THE AMERICAS

The US dollar fell 9.2% on a trade-weighted basis in 2002, and analysts predict further losses for the greenback this year, particularly against the euro.

Fears of a plunge in the dollar are overdone,however, despite the potential for a war with Iraq and worries about financing the bloated US trade deficit, currency strategists say.

Prospects for a durable US economic recovery are improving, while the euros rise could hamper Europes export-dependent economies, say analysts at Citigroup.And if there is a conflict in Iraq, it could depress Japans stagnant economy further due to rising oil prices, they add.

The dollar is probably less overvalued against the major currencies than many observers believe, says Gabriel de Kock, director of the economic and market analysis group at Citigroup in New York. The common perception that US industry has lost ground to European and Japanese competition as a result of dollar strength does not square with the facts, he says. Since the dollar bottomed in the mid-1990s, US exporters generally have maintained their share of the market for US exports, according to de Kock. Productivity gains have helped to offset some of the loss of competitiveness associated with the dollars rise, he says. US business-cycle leadership and the widest fiscal policy divergence in decades also suggest that the dollars potential to fall against the euro and the yen is limited, de Kock says. Others are less sanguine about the dollars prospects, however. Michael Rosenberg, head of global foreign exchange research at Deutsche Bank in New York, says that although aggregate US productivity growth surged in the second half of the 1990s, a large segment of the US economy did not participate in those gains.

While the dollar has fallen in the past two years, it is still significantly overvalued on a real, broad, trade-weighted basis, Rosenberg says. Despite the dollars recent declines against the euro and other leading currencies, it has risen in real terms against the Canadian dollar, the Mexican peso and the currencies of many emergingmarket countries with which the United States trades, he notes.

The US current-account deficit could widen to more than 6% of gross domestic product in the next 18 months, Rosenberg says.This could require a rather large exchange-rate adjustment to correct the external imbalance.

We look for the dollar to decline toward its fair value over the next two to three years and for the euro to rise to around $1.15 as early as the end of 2003, Rosenberg says.

Because the history of long cycles suggests that the dollar tends to overshoot, he adds, it would not be surprising to see the euro reach $1.30 or higher by 2005.

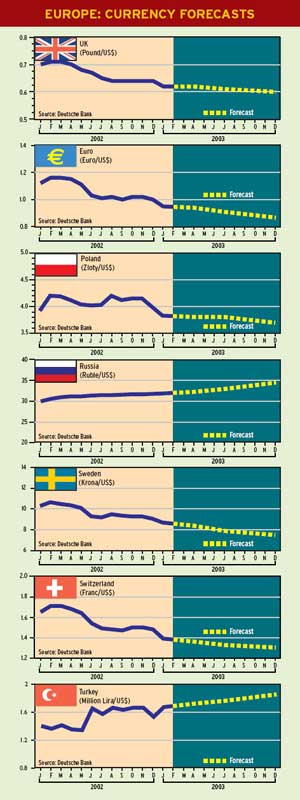

EUROPE

Central European Currencies Buoyant

Central European currencies are on a structural appreciation course that will accelerate over the next few years, analysts forecast.While Central European policymakers tend to talk their currencies down, this is only delaying the inevitable, says Thomas Browne, currency strategist at Deutsche Bank in London.

Foreign investors have consistently found assets in Central Europe to be cheap, Browne says.They can produce the same output for a lower cost than in Western Europe, and this has been the driver of foreign direct investment, he adds. Deutsche Bank forecasts that the returns from Central European currency exposure will range between 9% and 13% per year over the next three years.The ratification of the Nice Treaty at the end of last year heralds the enlargement of the EU by 10 new member states from 2004.

The economies of the prospective new members will converge toward the EU average, Browne says. We expect the appreciation path followed by the Czech koruna to be repeated over the next two years in Poland, Hungary and especially Slovakia, due to that currencys real appreciation lag, he says.

Browne says there is a latent suspicion that the Greek drachmas accession into the European monetary union was a contributor to the euros initial weakness.This is an experience that the European Central Bank does not wish to repeat, he says.

CEE countries have successfully weathered the economic slowdown that has hit the European Union, according to analysts at Vienna-based RZB. Over the next few months, however, it is increasingly likely that the overall economic conditions in each new EU member will once again come under increasing scrutiny, the RZB analysts say.

However, the strong downward trend in the volatility of Eastern European currencies has rendered stock and bond markets in the region considerably less risky for euro-based investors than they were just a few months ago, the RZB analysts note.

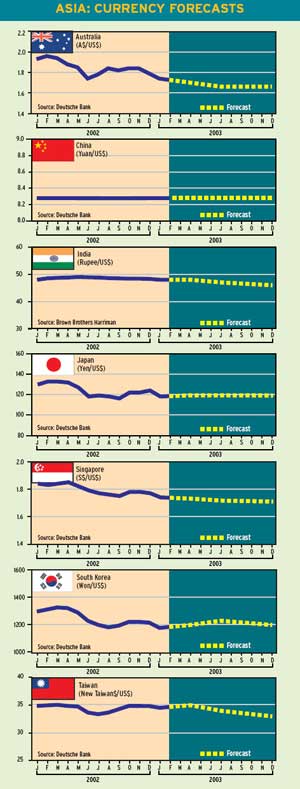

ASIA

Pressure Growing On China to Float

The debate on trade with China and the need for a stronger yuan will dominate the currency market this year, says Dennis Gartman, editor and publisher of the Virginiabased Gartman Letter, an advisory service.There has been a good deal of talk of late regarding the Chinese currency and the need to allow it to trade freely, he says.

Clearly the authorities in Beijing became annoyed in early January when rumors of an imminent revaluation swept through the market, Gartman says.The government moved quickly to downplay the rumors, he notes. While much of the rest of Asia is whining about the recent drop in the dollar, China may not be exposed, as it continues to peg the yuan at an arguably undervalued level, says David Gilmore, economist and partner at Essex, Connecticut-based Foreign Exchange Analytics.

So far, however, no one expects China to comply, he says.Oddly, Chinas help in finding a peaceful solution to the Korean crisis may just buy it another year of beggar-thy-neighbor policy, Gilmore says.

The bottom line is that as slow growth, low inflation, or even deflation in some countries, begin to take root in the global economy, everyone will want a weak currency, Gilmore says.And surely, simple arithmetic dictates that not all currencies can weaken, he adds.

Bank of Japan Leads Changing of Guard

At the beginning of the new fiscal year in Japan on April 1, the Bank of Japan will have a new governor and two new deputies.

The central bank will likely make inflation targeting, or attempting to achieve a modest increase in prices, a top priority after the retirement of governor Masaru Hayami, who failed to whip deflation with zero interest rates, analysts say.The Bank of Japan is expected to step up purchases of foreign bonds, mainly US treasury securities.

Besides Hayami, the current chiefs of the US Federal Reserve, the European Central Bank and the Bank of England are all set to step down in 2003. If Fed chairman Alan Greenspan does not opt for a fifth term, there lies the possibility of President Bush appointing a proponent of inflation targeting, says Ashraf Laidi, chief currency analyst at MG Financial, a New Yorkbased online currency trading firm.

This theme is being touted by newly appointed Federal Reserve Board governor Ben Bernanke, Laidi says. Inflation targeting would be dollar-negative, he adds.

Gordon Platt