Derivatives Stage A Comeback

Market participants are rediscovering the appeal of derivatives, and the providers that stayed the course during the recent meltdown are reaping the benefits.

By Laurence Neville

In the year covered by Global Finance’s sixth annual awards for the World’s Best Derivatives Providers, the world of finance changed beyond recognition, and the derivatives markets have been no exception. While the receivers of Lehman Brothers and AIG are still unraveling the complex trades that brought the two firms down, the wider market is digesting the implications of the financial crisis in terms of regulation, trading practices and the number of market participants.

In the year covered by Global Finance’s sixth annual awards for the World’s Best Derivatives Providers, the world of finance changed beyond recognition, and the derivatives markets have been no exception. While the receivers of Lehman Brothers and AIG are still unraveling the complex trades that brought the two firms down, the wider market is digesting the implications of the financial crisis in terms of regulation, trading practices and the number of market participants.

In the immediate aftermath of the crisis, many derivatives markets fell sharply, with the credit derivatives market—which was the heart of many of the world’s banks’ problems—worst affected. Tentative growth has since returned—with the exception of the credit derivatives market, which continues to shrink—as stability has begun to return to the financial system.

Market participants have rediscovered the benefits of derivatives for customized risk management solutions to help navigate the more uncertain economic landscape, according to Eraj Shirvani, chairman of the International Swaps and Derivatives Association (ISDA) and head of fixed income for EMEA at Credit Suisse. “This continued growth is a testament to both the utility of derivative instruments and to the industry’s ongoing efforts to reduce risk and enhance operational efficiency,” he says.

According to ISDA’s most recent survey of over-the-counter (OTC) derivatives trading, which covered the first half of 2009, the notional amount outstanding of credit derivatives—credit default swaps referencing single names, indexes, baskets, securitized obligations and portfolios—decreased by 19% in the first six months of the year to $31.2 trillion from $38.6 trillion. Over the preceding 12 months, credit derivative notional amounts decreased by 43% from $54.6 trillion at mid-year 2008.

In contrast, notional amount outstanding of interest rate derivatives, which include interest rate swaps and options and cross-currency swaps, grew by 3% to $414.1 trillion from $403.1 trillion. This compares with a 13% decrease from $464.7 trillion during the second half of 2008. Over the preceding 12 months, interest rate derivatives decreased by 11% from $464.7 trillion in mid-2008.

Despite the strong run in many global stock markets from March onward, notional amount outstanding of equity derivatives, which consist of equity swaps, options and forwards, remained relatively flat at $8.8 trillion for the first half of the year. This compares with a 27% decrease from $11.8 trillion during the second half of 2008.

Figures from the Bank for International Settlements, which measures activity on derivatives exchanges, show similar trends. During the second quarter of 2009, total turnover based on notional amounts increased to $426 trillion from $366 trillion in the previous quarter, consistent with a return of risk appetite. The increase was mostly accounted for by derivatives on shortterm interest rates, where turnover rose to $344 trillion compared to $294 trillion in the previous quarter.

Turnover in equity index derivatives also increased in the second quarter, from $37 trillion to $43 trillion, chiefly as a result of rising equity valuations. Global turnover measured in the number of contracts traded rose by less than 100 billion. Activity in foreign exchange derivatives began to recover as well, with turnover increasing to $5.9 trillion from $4.8 trillion in the preceding quarter.

Trading in commodity futures and options increased slightly in the second quarter. Global turnover in commodity derivatives measured in numbers of contracts (notional amounts are not available) stood at 446 million, compared to 423 million in the previous quarter. Major contributors were contracts on agricultural products and non-precious metals, while trading in energy derivatives fell.

While both OTC and exchangetraded derivatives volumes have recovered, with the exception of OTC credit derivatives, the wind is clearly in the sails of exchange trading, given concerns about counterparty risk. Regulatory pressure is mounting in both the United States and Europe and in mid- October, the US House Financial Services Committee passed legislation to regulate the OTC derivatives market— effectively driving trading and clearing for all asset classes onto exchanges.

More generally, across almost all asset classes it has been a tough year for banks. Strong correlation within and across asset classes and massive volatility in the latter part of 2008 and the early part of this year caused heavy losses at a number of banks, and many have quietly withdrawn. The result is a smaller group of banks whose commitment is beyond doubt—a characteristic that investors and corporates would do well to remember once markets fully recover and new entrants pile back into the derivatives market.

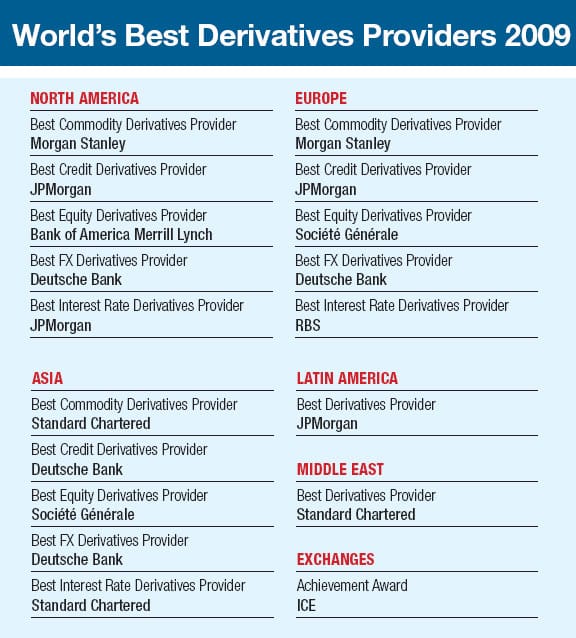

It is this commitment expressed through scale, reputation, competitive pricing and innovation that the Global Finance awards for the World’s Best Derivatives Providers seek to highlight. The awards cover each asset class across the three main financial regions of the world—North America, Europe and Asia—as well as overall awards for the best derivatives bank in Latin America and in the Middle East.

North America

Best Commodity Derivatives Provider

Morgan Stanley

Morgan Stanley’s legendary commodities team harnesses over 350 professionals from more than 40 countries, and the bank has continued to provide leadership during one of the most volatile periods for commodity prices in living memory. Morgan Stanley provides liquidity and risk management solutions to industrial organizations, corporations and financial institutions across a uniquely broad commodity spectrum.

One of the most critical drivers of Morgan Stanley’s success in commodity derivatives is its exposure to physical commodity trading. This gives it insight into trends at the coalface (sometimes literally), which allows it to effectively manage its own and its clients’ risks in the derivatives market.

Among the many important deals Morgan Stanley has led over the past year is the $1.2 billion financing of Texas-based independent power producer Topaz Power. The bank’s ability to physically deliver gas and take power through 2014 as part of the transaction was crucial, while the commodities derivatives business enabled Topaz to optimize its asset portfolio through trading, scheduling and delivering both physical power and physical gas in the spot markets.

Best Credit Derivatives Provider

JPMorgan

JPMorgan effectively created the credit derivatives market more than a decade ago, and despite its alumni leaving to establish operations at rival banks, it has remained the pre-eminent bank. That heritage stood it in good stead during one of the most event-driven periods in financial history. While other counterparties stepped down from providing liquidity in order to manage exploding risk profiles, JPMorgan stepped up to deliver first-class solutions with best execution.

Moreover, only JPMorgan was willing— and sophisticated enough—to help other banks exit the correlation trading business. The bank was able to price securities that no other bank could, allowing banks to free up capital and use it to extend much-needed credit into the market.

Best Equity Derivatives Provider

Bank of America Merrill Lynch

Bank of America (BoA) Merrill Lynch offers a comprehensive suite of equity derivatives, with a strong index options trading desk covering S&P; 500, Nasdaq and Russell options and another dedicated to exchange-traded funds (ETF) options. BoA Merrill Lynch also has a team dedicated to light exotics and a full fund-structuring team.

For VIX options, the bank generally ranks in the top two in trading market share. In ETF options BoA Merrill Lynch handles a significant percentage of the daily volume in some of the large ETFs (such as financial sector and gold ETFs).

In single stock options, BoA Merrill Lynch spans all of the major sectors in the United States and has access to as many or more countries as any other bulge-bracket dealer. Merrill Lynch’s integrated Delta One desk in the United States trades all Delta One products, including ETFs, index and single stock swaps—one of the few banks to combine products in this way. The company also has a separate group that deals with equity derivatives transactions with corporations.

Best FX Derivatives Provider

Deutsche Bank

If any derivatives market is about scale, then it is foreign exchange. And within the North American foreign exchange market—indeed, all major FX markets— there is no bigger bank than Deutsche Bank. The bank now has a bigger share of the foreign exchange market than Citi, JPMorgan, HSBC and Goldman Sachs combined, and the gap between Deutsche Bank and the rest of the industry is growing.

The scale and depth of Deutsche Bank’s trading operation is crucial to its success because it allows it to offer more competitive rates on a wider range of FX derivatives than any other bank, and in bigger sizes and longer maturities. Crucially, the bank has achieved this growth without proprietary trading—something that got many banks into trouble in the depths of the crisis—and with a lower value at risk than many of its rivals.

Best Interest Rate Derivatives Provider

JPMorgan

With liquidity at a premium in the interest rate derivatives market, only a handful of banks have been able to provide consistent support to clients and posithe wider interbank market. Of these, JPMorgan has shown the greatest depth and breadth of ability in both the US dollar and euro markets—in both vanilla products and exotics. Its ability to source liquidity from a wider pool than just the interbank market—through a welldiversified client base—has been crucial.

Europe

Best Commodity Derivatives Provider

Morgan Stanley

With more than 25 years in the business, Morgan Stanley’s depth and breadth in terms of product and geographical coverage is unrivaled. The integrated nature of Morgan Stanley’s physical and derivatives commodity operations in the US, Europe and Asia is central to the bank’s skill in anticipating trends and using that knowledge to help its clients plan ahead. Recent releases show that Morgan Stanley had $315 billion worth in gross notional swap transactions outstanding, including commodity index deals structured as total return swaps with pension funds and other institutional investors, as well as hedging transactions with producers and merchants.

Moreover, the bank’s ability to work with commodity producers and institutional investors and distribute to retail— in the last year alone, it completed more than 50 primary deals across Europe and Asia, including exotic options and structured notes—gives it superior visibility and greater ability to manage risks.

Best Credit Derivatives Provider

JPMorgan

JPMorgan has proved a stalwart throughout the financial crisis, facilitating life-saving risk transfers and working with regulators to build transparency in credit derivative pricing and settlement. The bank’s foresight has been crucial: Its research team made the right call on the market.

Armed with this foresight and applying strict risk management, JPMorgan proactively and successfully positioned its trading books to minimize the impact of defaults, spread-widening and technical dislocations that crippled other banks. Later, as defaults occurred, JPMorgan partnered with ISDA to facilitate CDS auctions. The bank continues to provide liquidity on defaulted bonds, while other counterparties have decreased their trading of these securities.

Best Equity Derivatives Provider

Société Générale

Société Générale proved itself during the volatile fourth quarter of 2008 by standing by clients when many other big-name banks effectively abandoned the equity derivatives market. On several days during that quarter, the bank was the only counterparty able to price certain options on equity indexes—a fact reflected in its 43.46% market share, placing it first among the DJ Stoxx 50 Index Futures’ 19 market makers.

Société Générale was able to provide liquid and transparent alternative investment solutions and help clients raise capital and make the most of equity markets through concepts specifically designed to cope with uncertain markets because it had the flexibility to innovate even during turbulent times. Of course, the bank had maintained a prudent risk management policy. This was strengthened through the €150 million “Fighting Back” contingency plan implemented following the bank’s trading scandal last year. Société Générale also had sound macro-hedges and defensive positions put in place as early as the end of 2007 that allowed it to perform better than its competitors.

Best FX Derivatives Provider

Deutsche Bank

Deutsche Bank’s fortitude in providing its customers with liquidity in the depths of the market turmoil is just one of the factors that contribute to its overwhelming success in global foreign exchange derivatives. The bank is also a leading designer of structured hedging strategies that allow clients to protect themselves against FX risk at a lower cost than is possible using plain-vanilla products.

Perhaps most importantly, Deutsche Bank continually reviews, updates and enhances every product, strategy and position to ensure that they fit market conditions. During 2008 and 2009 this approach was vital: FX rates were exceptionally volatile, with record moves in almost every currency pair, rendering many strategies not just ineffective but dangerously inappropriate. Deutsche Bank responded to this shift faster than any other bank due to its continuous review system, providing clients with advice, restructuring existing positions and developing new hedging and investment products that worked in the new market environment.

Best Interest Rate Derivatives Provider

RBS

At the heart of the financial storm itself for much of the past year, RBS nevertheless was able to take a wider view on the interests and exposures of its clients, leading it to develop concepts that offered what it describes as “holistic solutions.” Rather than focusing on turning over high volumes of individual products, the bank has delivered tailored solutions, which it believes represents a sustainable business. Its new products have resulted from the analysis of all influencing factors, including macro and specific economic environments, financial markets context and client-specific risk and exposures, as well as investment interests and policies.

For issuers, RBS has developed comprehensive frameworks and platforms to help clients identify and manage risks relating to hybrid credit and rates that are associated with a portfolio of callable bonds. In a farsighted move, the bank also introduced macro-hedged funding in 2007 to help clients decrease their funding costs in a recession—a concept that only RBS has been able to offer clients to date.

Asia

Best Commodity Derivatives Provider

Standard Chartered

Standard Chartered offers risk management solutions across the full spectrum of commodities, with specialists in precious metals, base metals, energy and agriculture, and a wide range of capabilities across energy products, including petroleum and petroleum products, coal and freight. The bank’s commitment to developing the Asian commodities market has not flagged despite the high price volatility, lack of market liquidity, reduced credit lines and heightened counterparty risk of the past year.

Standard Chartered tripled the number of customers it worked with during 2008 compared to the previous year and believes it is on track to double its customer base again in 2009. Similarly, its deal volume has dramatically increased as many US and European banks have shifted their focus from growing their business to sorting out their balance sheet problems and staying afloat in their domestic markets. As credit lines were withdrawn, Standard Chartered was able to effectively promote its strength in commodity derivatives.

Best Credit Derivatives Provider

Deutsche Bank

Deutsche Bank has done more than any other bank to help investors, borrowers and traders through the turbulent market conditions of the past year. It remained a significant provider of liquidity across both cash bonds and credit default swaps and is an active trader in more than 250 Asian credits. The bank enjoyed a 25% increase in trading volumes over the award period and a 40% increase in trading volumes during the third and fourth quarters of 2008.

Crucially, Deutsche Bank consistently used its balance-sheet strength to provide funding to Asian borrowers during the crisis period. The bank also established a specialist structuring unit with a focus on customized solutions for investors and borrowers.

Best Equity Derivatives Provider

Société Générale

Société Générale has used the opportunity presented by the financial crisis to strengthen its corporate and institutional equity derivatives business in the Asia-Pacific region. With market conditions characterized by liquidity concerns and volatility issues, Société Générale has been able to prove to clients that it has staying power: The bank continued to generate new services and solutions that meet the demands of the market environment and also succeeded in expanding its client base and reinforcing its track record of innovation in equity derivatives.

Among Société Générale’s achievements in the past year in Asia is the strengthening of its regional cross-asset platform as well as its flow and asset liability management (ALM) businesses. These are areas that draw on the bank’s resources in fixed income and equity derivatives in order to provide solutions to clients that span different fields of risk management. These solutions—all aimed at helping clients to manage their risks more efficiently—include assistance with strategic acquisitions and market risk advisory for corporates.

Best FX Derivatives Provider

Deutsche Bank

Deutsche Bank’s commitment to meeting clients’ needs during the period of unprecedented volatility last year meant, at the most basic level, provision of liquidity when other banks withdrew from markets and scaled back credit lines. However, the bank’s commitment also showed itself in the creation of new top-down, holistic analytical models that allow clients to get a deeper, more strategic understanding of their FX risks and opportunities and to take views and hedge risks quickly and on a portfolio-wide basis. Demand for this type of analysis and advice is growing rapidly as FX moves up the agenda from treasurer to CFO and CEO level. Deutsche Bank is the first bank to meet that demand.

Deutsche Bank has also been proactive in developing new products to meet the changed needs of the market. In March 2009 it developed the first-ever product to allow investors and borrowers to cap the potential mark-to-market losses on all their FX hedges via a single contract. The product, FlexFolio, also allows companies to protect themselves against FX volatility more cost-effectively than in the past.

Best Interest Rate Derivatives Provider

Standard Chartered

Standard Chartered’s recent track record speaks for itself. Its revenue from interest rate derivatives increased seven-fold from 2007 to 2009 while the number of new and active clients increased three-fold. This impressive growth is a result of a commitment made by Standard Chartered in 2007 to become the number-one rates house in Asia, Africa and the Middle East. The strategy entailed realigning its business structure to support its clients with superior pricing and world-class structuring solutions, increasing expertise and capabilities by making significant hires, and investing in infrastructure, both front and back office.

Despite challenging market conditions throughout 2008, Standard Chartered pursued its strategy and, as a result, continued to deepen its client relationships and gain market share at a time when many of its competitors were distracted by the turmoil and pulled back. During the second half of 2008, as many competitors were reducing their credit and market risk appetite, Standard Chartered remained open for the “flight into flow” that followed the market disruption.

Latin America

Best Derivatives Provider

JPMorgan

The local knowledge gained from the strength of JPMorgan’s investment banking franchise in Latin America—combined with the bank’s world-class derivatives capabilities across equity, credit, foreign exchange, rates and commodities—makes it a powerful force in Latin American derivatives. While JPMorgan’s capabilities are strongest in Brazil, it also has strength in other regional markets.

JPMorgan has suffered little from the problems surrounding the sale of options that allowed corporates to bet against domestic currencies. The sharp currency depreciation in Latin America after mid-September 2008 resulted in large losses for some of the top companies in Brazil and elsewhere—driving some companies to bankruptcy—and is estimated by the Bank for International Settlements to have resulted in losses of as much as $25 billion. Despite further muddying the name of derivatives, Latin America—which has had a relatively benign economic crisis to date—is a likely source of massive derivative volume growth, and JPMorgan is well placed to benefit.

Middle East

Best Derivatives Provider

Standard Chartered

Market dislocation and the resulting turbulence over the past year have shown that risk management can make or break an organization. Volatility across asset classes has resulted in increased demand from clients to manage a broad range of risks—including foreign exchange, interest rates, commodities, equities and credit—across balance sheets, from funding to investment risk.

In the Middle East, Standard Chartered’s deep understanding of Islamic values—reflected, for example, in the bank’s ground-breaking shariah-compliant FX and rates products—has helped equip clients with appropriate shariah-compliant risk management tools, which have helped them to navigate through turbulent times.

In 2008 Standard Chartered launched its regional trading hub for the Middle East and Africa in the Dubai International Financial Centre, which is one of three global hubs and now home to the bank’s G10 spot/forward, options desk and African spot/forward desk. Covering London trading hours, it replaces Standard Chartered’s London center, giving its regional customers unrestricted access to the most significant time zone for dealing FX and FX options.

Exchanges

Achievement Award

ICE

While all derivatives trading suffered in the turbulent second half of 2008, the pain was not equally felt. Corporates and investors responded to the new market environment by moving from OTC trading to exchanges. To be sure, OTC volumes have recovered somewhat—with the exception of credit derivatives—but the need for transparency, liquidity and standardization has accelerated a long-standing trend.

The market is credit default swaps (CDS), a $26 trillion market, where the move to exchange-based trading is driven as much by regulatory pressure as consumer preference. Eurex, NYSE Euronext and CME have all established CDS platforms. However, ICE, through its acquisition of electronic trading platform Creditex and clearing house CCorp, is in pole position in both the US and Europe. It not only launched its offering ahead of most of its competitors but made sure it had the technological and bank backing to succeed.