EXCHANGE-TRADED DERIVATIVES PROVE THEIR WORTH

As product offerings grow and pricing improves, exchange-traded derivatives are increasingly appealing to both corporate and institutional buyers of derivatives contracts.

By DENISE BEDELL

Of the lessons learned by companies during the recent financial meltdown, one of the most painful has been that strong risk management and good control and compliance are more important than ever. Hedging risk through derivatives contracts is a key component of corporate risk management strategies, even as some derivatives products—such as credit default swaps (CDS)—continue to take a beating in the press due to their perceived lack of stability during times of financial upheaval.

However, many of the problems that have faced the derivatives markets have appeared in the over-the-counter (OTC) derivatives market rather than in products traded on a derivatives exchange. OTC derivatives contracts are non-standardized and traded directly between market participants. In contrast, exchange-traded derivatives (ETDs), also known as listed derivatives, are standardized derivatives contracts regulated by the Commodity Futures Trading Commission (CFTC) that are traded on a regulated exchange.

As a result, companies using derivatives contracts for risk management purposes, and financial firms and asset management companies looking to trade them, are increasingly viewing exchange-traded derivatives as a valuable proposition—and with some similar motivations. Both financial and non-financial firms are seeking better counterparty risk management, and both are looking for greater transparency.

Derivatives exchanges provide both, but at the loss of some flexibility, as products must be relatively standardized and go through rigorous regulatory scrutiny before being launched on an exchange. However, as more products come on offer, as the strength of the model is repeatedly proven and as the price differential between ETD contracts and OTC contracts shrinks, exchange-traded derivatives are increasingly finding favor among the participants in many different market segments.

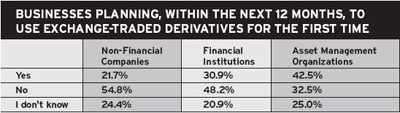

In a March 2009 survey of Global Finance subscribers, of those firms that are already using ETDs, 17.6% of non-financial companies, 26.1% of financial companies and 35.5% of asset management companies said they would increase their use of exchange-traded derivatives in 2009. In addition, more than a fifth of non-financial respondents that had never used ETDs before plan to try them out this year. Over 30% of financial firms and more than 40% of asset management firms that had never used them also mean to give them a go in 2009. Those are astounding figures at a time when most companies globally are hunkering down and either playing the waiting game or going for tried and tested products in their derivatives portfolios.

However, the reason for these figures becomes clearer when considering where much of the value lies in the exchange-traded product: transparency. With counterparty risk of prime concern to corporates in a post-Lehman world, transparency throughout any and every financial trade is essential.

EXCHANGES PROVIDE CLARITY

As the effects of the market crisis continue to be felt, regulators are looking for greater clarity and transparency into the use of all financial products while businesses are finding they need to know more detail than ever about the derivatives they employ. Regulators are asking for more information for audit compliance purposes and generally demanding greater detail about companies’ derivatives actions, according to Wolfgang Koester, CEO of RimTec, a provider of execution and documentation software for hedging management. “Instead of simply saying they have so much of derivatives on the books, the SEC wants to know why and what is the real effect,” he says. As a result, derivatives buyers are taking more interest in exchanges.

From an institutional investor perspective, the solid performance of the exchanges throughout the crisis and the resulting closing of the pricing gap between exchanges and derivatives sold over the counter are probably the biggest draws.

While its popularity is growing, the exchange-traded derivatives market has suffered as a result of the crisis. Jeff Howard, head of Americas futures and options sales and trading at Bank of America Merrill Lynch, notes: “Volumes are down significantly in 2009 year-on-year after a record year in 2008. This year will be challenging, and likely the first half of 2010 will be as well, but by the second half of 2010 we think the listed derivatives space will be a significant growth area.”

Some believe it will prompt increased diversity in listed products, as more OTC products are developed. “The listed [exchange] business has been a model which has proven to function well during this whole crisis,” says Gonzalo Chocano, global head of the futures and options group at Bank of America Merrill Lynch, “and that is what is making it more interesting for other OTC businesses to replicate this model and go through an exchange to clear business.”

Exchange-traded products traditionally have been more expensive because of the regulatory approval process and scrutiny in place from the CFTC, but that may be set to change. Carolyn Jackson, counsel at Allen & Overy, says, “In the OTC markets, provided a transaction satisfies an exclusion or exemption under the Commodity Exchange Act, there are few impediments to developing new contracts.” But, she adds, “For the first time since 2000, exchange-traded derivatives could be at a cost advantage versus their OTC brethren because there will be a huge regulatory cost to comply with whatever the OTC market does eventually look like.”

“The exchanges continue to roll out new products; some are slow to take hold, and others aren’t,” says Bank of America Merrill Lynch’s Howard. “We have seen three-year treasury and seven-year swap futures contracts, and the exchanges are always looking at new equity index products, such as the MSCI equity indexes.”

Eurodollar contracts on exchanges used to be only three to six months, but now they can go out as much as 10 years, showing the innovation and flexibility coming into the exchange-traded market.

CME Group, for example, began offering three-year treasury futures contracts on the Globex exchange on March 22. The contracts were sized at $200,000, and the first quarterly maturity to trade was the June 09 contract. CME Group is looking at adding options on the futures contracts at some point. The last time CME Group launched a treasury-tied future was in 1990. In addition, the exchange-traded market has seen much interest recently in the development of disaster contracts, weather contracts and pollution-related contracts.

According to the Global Finance survey, non-financial firms are interested primarily in FX derivatives products for hedging foreign exchange risk, followed by commodity hedging products and interest rate products. Financial institutions are mostly looking at FX, interest rate and equity products, and asset managers are interested in equity and commodity contracts, followed by energy and interest rate derivatives contracts.

As a result of the crisis and the negative publicity given to some OTC products, such as CDS, derivatives market participants are waiting to see what will change from a regulatory perspective and how that will affect both the OTC and exchange-traded derivatives markets. “We have been having a lot of conversations with exchanges and clients [about] the interest rate swaps market and the CDS market,” says Bank of America Merrill Lynch’s Chocano.

REGULATORY CHANGES LOOM

|

|

Koester: Regulators are looking for more information about derivatives exposure |

Allen & Overy’s Jackson explains that the current US regulatory proposals range from ensuring all products are cleared through regulated clearing organizations to mandating that they all be traded on regulated exchanges. “But if you are going to force OTC contracts to be cleared through a regulated clearing house, then inevitably OTC products must become more standardized,” she says. “If that were to occur, although technically they would still be OTC products, they would move closer to an exchange-traded structure.”

“What ideally would make sense with any new legislation is to create more transparency,” says Joel Telpner, a partner at law firm Mayer Brown. “Transparency is a good thing, and all legislative efforts will have as an underlying goal more transparency—more reporting and better ideas of notional exposures and where they lie.”

“Beyond that, ideally, new regulation would look at the leverage that was facilitated by derivatives contracts and change how we regulate capital and margin requirements, the ability to do leveraged transactions involving derivatives and how we use derivatives,” adds Telpner. “We should focus more on the leveraged component and capital reserve requirements with respect to that type of leverage. That is less likely to happen.”

What is more likely, Telpner says, is that derivatives will be redefined in a way that brings them more directly under the regulatory remit of the SEC or CFTC. “We will see changes to clearly define them as securities and/or commodities so regulators will have more statutory authority to demand more transparency in reporting, and so on,” he says.

|

|

Jackson: “Exchange-traded derivatives could be at a cost advantage” |

US regulators recently announced a proposal to initiate federal oversight of major OTC derivatives dealers and require some credit default swaps and other OTC derivative products to be traded on exchanges. However, some fears have been raised in the market that this could end up reducing or eliminating the flexibility—and hence much of the value—of OTC derivatives. In addition, market makers in the derivatives space are contesting a US Treasury proposal to end preferential tax treatment.

However, regulatory discussions take time both to consider and to implement. And the issue of SEC versus CFTC oversight may be moot should the two entities merge into a super-regulator, as has also been discussed.

There is no doubt that credit derivatives are seen as the most vulnerable of the OTC derivatives—partly as a result of all the bad publicity that they received over the course of the crisis. However, there are a number of practical issues in clearing credit derivatives that must be overcome both for domestic markets and for international clearing where, for example, one counterparty is in the United Kingdom and one in the United States.

Other OTC products could have fewer regulatory issues for central clearing—particularly those that are the easiest to value, such as interest rate and currency derivatives. Says one lawyer, “Although they are not necessarily standardized, one could envision a contract to be cleared or exchange-traded or both.”

>As the dust settles, it is hoped that regulators will continue to acknowledge the importance of both the OTC and exchange-traded markets and recognize that in certain instances OTC products provide hedges that cannot be replicated in the exchange-traded markets. As the regulators get a handle on the exchange-traded market, though, it should help corporations realize the value of derivatives as risk management tools rather than simply as risks.