningful investor interest and we develop a strategic plan,” says Claudine Gallagher, New York-based global head of the depositary receipts group at J.P. Morgan. “The various depositary banks have taken very different strategies,” she says.

“I am not surprised by the large number of unsponsored programs that the other banks have created,” Gallagher says. “It is easy to open a program, but it will take some time before they attract significant trading interest.” Even for sponsored programs that are carefully planned, it can take 18 months for a program to build some momentum, she adds.

Many Japanese issuers in particular are not keen to have unsponsored ADR programs opened in their shares, and several Japanese companies have asked that these programs be closed, Gallagher says. “They are cautious about their exposure to the US market,” she says. “Their own capital markets are broad and deep, and the focus on client relationships is very important. I would put the Japanese companies in the same bucket with the mature markets of Western Europe,” she adds.

Depositary banks that issue unsponsored ADRs need to check the foreign companies’ websites on a regular basis to make sure that proper disclosures are being made. “This is why it is so important to get the issuers’ blessings and to work in conjunction with them,” Gallagher says.

Valuations Mirror Market Conditions

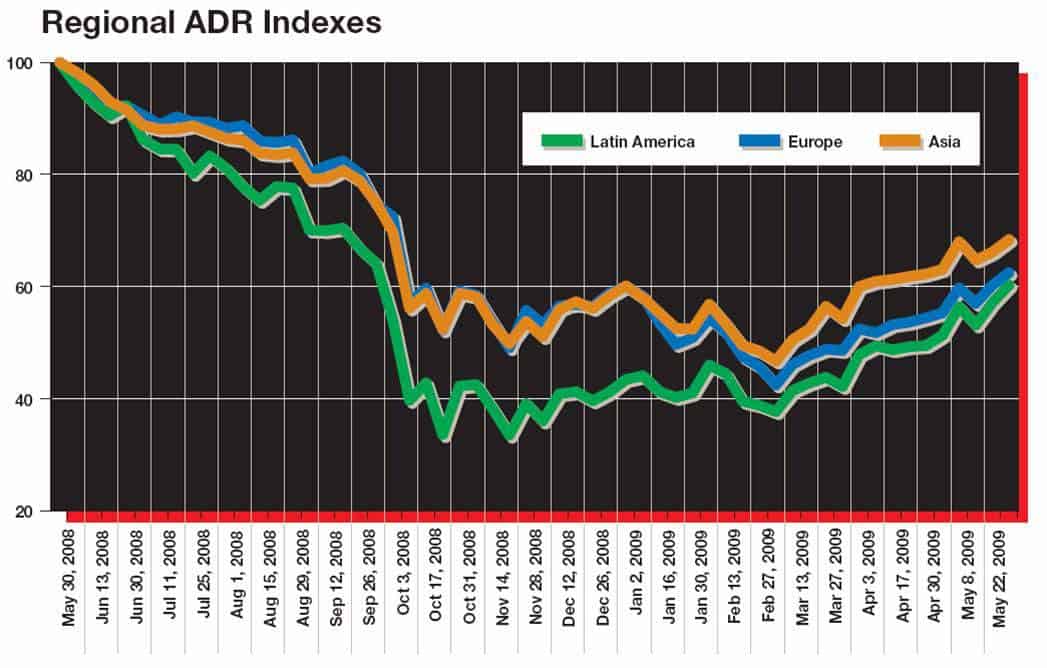

The trading volume of depositary receipts (ADRs and GDRs) totaled 35.6 billion shares in the first quarter of 2009, a 17% increase from the same period a year earlier, according to J.P. Morgan. However, the value of DR trading in the first quarter fell 52% from the same period last year to $588 billion, reflecting steep market declines. “We are starting to see some normalization in the markets more recently,” Gallagher says. “Underwriters are starting to talk about new equity issues once the markets stabilize. They are planning and setting tentative dates for issues,” she adds.

Meanwhile, the flood of new unsponsored ADRs is changing the face of the US over-the-counter market. R. Cromwell Coulson, chairman and CEO of Pink OTC Markets, says almost $100 billion, or two-thirds of the dollar volume traded in the OTC markets in 2008, was in the form of ADR trading. “During the next few years half of the new unsponsored ADR programs will switch to sponsored programs,” he predicts. Companies that are investor-focused will want the information and control that comes with having a sponsored ADR, he says.

Pink OTC Markets is an inter-dealer quotation system for the OTC market. On May 15, 2009, it listed its first Brazilian company, JBS, the world’s largest beef producer and exporter. The company listed on OTCQX International Premier, the OTC market’s highest tier for companies that can meet high international standards for capital, sales and assets.

Companies listed on OTCQX provide US investors with access to their latest news and disclosure information, Coulson says. “OTCQX gives companies listed on a qualified foreign stock exchange a visible cross-listing in the US, without the duplicative regulatory costs required for listing on a traditional US exchange,” he says.

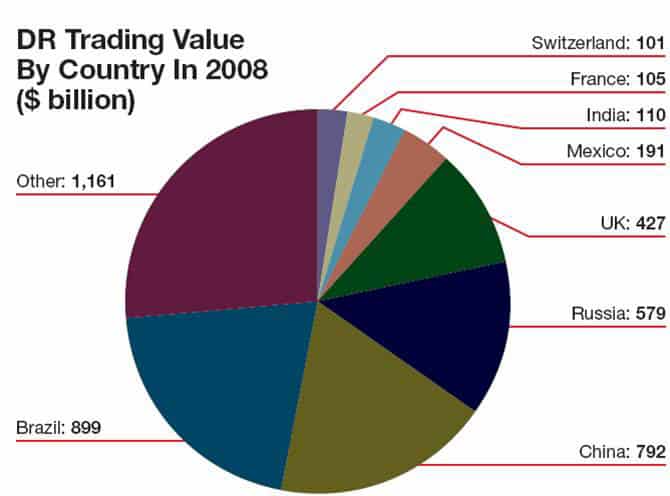

Sponsored ADR programs historically have been created to trade shares of established issuers in developed countries. While companies based in Brazil, Russia, India and China accounted for more than half of the total value of worldwide trading in depositary receipts last year, the BRIC countries account for relatively few of the new unsponsored ADR programs.

Many of the big emerging market countries have erected regulatory hurdles to unsponsored programs. The Brazilian regulator CVM, for example, has approved only one of 20 recent proposals to create unsponsored ADRs. This could be tied in part to the desire of central banks in these countries to control inflows of hot money, bankers say. India permits only DR programs related to the raising of capital. China allows only H-share unsponsored DR programs for companies listed in Hong Kong. Even in the face of regulatory hurdles, bankers believe that with the supply of DRs in the market greatly expanded, their popularity with investors is bound to keep growing.