CORPORATE FINANCING FOCUS

The shifting sands in the foreign exchange market in 2007 undermined the dollar to the extent that China openly weighed what its state media refer to as the “nuclear option” of dropping its vast holdings of US securities if Washington were to impose trade sanctions to force a quicker revaluation of the yuan. A weak dollar is not in the best interests of US creditors, who will be paid back in cheaper greenbacks.

The shifting sands in the foreign exchange market in 2007 undermined the dollar to the extent that China openly weighed what its state media refer to as the “nuclear option” of dropping its vast holdings of US securities if Washington were to impose trade sanctions to force a quicker revaluation of the yuan. A weak dollar is not in the best interests of US creditors, who will be paid back in cheaper greenbacks.

Meanwhile, Jassem Al-Mannai, chairman of the Arab Monetary Fund, based in Abu Dhabi, UAE, recommended that members of the Gulf Cooperation Council end their currency pegs to the dollar to give themselves more flexibility to combat rising inflation. He suggested that the GCC countries peg their currencies to a basket of currencies, including the euro, the British pound and the Japanese yen, or shift to a managed float.

The GCC declined to follow Al-Mannai’s advice at its summit meeting in Doha, Qatar, in December, with Saudi Arabia adamant about maintaining the current system. The dollar’s role as the world’s leading reserve currency, however, is looking less secure.

“Continued talk of repegging and revaluations is a reminder of the global impact of the decline in the value of the dollar, causing central banks and sovereign funds to rethink their positioning regarding reserve accumulation, currency regimes and oil pricing,” says Ashraf Laidi, chief foreign exchange analyst at New York-based CMC Markets US. “Such comments from China have been a veiled counter threat to the growing protectionist rhetoric by Democratic presidential candidates and the US Congress calling for restrictive legislation against China in the event that Beijing didn’t revalue its currency,” he says.

China, Japan Sell Treasuries

Both China and Japan, the largest holders of US treasuries, have reduced their holdings of these securities, with Japan’s total falling to a three-year low of $582 billion and China’s to a six-month low of about $397 billion at the end of the third quarter of 2007, Laidi says. This trend could continue in 2008 if the dollar weakens further, eroding the value of their reserves.

China announced in late November that its foreign exchange reserves, the world’s largest, had climbed to $1.46 trillion in October, up $21 billion in one month. However, that was the smallest rise since September 2006. After rising at about $45 billion a month in the first seven months of 2007, China’s foreign exchange reserves rose by just $23 billion in August and $24 billion in September 2007. The slowdown seemed to indicate the country was diverting its trade surplus away from US treasury securities and into stocks and corporate acquisitions controlled by its sovereign wealth fund.

It is not possible to determine from the data published by the US Treasury Department and the Federal Reserve exactly which foreign investors own US debt and how much is in foreign hands. It is clear, however, that the United States is vulnerable to sudden decisions by foreign holders to make large-scale sales of their dollar assets. So far, any selling that has been detected has been gradual rather than sudden.

US and China Rely on Each Other

“China is in a bit of a tough spot,” says Todd Crosland, chairman and president of Salt Lake City, Utah-based Interbank FX, a futures commission merchant specializing in the retail foreign currency market. “The US is China’s largest trading partner and has a significant trade deficit that has to be financed,” he says. The countries are locked in a mutually beneficial relationship that depends on the US buying China’s exports and China buying US treasury securities.

If either China or Japan were to aggressively sell some of their dollar holdings, it would only hurt the value of their remaining holdings, Crosland says. “While there has been talk of the euro gaining as a reserve currency, I do not see a significant shift happening,” he says.

China wants to avoid using the “nuclear option” of a mass liquidation of its vast holdings of US treasuries, says He Fan, a researcher with the Institute of World Economics at the China Academy of Social Sciences. However, he made it clear in a report in the China Daily newspaper that China has the power to trigger a dollar collapse. “China has accumulated a large sum of US dollars,” he said. “Such a big sum, of which a considerable portion is in US treasury bonds, contributes a great deal to maintaining the position of the dollar as an international currency.”

As long as the yuan is stable against the dollar, China is unlikely to shift its reserves out of dollars, He said. Nonetheless, “The Chinese central bank will be forced to sell dollars once the renminbi [yuan] appreciates dramatically, which might lead to a mass depreciation of the dollar against other currencies,” he told the China Daily. The yuan has appreciated by about 10% against the dollar in the past two years, and China has resisted international pressure to speed the pace of the yuan’s ascent.

|

|

Todd Crosland, chairman and president, Interbank FX |

Flight-to-Quality Lifts Bonds

A widespread sell-off of US treasury securities could drive down the prices of the remaining treasury assets held by the People’s Bank of China and cause substantial losses on further sales. Ironically, however, recent unsettled economic and financial conditions related to the US subprime crisis have encouraged flight-to-quality buying of US treasuries that has boosted prices of these bonds and lowered long-term US interest rates.

As the dollar fell to a record low against the euro in November, Cheng Siwei, vice chairman of the Chinese Peoples’ Political and Consultative Conference, said, “We will favor stronger currencies over weaker ones and will adjust accordingly.”

While this would seem to suggest that China is going to diversify its reserve holdings away from the dollar and was preannouncing this to the world, the country has no incentive to tip its hand, says Marc Chandler, global head of currency strategy at Brown Brothers Harriman, based in New York. “Instead, we suggest that what China and other central banks may be doing is diversifying the new reserve accumulations, not their [existing] stock of reserve holdings,” he says. “There is no compelling sign that China is really diversifying its massive reserves out of dollars,” he adds.

Agencies Offset Bond Sales

US agency and other dollar holdings have offset the lion’s share of the decline in China’s treasury holdings, according to Chandler. Central banks in Asia, and perhaps elsewhere, that are accumulating reserves in an effort to slow their currencies’ appreciation do so against the dollar primarily and then, with a lag, shift some of the dollars into other currencies, such as the euro and the British pound, he says.

The most authoritative sources for the allocation of reserves by currency are the International Monetary Fund and the Bank for International Settlements, according to Chandler. An important caveat, however, is that not all countries report the allocation of their reserves. The most recent data, which cover the second quarter of 2007, indicate that the dollar’s share of international reserves for which allocations are reported slipped to 64.8% on June 30, 2007, from 66.1% a year earlier. The euro’s share rose to 25.6% from 24.8%.

The most authoritative sources for the allocation of reserves by currency are the International Monetary Fund and the Bank for International Settlements, according to Chandler. An important caveat, however, is that not all countries report the allocation of their reserves. The most recent data, which cover the second quarter of 2007, indicate that the dollar’s share of international reserves for which allocations are reported slipped to 64.8% on June 30, 2007, from 66.1% a year earlier. The euro’s share rose to 25.6% from 24.8%.

“These figures would seem to show only the slightest shift in reserve diversification, and even this overstates the case,” Chandler says. When the dollar declines, central banks that hold dollars see their dollar proportion of reserves decline even if they don’t make any shifts in their holdings.

The dollar’s share of central bank reserves is fairly constant at around two-thirds, while the euro’s share is generally steady at around 25%, Chandler says. Meanwhile, the decline of the dollar is not adversely affecting the US economy, he says. “If anything, it is helping it to substitute foreign demand for slackening domestic demand,” he says.

Is End of Cycle Near?

“While we should be prepared for a weaker dollar in the near term, the dollar’s downturn is getting long in the tooth,” Chandler says. The dollar has been declining against the euro since the fall of 2000, the last time the major central banks of the developed countries intervened in the foreign exchange market.

Fears that a continuing decline of the euro could ignite a global financial crisis prompted the financial authorities of the Group of Seven industrialized nations to conduct a coordinated intervention in September 2000. The coordinated action lifted the euro from 85 cents to the dollar to around 90 cents. The single currency was introduced in January 1999 at a rate of $1.17.

“We assume the dollar’s [current] decline is largely cyclical in nature, having to do with the fact that diverging monetary policies and interest-rate differentials are moving decisively against the US,” Chandler says. “This dollar cycle does not appear unique.”

The main weight on the dollar is not the US current account deficit, the dollar’s role as the numeraire for the world economy and its status as the predominant reserve asset, Chandler says. “Instead, we see the weakness as largely cyclical in nature, having to do with the divergence in the monetary cycles among the major industrialized countries,” he says.

GCC Stands Pat on Pegs

The Gulf Cooperation Council, comprising the United Arab Emirates, Qatar, Kuwait, Bahrain, Saudi Arabia and Oman, concluded its annual summit meeting in Doha, Qatar, in early December without making any change in their dollar pegs or announcing any revaluations, despite forecasts by many analysts that there would be a coordinated move to a new currency regime.

Iran’s president Mahmoud Ahmadinejad spoke at the summit, becoming the first Iranian head of state to attend the conference. The GCC leaders agreed to stick with the 2010 date set earlier for the launch of a single GCC currency. They also reaffirmed their plan to launch a common market on January 1, 2008.

“The Gulf common market aims at realizing one market through which GCC nationals benefit from opportunities in the Gulf economy and opening broader spheres for inter and foreign investment,” said the Doha Declaration issued at the end of the two-day summit. The declaration said the common market would help realize the most efficient use of resources, improve the negotiating status of the GCC states and enhance their influence in international economic groupings.

Earlier, Saudi finance minister Ibrahim Al-Assaf ruled out cutting the riyal’s peg to the dollar. “We will not drop it. That’s it,” he told reporters after a meeting of GCC finance ministers.

Not on the Agenda

Qatari finance minister Youssef Hussein Kamal said, “We did not raise the issue of de-pegging at all. It was not on our agenda.” He suggested that countries in the region should be in no hurry to change their currency regimes, since the dollar may rebound in the next 18 months. Kamal noted that the main source of inflation was not coming from imports but from soaring rents.

“Imagine what would happen if in order to (mistakenly) curb inflation, a country lowers the weighting of the weakening dollar and increases the weighting of a strong currency like the euro, just as the euro’s seven-year upward trend ends,” says Chandler of Brown Brothers Harriman.

GCC member Kuwait unilaterally dropped the dollar peg in favor of a basket of currencies in May 2007. The Kuwaiti dinar appreciated by a little more than 5% between then and early December. Meanwhile, Kuwait’s inflation surged to 6.2% year-over-year in September 2007 (in the latest figure available) from 4.8% in August. Rising housing costs were a critical source of the country’s inflation, according to Chandler.

The more that GCC-member countries take unilateral action in terms of their currency regimes, the less credible is the prospect for monetary union in 2010, Chandler says. Unilateral revaluations would not be as much of an obstacle to monetary union as the currency-basket approach, he says.

Oil-Pricing Debate

Saudi Arabia fought off an attempt in November by Iran and Venezuela to convince the Organization of Petroleum Exporting Countries to discuss pricing oil in different currencies than the dollar.

Meanwhile, Russia’s state-run Gazprom, the world’s largest natural-gas exporter, said it might start selling its crude oil and natural gas production in rubles rather than dollars and euros. “We are seriously thinking about selling our resources in rubles,” Alexander Medvedev, Gazprom’s deputy chief executive, said on a visit to New York in late November. Andrei Kruglov, the company’s chief financial officer, said the switch would happen “sooner rather than later.”

Russia is the world’s second-largest exporter of crude after Saudi Arabia. “In keeping with the rising world demand for rubles, our currency can become one of the reserve currencies [of the world] and a currency for other centers of economic development,” Medvedev says. He acknowledges, however, that the goal won’t be reached in the short term.

Role of Interest Rates

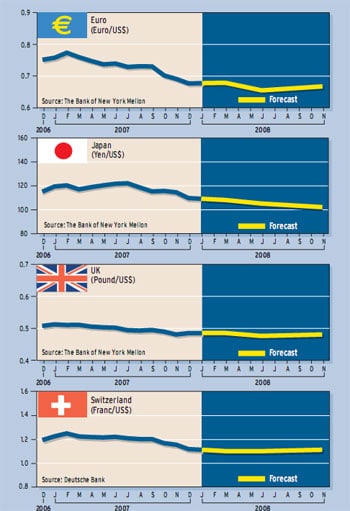

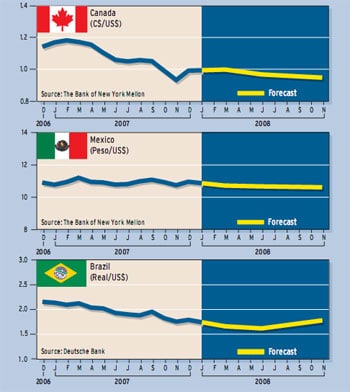

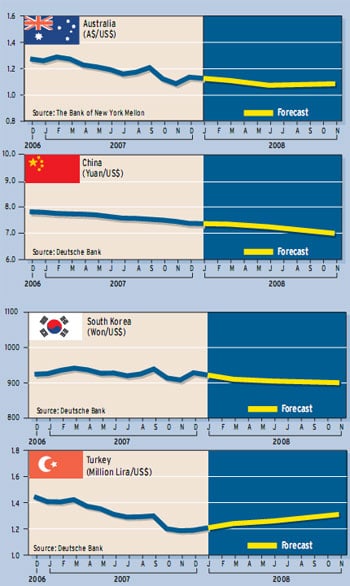

Forecasts of a dollar rebound in 2008 are becoming more frequent as the US current account and budget deficits continue shrinking, says Laidi of CMC Markets US. “The dollar is unlikely to pursue single directional moves against the major currency pairs in 2008, as was the case in 2007,” he says. “The extent of the dollar rebound will largely depend on the scope of interest-rate cuts in Europe, Canada and Australia, serving as an offset to further rate cuts by the Fed,” he says.

“The main reason we expect any dollar rebound to be relatively limited is the nature of the interest-rate cuts,” Laidi says. The Federal Reserve’s rate cuts expected this year would be aimed at treating structural problems, such as falling bank credit and a deepening housing recession, an increasingly weak commercial property market and weakening consumer demand, he says. Meanwhile, any rate cuts from the European Central Bank, the Bank of Canada and the Bank of England are expected to address temporary cyclical issues, such as slowing business activity and reduced aggregate demand, according to Laidi.

The dollar is undervalued by many measures, analysts say. “We expect the dollar’s multi-year decline to come to an end in 2008 as markets begin to reward the US for pro-growth policies and to anticipate that other central banks will reduce interest rates,” a report by Brown Brothers Harriman says.

Gordon Platt