Dealing with the regulatory complexities faced by their larger peers and without some of the flexibility of their smaller brethren, US regional transaction banks are building international partnerships and investing in best-of-breed technology platforms in order to win, and hold on to, corporate clients.

US regional banks face significant challenges. Along with those that transaction banks of all sizes are dealing with—increasing regulation and globalization, competition from technology vendors, heightened expectations from clients regarding the technology they can offer—they are also feeling pressure from community banks and the large, global banks. Even so, some regional corporate banks are not only surviving but thriving. They are investing in systems, providing expertise and developing networks and relationships that allow their business clients to succeed around the globe.

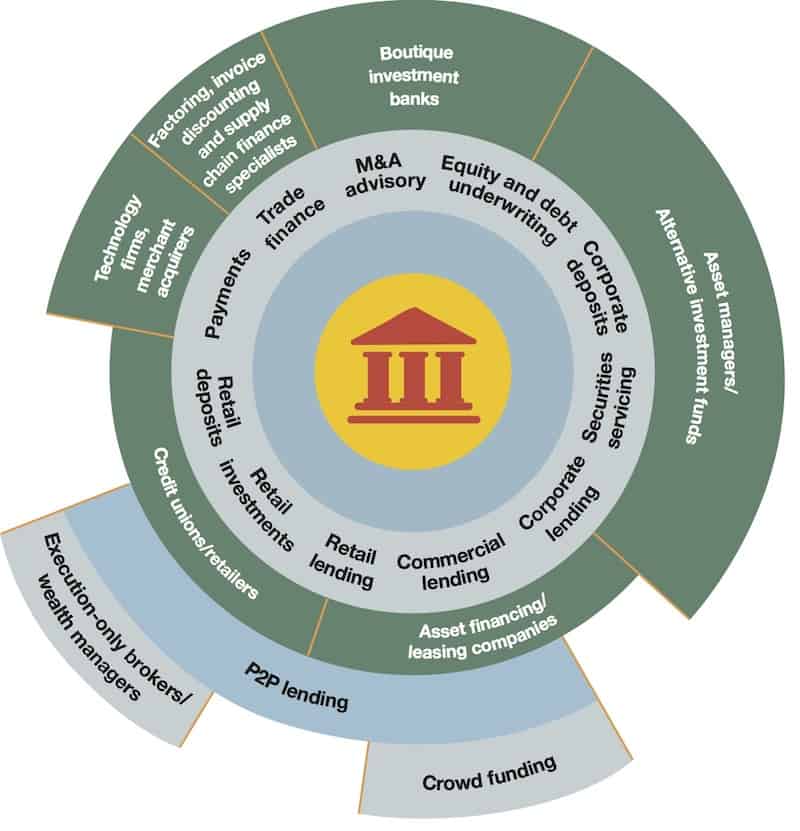

Among the more noteworthy obstacles regional banks must tackle is heightened competition from their global banking counterparts. As some multinational companies have turned to the capital markets for more of their financing needs, many global banks—the institutions that traditionally would serve these clients—have become more adept at servicing smaller corporate clients, says Alan Thompson, managing partner with consulting firm Bank Solutions Group.

“As the global banks move down-market in terms of the size corporates they are targeting, regional banks are having to respond,” says Gareth Lodge, senior analyst with Celent’s banking practice. Lodge points to many regional banks’ investment in payment hubs—a solution global banks offer—as one indication of this.

At the same time, many community banks can tout their ability to make decisions on the spot and to arrange meetings between business owners and their bank presidents. These are promises few regional banks can offer.

The upshot? “Regional banks are getting squeezed on both sides,” Thompson says. Competition is also appearing from new institutions and technologies, he adds. “Today almost every product line has a significant” nonregulated financial institution competitor, such as Apple Pay or Square. Moreover, it’s not yet clear how much regulation will be brought to bear on these new market entrants, he says.

REGULATORY SQUEEZE

In contrast, the regulatory environment in which all banks operate is becoming increasingly onerous. “Government policy and regulatory policy in general is affecting the industry more than normal,” says Bill Isaacs, senior managing director with FTI Consulting, a global business advisory firm.

And banks face regualtory challenges in their operations outside the US, as well. A number of countries either have adopted or are in the process of adopting Basel III, which sets new, higher capital requirements for many banks. In addition, many countries, such as the United Kingdom, are beefing up other regulatory efforts. “What happened in 2007 and 2008 scared everyone,” Thompson says.

Another shift is the increasingly global aspirations of many small and midsize companies. “We’re definitely seeing more activity with many companies from an international perspective,” notes Jeff Jones, executive vice president, global treasury management, U.S. Bank. Even companies that don’t have operations in other countries often work with clients or suppliers located outside the US.

While regional banks, like their smaller and larger competitors, face myriad challenges, many are nonetheless succeeding. They’re attracting more clients of all sizes by providing the expertise, tools and networks that can help them conduct business in multiple regions of the world.

Many midsize companies look to their banks for knowledge and insight, says Yaminah Sattarian, vice president, treasury and international services, with Keybank. In addition to working with clients one-on-one—say, advising on the documentation that will reduce the risk that a transaction fails—Keybank hosts boot camps in various cities on such subjects as global trade and foreign exchange, Sattarian explains. “We’ve actually doubled our revenue in global trade in the past year and expect that to continue.”

Many regional banks are also investing heavily in their technology offerings. For instance, SinglePoint, U.S. Bank’s primary cash management portal, lets treasurers and CFOs see the cash in- and out-flows not only at their U.S. Bank accounts, but also at those with their other banks, Jones says. “They have visibility into what’s taking place in all accounts.”

COMPETITION IS INCREASING ACROSS THE UNIVERSAL BANKING VALUE CHAIN

Multibank solutions that were once a key differentiator of global banks are now increasingly offered by next-tier institutions. This is key, as customer service on its own no longer is enough to attract and retain corporate clients, no matter the size of the bank, Thompson says. “You need products and technology.”

Indeed, best-of-breed systems and solutions are now expected by corporate clients. Nanette Crocker, executive director, corporate and investment banking, corporate treasury management, with BBVA Compass, notes: “Four years ago they might [have been] surprised at what we had. Now they recognize we’re committed to the market, and we continue to develop what they need.”

Many regional banks are also building their global networks. In some cases, they have a corporate presence in other countries—for example, BBVA Compass benefits from its affiliation with Spanish parent BBVA’s European and Latin American operations.

Even when a regional bank doesn’t have its own employees on the ground in a specific country, it often establishes partnerships or correspondent relationships with banks in the region. Through their partner banks, many regional firms can conduct transactions that a bank headquartered outside the country, even if it has global operations, might not be able to do, Sattarian says.

U.S. Bank works through networks of banks, such as IBOS, an international network that provides local banking services across the globe. Each bank within the network uses standardized operating procedures to, for instance, open an account. That streamlines the process for companies, Jones points out. The banks also adhere to service level agreements.

At the same time, each bank knows the regulations and policies within its country. “They have significant expertise on the ground,” Jones says. Companies who aren’t based in the region gain access to this expertise.

Regional banks also are benefiting from several broader shifts in the market. Many global banks are finding that “trying to be all things to all men in all markets is not viable long-term,” Lodge says. At the same time, a growing number of companies appear to be giving regional banks a new look. Crocker notes: “I think they’ve realized it doesn’t require a top-three [in size] bank to do business” around the globe. If you have the capabilities and have a relationship, they give you an opportunity.”

Regional banks that can meet the challenges can succeed. “I’m optimistic, although it’s a tough market,” Isaacs says, adding, “the industry has a place in the financial system.”