Kuwait | Country Report

Kuwait is at a crossroads. Despite huge financial reserves, the Persian Gulf state must speed up project implementation to revive a stagnant economy far too dependent on oil revenues.

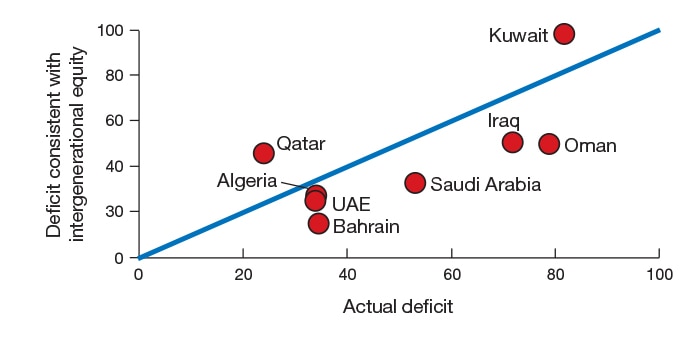

Kuwait can lay claim to the world’s first and oldest sovereign wealth fund—the Kuwait Investment Authority, with $410 billion in assets, according to the Sovereign Wealth Fund Institute. Yet part of its investment objective, to provide security for future generations, looks like an increasingly shaky proposition unless reforms are undertaken to boost the non-oil economy. Kuwait is hugely dependent on oil revenues, estimated by the International Monetary Fund to account for 95% of export revenues and government income. Paradoxically, despite vast riches Kuwait is the least efficient country when it comes to saving enough nonhydrocarbon wealth for future generations (see chart page 24).

In its regional outlook, published in October, the IMF forecasts that Kuwait’s GDP will grow by 1.8% in 2015—way below the average of 4.8% it achieved between 2000 and 2010. With the IMF predicting GDP growth will average 4.5% in the Gulf Cooperation Council (GCC) countries, Kuwait is the economic laggard. Still, with forecast oil output at 2.9 million barrels a day in 2015, it has and will continue to have substantial capital buffers to protect it from any further deterioration in crude oil prices. At $54 a barrel, Kuwait has the lowest fiscal break-even price of its oil-producing neighbors in the GCC and scarcely any borrowing. Total government debt will amount to just 3.1% of GDP in 2015, the IMF estimates. Even so, there is uncertainty over oil prices, and Capital Economics in London calculates Kuwait will swing into deficit if prices fall below $70 a barrel. That, according to Kirk Sowell, a specialist in Middle East political risk and principal at political risk firm Uticensis Risk Services, would be a shock to the system. “Kuwait has massive cash reserves, so it isn’t on the brink of insolvency, but deficit spending in reliance on the reserves would be an indignity.”

|

|

|

ECONOMIC LIBERALIZATION

Coping with a deficit is one thing, but any more delays in public spending will hold back much needed investment in energy, transport and health infrastructure. The 30 billion Kuwaiti dinars ($107 billion), five-year development plan announced in 2010 has faced repeated delays, owing to squabbling between government and parliament. In August a new five-year plan was launched. It should see renewed activity in stalled projects such as the metro and rail plans, according to Standard Chartered. However, with ample global supplies of oil there is little scope for Kuwait to increase oil production—meaning economic growth will remain sluggish. Investors have taken solace from the government’s decision to suspend the controversial offset program, but according to analysts, it is far from clear whether it will lead to an increase in foreign investment.

Farouk Soussa, Middle East chief economist at Citi, argues the decision depends on the government’s ability to implement projects on the ground. “This requires a big step-up in the budget execution rate, as well as a more stable political environment in which contracts awarded to foreign companies are not subjected to the ever-present risk of review and abrogation.”

New rules are due to be revealed in the next six months say authorities. The offset program has been an obstacle to investment, particularly for smaller investors who do not have the economies of scale to shoulder additional costs demanded by the program. An inefficient bureaucracy has clearly curtailed foreign direct investment, with the 2015 World Bank Doing Business survey ranking Kuwait 86th out of 189 countries for ease of doing business, 150th for starting a business and 131st for enforcing contracts. In 2013, FDI to Kuwait fell to $2.3 billion, according to Standard Chartered.

Nevertheless all the signs are Kuwait’s government wants to ramp up project execution and forge a better working relationship with parliament. That is crucial if legislation like the build-operate-transfer program of the public-private partnership initiative is to succeed. Citi’s Soussa says it is a step in the right direction. “The new build-operate-transfer law clarifies the legal framework for participation in PPPs and is encouraging for new investors in that it allows for a longer investment horizon. That said, there are concerns that in restricting the right to extend, current investors have, de facto, had their investment horizon expectations cut, and this could result in legal challenges.”

DEFICITS RELATED TO THE NONHYDROCARBON ECONOMY |

| (Nonhydrocarbon primary deficit, % of nonhydrocarbon GDP, 2013) |

|---|

Sources: National authorities and IMF staff calculations.

x axis = Current Deficit (2013)

y axis = Intergenerational equity deficit

SOLID BANKING FUNDAMENTALS

Kuwait’s banking sector reported total assets of 51 billion dinars as of December 31, 2013—equivalent to 100% of GDP, says Moody’s Investors Services. It comprises 16 commercial banks, six Islamic banks and one specialized banking institution. National Bank of Kuwait and Kuwait Finance House hold the largest share of total system assets, with respective shares of 31% and 27%. All financial institutions are regulated by the Central Bank of Kuwait.

Kuwaiti banks operate in a favorable business environment amid expectations of increasingly supportive fiscal policies for the non-oil sector that should spur commercial and lending opportunities. There is optimism among banks that the new five-year plan will have momentum. “We sense the government’s determination for a speedier implementation of this new plan, (and) we have started to see implementation of the plan already—the refinery project, Kuwait airways fleet and bridge projects are works in progress,” says Bashir Jaber, head of group corporate communications and investor relations at Burgan Bank in Kuwait. “The banking sector is ready and capable to support when projects reach financing stage,” adds Jaber.

It is a point echoed by Alexios Philippides, an analyst at Moody’s Investors Service in Limassol, Cyprus, and co-author of a November report on the Kuwaiti banking system. “Political deadlock is the main downside risk,” he says, “but we see positive indications; the new 2013 parliament seems friendlier, and that is encouraging for policy implementation.” He says there is a positive outlook for credit growth in the next two to five years. According to Philippides, bank credit growth surged to 8% in 2013 against a compound annual growth rate of 3% between 2009 and 2012. In January 2014, Kuwait adopted the Basel III framework, which mandates higher capital requirements. The new capital requirements will be fully phased in by 2016. However, some analysts question whether broader reforms in the business sector will get off the ground at a time when the government is reducing subsidies. “The key risk to Kuwait’s economy is for the pattern of undershooting capital spending and delaying development projects to continue in 2015, weighing on non-oil growth and further slowing down Kuwait’s path to reach a diversified economic base,” says Carla Slim, Middle East North Africa economist at Standard Chartered in Dubai. In the short term, investors will have to determine whether that means the glass is half full or half empty.

GFmag.com Data Summary: Kuwait

Central Bank: Central Bank of Kuwait |

|||

|---|---|---|---|

|

International Reserves |

$35,242 billion |

||

|

Gross Domestic Product (GDP) |

$175,787 billion |

||

|

Real GDP Growth |

2011 10.2% |

2012 8.3% |

2013 -0.4% |

|

GDP Per Capita—Current Prices |

$45,188.56 |

||

|

GDP—Composition By Sector* |

agriculture: 0.3% |

industry: 50.6% |

services: 49.1% |

|

Inflation |

2011 4.9% |

2012 3.2% |

2013 2.7% |

|

Public Debt (general government |

2011 8.5% |

2012 6.8% |

2013* 6.1% |

|

Government Bond Ratings |

Standard & Poor’s AA/Stable/A-1+ |

Moody’s Aa2 |

Moody’s Outlook STA |

|

FDI Inflows |

2011 $3,260 million |

2012 $3,931 million |

2013 $2,329 million |

* Estimates

Source: GFMag.com Country Economic Reports, IMF

PRIVATE-SECTOR REFORMS FAVOR BANKING SECTOR

There is an air of optimism in the banking community in Kuwait that this time things will be different. With the recently enacted five-year plan and after years of political wrangling, bankers detect a concerted effort to liberalize the economy. With GDP per capita of more than $45,000, according to the IMF, their confidence looks compelling. “We do sense the government’s determination for a speedier implementation of this new plan,” says Bashir Jaber, head of group corporate communications and investor relations at Burgan Bank.

Alexios Philippides, an analyst at Moody’s Investors Service, says the optimism bodes well for the sector, assuming the government can break free of the political inertia that has stalled project execution. “If there is greater private-sector participation by international companies, they will require domestic banking relationships, which will be generally positive for banks in Kuwait.” That scenario is also likely to boost credit growth, which Moody’s estimates could reach 10% over the next year.

It is the prospect for corporate credit growth that excites analysts, as the private sector accounts for a small share of all loans. They cite trade and construction as potential growth markets that were early beneficiaries of previously deadlocked infrastructure projects, but for the moment high public-sector wages will continue to drive demand for consumer loans. In the past, loans provided for the purchase of securities proved disastrous, but there has been a marked improvement in asset quality, with nonperforming loans at 3.5% of total loans in June 2014, down from 4.6% in June 2013, according to the Central Bank of Kuwait and the IMF. Additionally, Kuwaiti banks are very well capitalized, with an average capital adequacy level of more than 18%, says the Central Bank of Kuwait.

The well-documented rise of Islamic finance traditionally centered in Bahrain has recently seen growing competition from Dubai. Yet according to Qutayba Al-Bassam, senior manager, corporate communications, at Boubyan Bank, demand for shariah-compliant financial services is showing strong growth in Kuwait. He cites the increase in market share of Islamic banks, which reached 41.5% in 2013, up from 39% in 2012. Shariah-compliant financial services in the consumer sector are also performing well, with 45% of salaried Kuwaitis transferring their salaries to Islamic banks, up from 37% in 2009. That increase has been reflected in the rapid expansion of bank branches, which have grown at five times the rate of conventional banks, according to Al-Bassam. In 2014, Islamic banks constituted 41% of the Kuwaiti branch network.

Attention is also focused on the Kuwait Stock Exchange, one of the oldest in the Middle East, and whether, following neighboring Saudi Arabia’s decision to allow direct foreign investment on the Tadawul, Kuwait will open its market to institutional investors outside of the Gulf Cooperation Council. There has been no indication that will be the case, but banks in Kuwait would be well positioned to take advantage of such a development.

PROPOSED INSOLVENCY LAW PAVES WAY FOR FDI

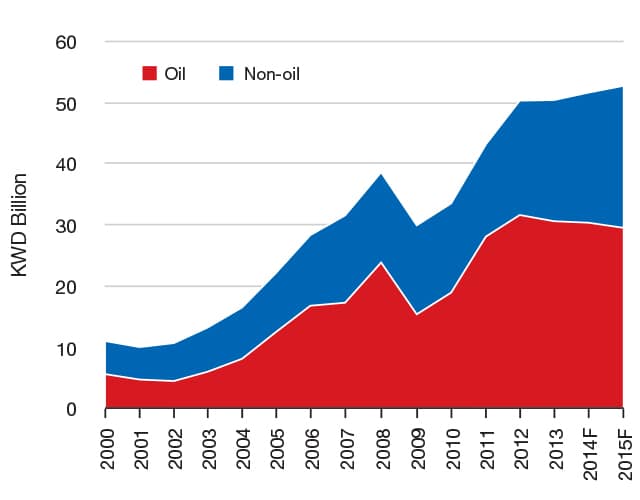

Kuwait, unlike its Gulf neighbors in the UAE and Qatar, has been slow to diversify its economy away from dependency on oil revenues. There is a certain logic to that course, as it still has around 89 years in crude and gas reserves at the current rate of production. Yet if Kuwait is to develop a thriving private sector, improvements are needed in the quality of political, administrative and legal institutions, particularly if it wants to attract foreign investment. The news that Kuwait is finalizing an insolvency law could radically alter the investment climate and, depending on timing, would be the first such law in the Gulf Cooperation Council. To be fair, the non-oil sector is gradually contributing a larger share of GDP, and there is an expectation it will gather pace in 2015 (see chart).

Supporting that drive are bodies such as the recently created Kuwait Direct Investment Promotion Authority (KDIPA), which was set up to be a one-stop shop for attracting foreign investment, replacing the Foreign Direct Investment Office. However, analysts say the agency charged with overseeing the new direct investment promotion law is still deciding upon its remit, which will no doubt concern investors. Indeed the KDIPA itself says it has yet to finalize legal, administrative and financial requirements, as well as executive regulations. The Authority has its work cut out. The economy lacks competitiveness, which is reflected in lackluster foreign direct investment inflows when benchmarked against regional peers. In Transparency International’s 2014 Corruption Perceptions Index, Kuwait ranked 67 out of 175 countries, the lowest in the GCC, compared to the UAE at 25th.

Nevertheless, the outlook for FDI in the energy sector is encouraging, says Farouk Soussa, Middle East chief economist at Citi. “A large focus of the development plan is in the energy sector, particularly in power generation, so prospects there look particularly good.” Aside from exploration, it is likely energy infrastructure will be the core of FDI, rather than upstream refining. Although Kuwait is largely immune from the rout in oil prices, some analysts say the pricing environment may help when it comes to speeding up reforms. “The decline in oil prices might be a good thing and get the government to take action sooner rather later,” says Steffen Dyck, vice president and senior analyst at Moody’s sovereign risk group in Singapore.

Yet, even with oil prices as they are and pressure to develop the private sector, there are still investment opportunities in exploration, says Carla Slim, Middle East North Africa economist at Standard Chartered: “We expect growth to be driven by the non-oil sector, while the oil sector’s performance is set to remain flat. Investments to expand oil production capacity in the next five years should help support the government’s initiatives in investing in its own economy.” Kuwait is also expected to invest in Iraq’s energy sector.

The trouble is, for all of the planned initiatives Kuwait has a reputation of being a difficult place to do business—largely because of a challenging bureaucracy and institutionalized skepticism of foreign investment. In 2015 it will need to work to overcome this reputation.