Dollar Will Remain Buoyant As Long as the Federal Reserve Keeps Raising Rates, Analysts Say

Interest-rate rises are like vitamins for the dollar, which jumped to its highest level in two years in November and which will continue to flex its muscles in the months ahead, currency analysts say.

Although European policymakers are moving closer to hiking rates on the Continent, the United States is expected to maintain a wide advantage in rate differentials for months to come. And the same holds true for US rates compared with those in Japan, analysts say. Judging by the trading level of federal funds futures, US short-term interest rates are expected to climb to 4.75% by the end of the first quarter of 2006, says Marc Chandler, global head of currency strategy at Brown Brothers Harriman in New York.

Virtually nobody was surprised when the Federal Reserve raised interest rates another quarter of a percentage point to 4% on November 1, for the 12th straight rise since June 2004. Price pressures are evident in the US economy, and the Fed will likely raise rates by a quarter point at their December 13 meeting, Chandler says. Another quarter-point increase is likely, he says, at the Feds two-day meeting on January 30-31, 2006, the last Federal Open Market Committee meeting to be led by chairman Alan Greenspan.

When Ben Bernanke succeeds Greenspan as Fed chairman and heads his first FOMC meeting on March 28, 2006, the new Fed chief likely will want to establish his anti-inflation credentials and to continue the gradualist approach of his predecessor by raising rates another quarter point, Chandler says. Meanwhile, the European Central Bank recognizes the fragility of the eurozones economic recovery and will be reluctant to raise rates by more than a quarter point to 2.25% late this year or early in 2006, he says.

The ECB left its target rate at 2% on November 3, and the banks president, Jean-Claude Trichet, said the level, which has been unchanged for more than two years, was still appropriate. The ECB doesnt need to be in a hurry, Chandler says. And any tightening that the market anticipates from the ECB over the next several months is being offset by the markets discounting an extension of the Feds tightening cycle.

|

Yen Keeps Sliding |

|

The dollar has shown big gains against the Japanese yen, reaching a 26-month high near 118 in early November, mainly as a result of interest-rate considerations, analysts say. The Bank of Japan has kept rates near zero since 2001 and will move cautiously in raising rates next year, analysts say.

Given the lingering deflationary forces in Japan, the weaker yen may be quietly welcomed by officials and may help boost already-strong corporate earnings, according to Chandler. Thus, contrary to conventional wisdom, which had expected a rising Nikkei stock average to be good for the yen, a weaker yen may actually be supportive of Japanese share prices in the current environment, he says. Michael Woolfolk, senior currency strategist at the Bank of New York, says strong US economic growth, rising rates and contained inflation are all lining up in favor of continued strength in the dollar. The personal consumption expenditures, or PCE, core index, Greenspans favored quarterly measure of inflation, actually eased to 1.3% in the third quarter from 1.7% in the second quarter. This should provide some comfort to ongoing concerns over rising inflationary risks outside of energy prices, Woolfolk says. Meanwhile, the third-quarter US gross domestic product report, which showed an increase of 3.8% at an annualized rate, was everything it was advertised to be and more, he says. While the Fed has adopted a more hawkish stance since Hurricane Katrina, the nomination of Ben Bernanke has curbed some of the enthusiasm for the dollar based upon the markets assessment of him as being more dovish than Greenspan, Woolfolk says. |

Helicopter Drop

Bernanke is best known in the financial markets for his anti-deflation campaign at the Fed, according to David Gilmore, economist and partner at Essex, Connecticut-based Foreign Exchange Analytics. Bernanke was worried that near-zero inflation and stagnant economic activity could prompt a Japan-like bout of US deflation, Gilmore says.

In a November 2002 speech to the National Economists Club in Washington, DC, Bernanke outlined just what the Fed could do if deflation were to occur. A broad-based tax cut accompanied by a program of open-market purchases to alleviate any tendency for interest rates to rise would almost certainly be an effective stimulant to consumption, he said. A money-financed tax cut is essentially equivalent to dropping money from a helicopter, he noted.

What the deflation story showed is that Bernanke pays lots of attention to the price level and inflation measures generally, Gilmore says. And, as an advocate of inflation-targeting, I think it is a safe assumption that he would be as reactive to inflation approaching the top end of the Feds threshold as the bottom end.

In theory, a more rules-based monetary policy with more transparency should result in reduced asset-price volatility, according to Gilmore. I also think that Bernanke could step into his first FOMC meeting in late March with a need to hike, simply to show markets that he has symmetry in handling upside as well as downside risks to prices, he says. And if the wheels stay on the economy and restraint is embraced by Bernanke, then we can look for a 5%-5.5% federal funds rate in relatively short order in 2006, he adds.

|

Deficits Detract |

|

The dollar may well press higher based on interest-rate considerations, Gilmore says, but the higher it goes, the harder it will fall, due to structural problems related to the US budget and trade deficits, he says. I think it is inevitable that the wheels will come off, he asserts.

Many currency analysts at the major banks continue to forecast a weaker dollar over the medium to longer term, and they warn that the US eventually will need to address the steady deterioration in the current account deficit. Interest rates are the main influence on the market at the moment, says Chandler of Brown Brothers Harriman. When the Fed is tightening policy, cyclical factors such as economic-growth differentials and interest-rate differentials offset worries about the current account, he says. Interest rates do a better job of explaining both the dollars decline from 2001 through 2004 and its strength this year than does the current account, he notes. For now, the dollar will remain strong, as generally good US economic data and comments from Fed officials, including Greenspan, reinforce expectations of additional tightening in monetary policy going forward, says Robert Lynch, head of Group of 10 foreign exchange strategy, the Americas, at HSBC Bank in New York. But a key message to take away from the ECBs November press conference is that the central bank could move on rates at any time, he says. The perceived risk for an ECB tightening will again be a factor in the market as the December ECB policy meeting approaches, he adds. The ECB confirmed in early November that if the eurozone growth outlook continues to improve, policy would have to become less accommodative in coming months, says Jos Luis Alzola, European economist at Citigroup in London. But contrary to some market fears, the ECB stopped short of indicating that an interest rate hike was imminent, he says. If the European recovery continues to gather steam, the ECB likely will begin a gradual tightening cycle sometime around next March, Alzola says. As long as underlying inflation and price expectations are contained, the ECB would be willing to let the recovery strengthen before moving to raise rates, according to Alzola. |

Repatriation Flows

The dollar is unlikely to get much of a boost from the repatriation of as much as $400 billion of earnings by US multinational companies this year at a special reduced tax rate under the Homeland Investment Act, analysts say.

There could be some increased dollar buying ahead of the year-end closing of the window for US corporations that want to repatriate funds under the program. However, the impact of the inflows will be minor in the foreign exchange market, which trades $1.2 trillion daily, says Stephen Kuhl, vice president of foreign exchange solutions and strategy at Travelex, which facilitates international fund transfers for multinational corporations and handles 50% of currency-exchange note volumes at international airports worldwide. Its just a drop in the bucket, he says. The amount of non-dollar holdings that will be repatriated isnt that great, he adds. Most of these earnings already are sitting in dollar-denominated accounts offshore and dont need to be converted into dollars, he explains.

Meanwhile, a potential further revaluation of the Chinese yuan is one factor that could work against the dollars continued rise in the months ahead, analysts say. Chinas economy is flexible enough to withstand a more freely traded currency, according to Zhou Xiaochuan, governor of the Peoples Bank of China.

China recently announced that it would loosen capital controls on multinational companies by allowing them to lend foreign exchange to their overseas subsidiaries. No timetable was announced for the change, however.

|

China Is Cautious |

|

China will move very cautiously in allowing the yuan to appreciate, says Marc Chandler of Brown Brothers Harriman. There is an old saying in China: To cross a river, step on the stones, he says. China is not fully using its existing trading band of plus or minus 0.3% in the yuan against the dollar, so there is no immediate need to widen the band, he asserts.

It is possible, however, that China will widen the permitted trading range slightly to about 0.5% sometime in the first half of next year, Chandler says. The Bank of Japan also will be cautious in ending its policy of quantitative ease, under which it has been flooding the banking system with reserves, he says. The Japanese central bank has made it clear that the end of quantitative ease will not imply an immediate increase in interest rates, Chandler says. First, it will begin slowly reducing its target for bank reserves. Only later will it set an interest-rate target greater than zero, and then it will move very gradually in raising short-term rates. Japans monetary-base growth rate has accelerated rapidly in recent months, which could be negative for the yen, according to currency analysts at Barclays Capital. Japans adjusted monetary base increased by 10.1% in October from the level of three months earlier, the highest growth since July 2003, according to the Japanese central bank. This could mean that the circulation of money in the banking system has increased due to the end of the banking-sector crisis and that an increase of bank lending is driving monetary growth higher, the Barclays analysts say. The more money that is printed, the weaker the yen is likely to become, they say. Elsewhere in Asia, Indonesias central bank raised its benchmark interest rate by 125 basis points to 12.25% on November 1, following a much sharper-than-expected increase in inflation. Indonesias consumer price inflation jumped to 17.9% in October when the government more than doubled fuel prices by ending subsidies that kept the countrys energy prices well below world levels. Analysts say the central bank had little choice but to act, for if it had failed to raise interest rates, the rupiah would have fallen further, putting even more upward pressure on inflation. |

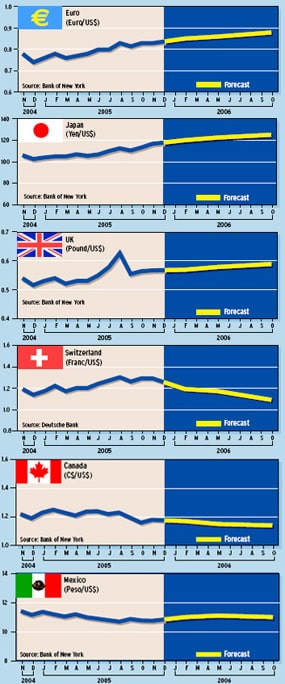

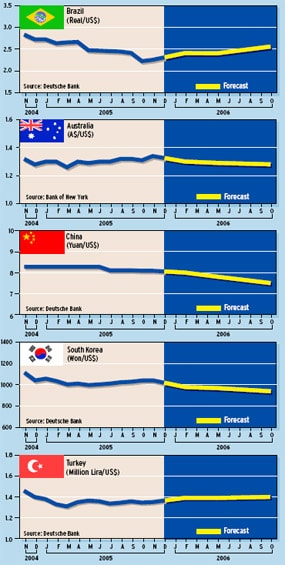

Currency Forecasts

Gordon Platt