The pandemic spurred financial institutions to ramp up technology upgrades and add new services at record speeds.

From Brazil to Belarus, the Covid-19 pandemic unleashed a wave of innovation across banking and financial services. While the recent global financial crisis saw the rise of fintechs, now the lines between banks and technology companies are becoming increasingly blurred.

Banks are now innovating beyond the traditional realm of banking services, particularly in areas such as financial literacy and education, and in the provision of e-commerce and e-enablement platforms to help small businesses start their digital transformation journey. Customer experience is the new battleground among banks, software companies and fintechs.

This year’s innovators across cash management; trade, Islamic and corporate finance; and payments, demonstrated a renewed focus on speed to market, ease of use and the ability of customers to do more remotely using chatbots and mobile devices. National lockdowns birthed new and innovative payment and banking services, particularly in those regions of the world hardest hit by the pandemic—Latin America, Central and Eastern Europe. Everything from custody services for digital assets, to greater financing and working capital options for small and midsize enterprises (SMEs), payments at a glance, paperless trade and virtual digital influencers for promoting greater financial literacy among students, are recognized among this year’s Outstanding Innovations.

|

CASH MANAGEMENT INNOVATIONS 2021 |

|---|

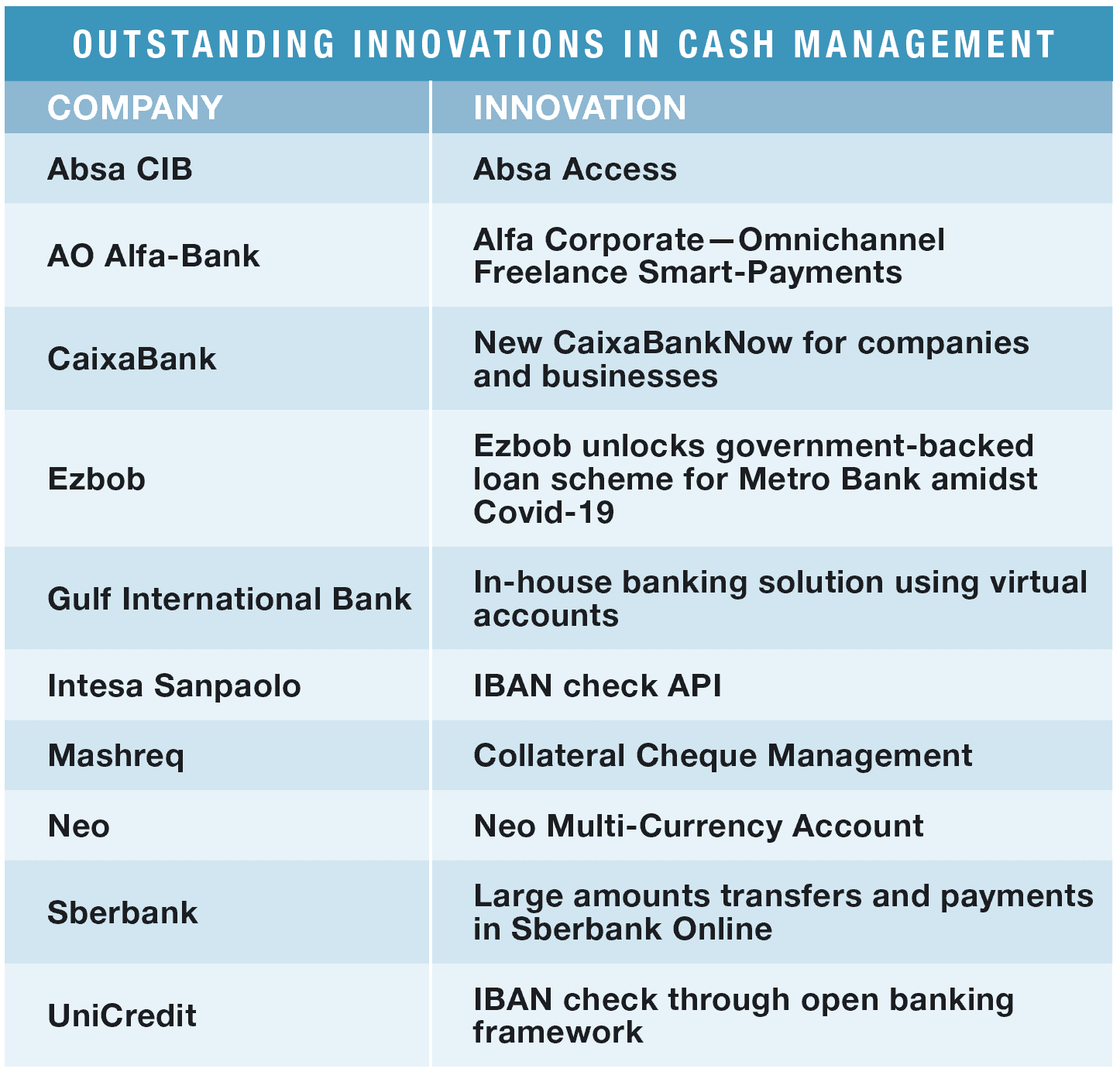

Renewed emphasis on working capital led to a raft of cash management innovations this year, as banks and fintechs sought to provide corporate customers with the most usable and efficient solutions. At the start of the pandemic, keeping the lights on and the doors open was the key preoccupation for most companies; and that intense focus on cash has led to a change in cash culture, with clarity and big-picture awareness seen as crucial components. Digital solutions are bringing convenience to businesses and helping service providers deepen relationships with their clients.

For South African Absa Corporate and Investment Banking (Absa CIB), the separation and rebranding from Barclays allowed following a pan-African service model and taking the opportunity to create a new digital platform that provides clients and colleagues with a single access point to all corporate and investment banking products and services.

In building Absa Access, bank employees and customers no longer need to navigate a disparate mix of Barclays and vendor solutions. “Our focus is to create a platform that offers a complete transactional banking proposition for our customers and solves key components of the cash conversion cycle,” explains Thabo Makoko, managing director of transactional banking, African regional operations for Absa Group. “We focus on simplifying payment solutions for clients and include domestic, cross border as well as micro payments to mobile wallets. We provide clients with the ability to facilitate trade transactions on the platform including fulfilling their FX [foreign exchange] requirements.”

Absa also offers liquidity solutions allowing customers to better manage cash flow, and an electronic bill presentment and payment solution simplifies the collections and reconciliation processes for clients. Makoko says investment into the Access platform is anchored on building skills and modern ways of working as well as leveraging technology to ensure Absa can scale securely and respond to client demands at speed. “Our platform enables us to offer a comprehensive proposition and to exploit synergies between products that were traditionally sold independently,” Makoko states. “The key principles that continue to govern our platform build are intuitive design, simple integration, superior customer experience and best-in-class security.”

For CaixaBank, an upgrade of CaixaBankNow for businesses includes a customized homepage with a personalized dashboard, and the integration of third-party services, providing users with a global, aggregated vision of their most relevant information to facilitate decision-making. Since the advent of the revised Payment Services Directive (PSD2) regulations, CaixaBank has developed a range of application programming interface (API) products for corporate clients.

“We understand open banking as an opportunity, a real way to deepen our relationships with clients,” says Jordi Nicolau, director of retail banking and customer experience, CaixaBank. “With the PSD2 regulation, we will be able to improve our clients’ experience, with new client-engagement models and the development of new platform and ecosystem business models based on the API channels. These are some initiatives that are allowing us to accelerate our digital transformation, not only in the retail sector but also in the corporate one.”

While APIs are making it simpler to roll out new products, making life simpler for clients is a key cash management consideration. Affluent customers of Sberbank no longer need to come to the office to make large transfers, as they can carry out transactions of up to 15 million rubles with the Sberbank Online mobile application, using biometrics.

To help corporate customers manage complex global account structures and control working capital effectively, Gulf International Bank introduced an in-house banking solution using virtual accounts. Mashreq, another Gulf region bank, has developed a collateral check management solution to enhance controls on security checks handling assigned to the bank—catering to both conventional and Islamic banking corporations.

Italian banks Intesa Sanpaolo and UniCredit, meanwhile, have both adopted International Bank Account Numbers (IBAN) checking solutions to provide real-time verification to protect against fraud and reduce payment rejections. Crucially these allowed the Italian public administration to verify the IBANs of cash benefit recipients during the pandemic. Through API integration both banks are developing multi-bank functionality to offer both retail and corporate clients further simplification.

Neo, a fintech focused on treasury management, payments and FX, provides SMEs fully registered IBANs from which they can complete payments in over 30 currencies via plug and play multicurrency accounts.

Fellow fintech Ezbob, meanwhile, integrated its digital SME lending-as-a-service solution with Metro Bank in record time, enabling Metro to take part in the UK government-backed Bounce Back Loan Scheme to help small businesses through the Covid-19 pandemic. It will also benefit the bank in the future.

“A digital SME lending platform improves profitability in several ways,” says Tomer Guriel, Ezbob’s CEO. “By automating a labor-intensive process, it can reduce operating costs by 80%, the AI-enhanced data analytics can improve the loan book by making smarter lending decisions, and customer acquisition costs are reduced through a superior user experience.”

Also looking out for small businesses, AO Alfa-Bank Russia introduced this year a new freelance smart-payments management system, based on blockchain technology, to provide independent consultants with financial services such as payments, income registration and tax management.

|

CORPORATE FINANCE INNOVATIONS 2021 |

|---|

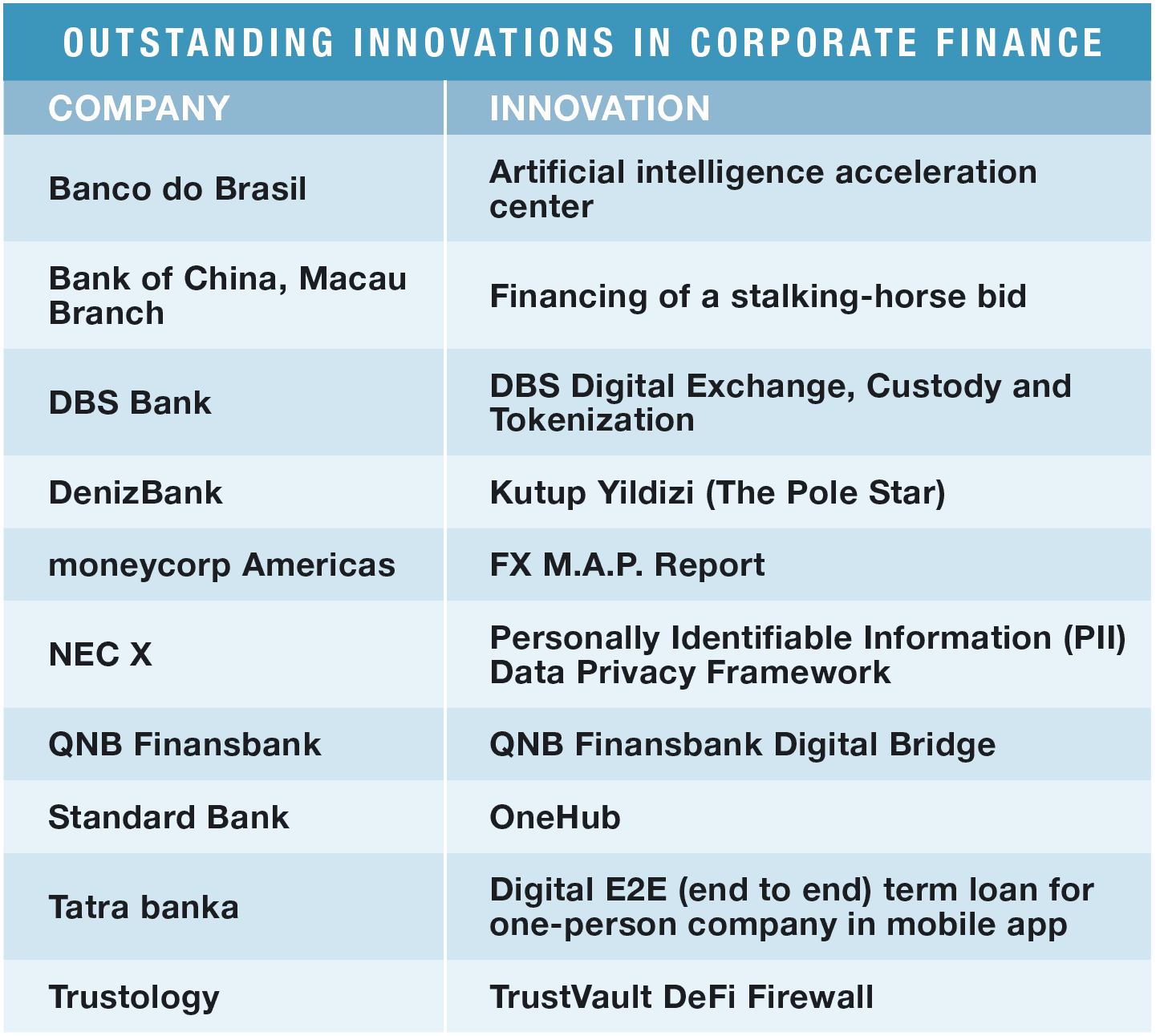

Although many financial professionals remain skeptical about cryptocurrency, institutional money is gradually finding its way to this new world. Some of this year’s top innovators in corporate finance address the growing trend of institutional investment in digital assets by providing a framework for safekeeping services, for example, as they do for more-tangible assets. Other innovations address rising privacy concerns, leverage technology to expand uses of information and access to finance, and more.

Legacy technologies just don’t cut it in the supercharged world of digital assets. DBS Bank’s Digital Exchange, custody and tokenization support the issuance, trading and custody of digital assets. The solution uses distributed-ledger technology, which provides traceability and transparency of ownership of digital assets; a cloud-native stack; and a “supercharged matching engine,” as DBS terms it, that allows hundreds of thousands of trades to be processed per second.

Trustology’s TrustVault DeFi Firewall is designed to enable users of DeFi (decentralized finance) protocols for lending, trading and borrowing cryptocurrency assets to safely and easily administer assets in real time. This helps create trust and growing institutional participation in the burgeoning DeFi market, which is worth approximately $128 billion.

One DeFi trend gaining momentum is lending cryptocurrency assets out to generate higher returns or to earn additional crypto. However, Trustology’s CTO, Mark Hornsby realized a better solution was needed to make this type of lending work for institutional users who may be unaware of DeFi’s inherent risks (DeFi protocols are unaudited, managed by anonymous project owners and susceptible to hacking attacks). DeFi Firewall solution is built on top of Trustology’s TrustVault custodial wallet, which provides an advanced security layer and controls for moving assets between the different DeFi protocols. “Trustology is proud of the impact our DeFi Firewall is having in protecting our institutional clients from harm while allowing them to leverage the power of decentralized finance,” says Hornsby.

Away from the world of cryptocurrency assets, traditional corporate financing providers like FX specialist moneycorp Americas is providing North American CFOs with digital tools to help them better assess the strengths and weaknesses in their hedging ratios. Its FX M.A.P. Report, which is currently available only in North America, looks at a corporation’s overall portfolio of hedges and provides high-level reporting to determine what’s working and what’s not so the company can better manage its FX exposures.

“After learning that many businesses were unhappy with the unreliable and time-consuming hedge reports in the market, we decided to develop an all-encompassing tool that would take the admin work off the desks of CFOs, allowing them to spend more time focusing on their core business and making strategic decisions quickly and efficiently,” says Bob Dowd, CEO at moneycorp Americas. “Our breakthrough FX M.A.P Report takes all of the client’s current positions into one repository and provides real-time data on their overall portfolio versus their exposure.”

Other innovations in corporate financing focus directly on terms of financing. Financing by Bank of China, Macau Branch (BOCM) of a stalking-horse bid enabled Chinese pharmaceuticals company Hayao to acquire the “good assets” of Pittsburgh-based vitamin and health supplements maker GNC, which filed for bankruptcy during the Covid-19 pandemic. Normally, companies that file for bankruptcy find it difficult to access financing from commercial banks; but BOCM was able to restructure GNC’s debt and optimize its capital structure, enabling Hayao to safely bid on GNC’s good assets.

Innovations at QNB Finansbank in Turkey and Standard Bank in South Africa help companies bridge the digital divide. QNB Finansbank’s Digital Bridge supports SMEs in their digital transformation journey by providing them with access, free of charge, to a wide range of e-enablement solutions such as e-invoicing, HR management, e-commerce marketplace management and other finance and accounting software tools. The bank’s fully rolled-out Digital Bridge portal allows SMEs to manage all of these solutions via a single sign-on or password.

Standard Bank’s OneHub draws on the bank’s own experience, customer insights and developer teams, to provide corporate clients in Africa, the bank’s staff and fintech partners with a single digital entry point for consuming web-based and API solutions. The aim is to give the bank’s customers access to a wider range of innovative business-to-business solutions tailored to their individual needs.

Tatra banka’s digital E2E (end-to-end) term loan for a one-person company in a mobile app for internet banking ushers in an era of fully branchless banking by making it easier for self-employed people and single-person companies to apply for loans from anywhere in the world, without needing to visit a branch. In this way, the bank was able to easily grow its customer base during the pandemic and service customers remotely.

DenizBank’s Kutup Yildizi (The Pole Star) also uses a new mobile app but aimed at the bank’s sales teams out in the field wanting to access critical information (key performance indicator reports, sectoral information or historical data) about their customer portfolios without having to revert to computers back at the branch. Thanks to the mobile app, time spent outside the branch during working hours is now more productive.

Banco do Brasil’s artificial intelligence (AI) acceleration center has enabled the bank to develop a range of innovative solutions that help it better predict customer satisfaction levels. During the pandemic, due to many customers’ decreased ability to repay debts, Banco do Brasil used AI to help them safely renegotiate debt agreements remotely using chatbots without any human intervention.

Alongside the increasing use of AI and machine learning by banks to provide customized solutions for their corporate customers, is the need to keep personally identifiable information (PII) safe. Silicon-Valley based NEC X and OppLane combined their advanced technologies—NEC X’s AI/machine-learning accelerator processor and OppLane’s Cognitive Computing Engine—to deliver an AI-based solution, ID-Redact.

“The solution gives higher confidence to enterprises in corporate financing when it comes to PII data privacy and compliance measures,” says Robbert Emery, director of technology marketing and business development at NEC X. ID-Redact parses, identifies, confirms and redacts PII within the data ecosystem, including structured, unstructured and semi-structured data formats. “This collaborative product partnership addresses the rapidly evolving global data privacy laws and regulations, while at the same time lowering financial institutions’ operational overhead,” says Emery.

|

ISLAMIC FINANCE INNOVATIONS 2021 |

|---|

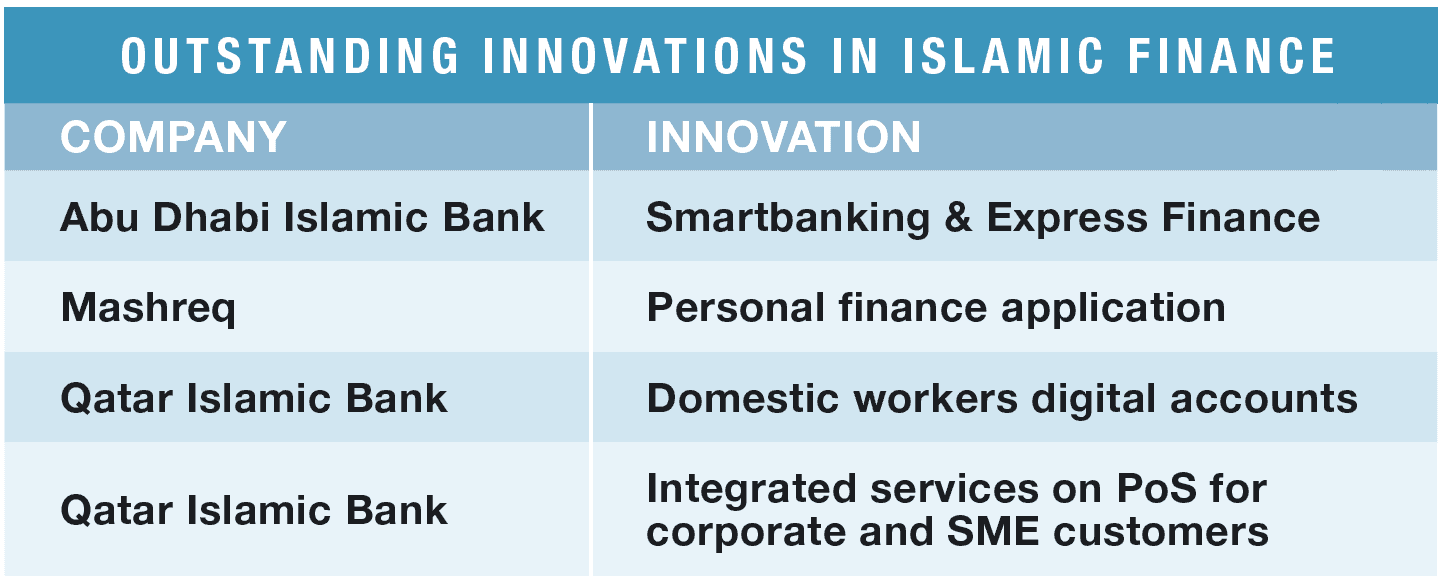

Islamic financial institutions have been severely disrupted by Covid-19, encouraging banks to develop innovative solutions that cater to customer needs. In particular, tools for financial inclusion and for facilitating access to needed cash became of overriding importance during the pandemic.

In 2020 Qatar Islamic Bank (QIB) became the first Islamic bank in Qatar to launch a corporate-only mobile app. Additionally, it developed two solutions that stood out for solving very different problems created during lockdown. Dinos Constantinides, QIB’s chief strategy and digital officer explains how QIB’s easy and contactless integrated postal delivery point of sale (PoS) works, in collaboration with the Qatar post office: “Now the person who delivers your post at home or in the office will scan a parcel through the terminal, and all the information will automatically come in; and the customer, with one of our contactless cards—or that of somebody else in the market—can pay.”

A similar collaboration with Vodafone makes the telecom operator’s electronic recharge and bill payment services available via QIB select PoS machines available for all merchants in Qatar. “It is a simple solution that answers a business need,” Constantinides says. “I think this is important to be successful in any business—you need to satisfy a real need.”

Last year, QIB launched a unique end-to-end digital account to enable domestic workers to open bank accounts remotely through its mobile app. This allows their sponsors to pay their salaries, gives domestic workers a digital alternative for their remittances and limits their reliance on cash. Constantinides added, “At QIB, we are committed to provide banking services to all segments of society and to support their inclusion in the banking system. Providing those services in a convenient, simple and secure way is a key objective.”

Digitization helped Mashreq eliminate the need for its customers to fill and sign lengthy contracts—converting a five-day Islamic personal finance process into a five-minute digital journey.

Increased speed lies behind the Smartbanking and Express Finance innovations by Abu Dhabi Islamic Bank (ADIB). “Through effective digitization, we have been able to streamline our processes, reduce costs and ensure that our customers have convenient, seamless and uninterrupted banking services,” states Philip King, global head of retail banking at ADIB.

Covid-19 forced banks to adopt a more agile way of working, and Constantinides wouldn’t have it any other way: “QIB started its own digital transformation a few years back. Post Covid-19, customers’ adoption of digital solutions has increased significantly. All banks are upgrading their digital channels; there is good, healthy competition right now in the market, which is great because it is good for customers and the banking sector, and it also makes us not lose our sense of urgency.”

|

PAYMENTS INNOVATIONS 2021 |

|---|

Disruption in payments continues at pace—turbocharged by the increase in e-commerce and heightened demand for contactless solutions brought on by the global pandemic. From real-time to automated and from mobile to biometric, cash is no longer the king of commerce, as payments become more digital and faster and smarter than ever before.

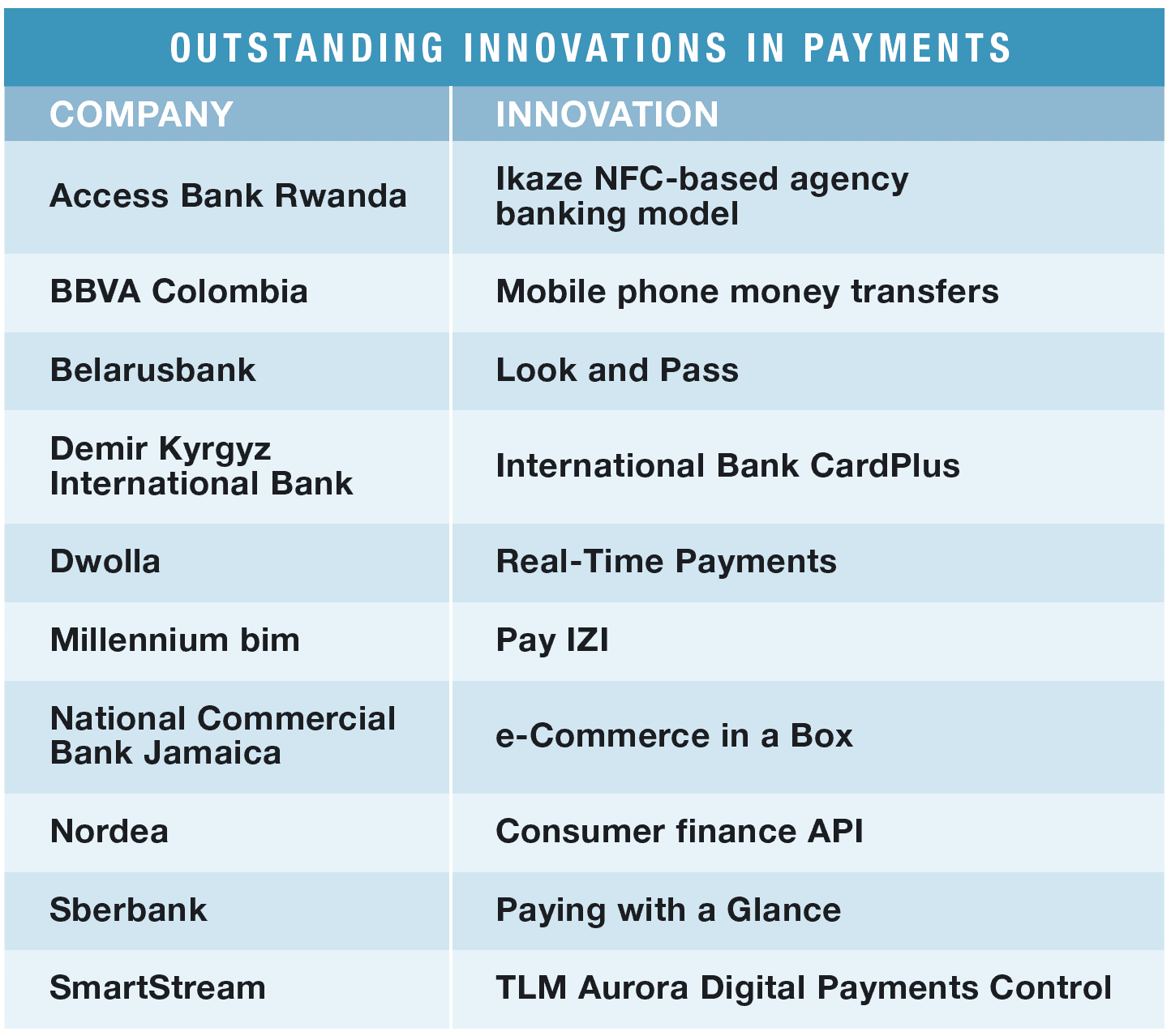

In April 2021, the payment network Dwolla released Real-Time Payments (RTP), adding to the company’s payment technology suite that includes ACH and Push-to-Debit. By changing a small line of code, existing clients can initiate an RTP transaction using Dwolla’s API.

To help both traditional and alternative payment providers act a lot smarter with their payments data, SmartStream has developed an AI reconciliation called TLM Aurora Digital Payments Control to help find and manage exceptions rapidly.

“At the heart of any business it is critical to have the necessary data integrity and validation checks in place,” explains Andreas Burner, chief innovation officer at SmartStream Technologies. “Through our research in the lab, we’ve found that integrating AI and automation in daily operations allows banks to respond to the demands of both the industry and its customers in a fraction of the time.”

The rise in mobile payments is synonymous with the rise in real-time payment processing, and banks have needed to adapt to compete with challengers.

Many of this year’s payments innovators have found ingenious ways to make it easier for clients to make mobile payments. To help facilitate mobile phone money transfers, BBVA Colombia clients just need to enter the mobile phone number of the recipient, who does not need to be a BBVA client, and the transfer is made through the BBVA app.

Millennium bim became the first bank in Mozambique to integrate a mobile banking platform, IZI, with another mobile money platform, M-Pesa. With Pay IZI, Millennium bim allows connections to other apps so its customers can receive payments from nonbank customers.

Two banks recently deployed facial recognition systems.

Belarusbank initiated the Look and Pass metro fare payment technology. Users must first download the Belarusbank app and take a picture of their face, which is then stored in a database. Fare amounts are debited from a payments card keyed to the face each time the user scans it at biometric terminals on the fare gates. Belarusbank claims authentication takes two seconds and works while turning one’s head, in poor lighting or even if the user is wearing glasses or a medical mask.

Dmitry Malykh, acquiring director at Sberbank, says over 400,000 clients currently use Sberbank’s biometrics for payments. Buyers are not required to sign any documents and in less than a minute can have their face and card tied to Sberbank’s Paying with a Glance option. “Biometrics data is aggregated, processed and stored by Sber alone,” Malykh states. “The key benefits for clients are usability and a contactless way of making a purchase.”

As of today, there are almost 6,600 biometric self-service scanning devices at Russia’s largest food retailer, X5 Retail Group stores, including its Pyaterochka and Perekrestok stores in all parts of Russia with X5 presence. On top of that, the service is available in Cafe PRIME (85 stores) and food retailer VkusVill (44 stores).

In 2021, Malykh says, biometric payment can be made available in 7,000-10,000 more devices and in 1,500-2,000 stores. “This could be the largest biometrics adoption the retail industry has ever seen,” Malykh insists. “In terms of the number of stores, no similar examples of biometric payment availability can be found in or outside Russia.”

Technology has been key in helping businesses remain operational during the pandemic. Access Bank Rwanda Ikaze Agency Banking is the first and only agency banking model in Rwanda powered by near-field communication (NFC) technology, whereby agents are enabled to issue NFC prepaid cards and process transactions online and offline.

National Commercial Bank Jamaica developed e-Commerce in a Box—a bundled suite of solutions that provides micro, small and medium-sized enterprises (MSMEs) with a low-cost means to make and accept payments online with or without a website. The solution includes inventory, management, accounting and customer relationship management functions so MSMEs can manage their operations using a single application. It’s also integrated with DHL’s logistics hub so MSMEs can send goods from anywhere.

Noncash payments have also led to card innovations. Demir Kyrgyz International Bank’s CardPlus allows people to purchase goods by credit card and repay it in installments This is a first in the Kyrgyz financial market, and it’s helped increase turnover for merchants involved in the CardPlus project.

In collaboration with a well-known Nordic airline, Nordea developed an innovative open banking solution, consumer finance API that is improving the digital experience of airline customers applying for an airline-branded loyalty credit card as they now receive a response to their credit application in a couple of seconds.

Payments may have become remote and contactless, but for banks and fintechs they offer opportunities to remain at the heart of customers lives.

|

TRADE FINANCE INNOVATIONS 2021 |

|---|

For many years, trade finance seemed to be stuck in the dark ages. Early attempts to try digitizing parts of the physical supply chain largely failed as there were so many moving parts (shipping, warehousing, customs, insurance, freight forwarding, logistics), which made it difficult to get everyone on the same page, let alone connected on a single digital platform. But thanks to the emergence of “disruptive” technologies like blockchain, combined with different forms of AI such as optical character recognition, and APIs for ease of integrating new and innovative applications, trade finance is now one of the most dynamic and fastest evolving businesses in banking.

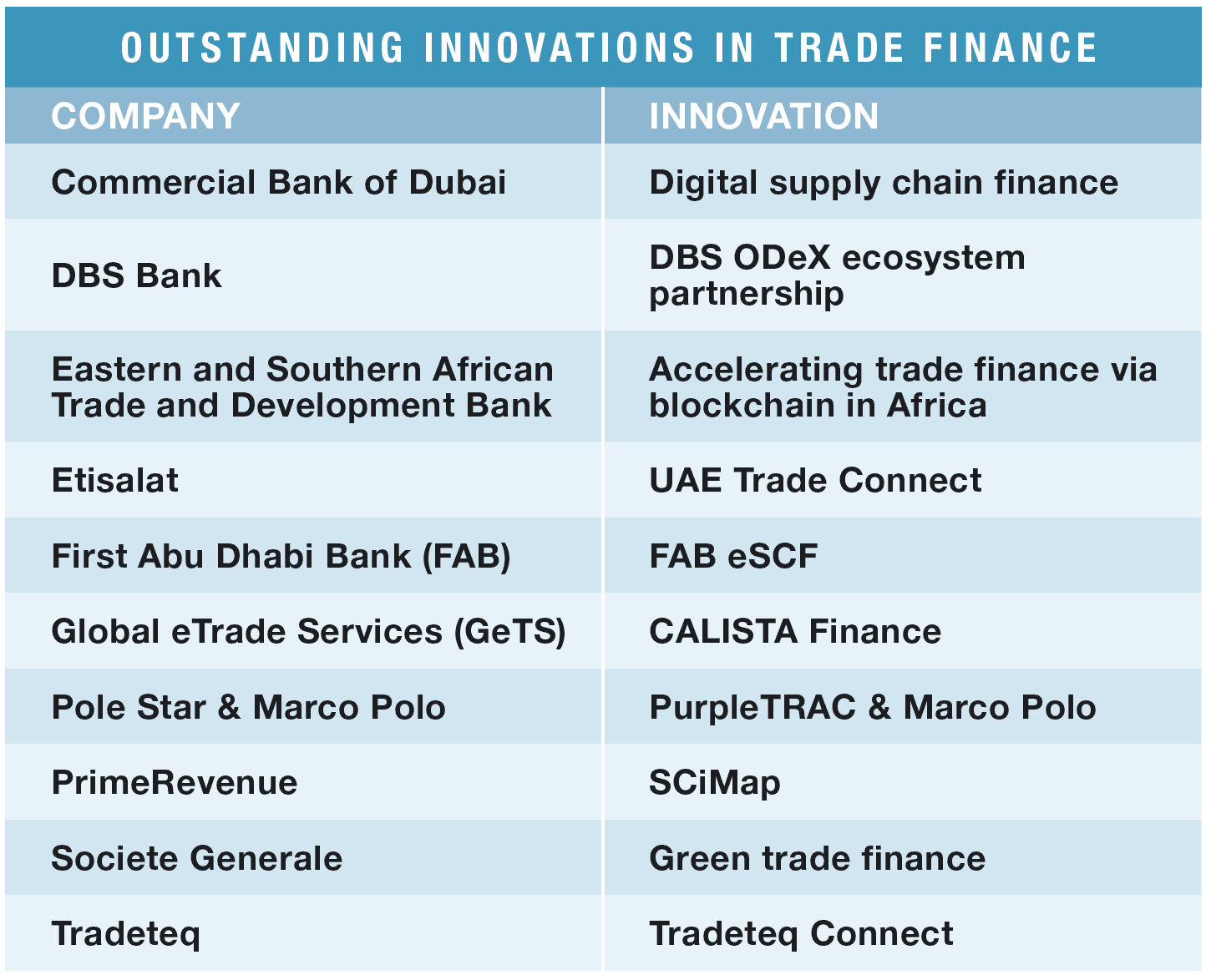

With multiple counterparties to a single trade, innovation in trade finance requires collaboration between different parties. That is how the UAE devised one of the Emirates’ first commercialized blockchain applications, UAE Trade Connect (UTC). The idea stemmed from an approach First Abu Dhabi Bank (FAB) made to Etisalat Digital, the digital solutions arm of the UAE’s largest telco provider, to help brainstorm ideas to address the perennial problem of duplicate financing and fraudulent documents in trade finance.

The end result is UTC, which CEO Zulqarnain Javaid says is a pioneer in the niche of applied blockchain technology. “The solution was innovated through ‘cocreation,’” he says. “It is among the country’s first commercialized blockchain applications, which has been successfully adopted because of the collaborative approach taken to build it.”

A consortium of eight UAE banks—FAB, Mashreq, Abu Dhabi Islamic Bank, Emirates NBD, Commercial Bank of Dubai, Commercial Bank International, Rakbank and National Bank of Fujairah—came together in 2019 to test the initial proof of concept for UTC. During the pandemic, the solution rapidly moved from testing and development to “limited load” mode. Last year, Etisalat and participating banks put the finishing touches to UTC, which uses the immutable nature of transactions on the blockchain, AI and machine learning to help identify duplications and dubious transactions and ensure data has not been tampered with. Ultimately, Etisalat hopes the UTC will give banks greater comfort and confidence to extend financing to SMEs.

In addition to being part of UTC, FAB was also recognized individually this year for upgrades to its fully automated eSCF (electronic supply chain finance platform). In Q1 last year, FAB updated the service to include a multi-bank SCF capability that provides companies greater funding flexibility. The bank also automated the syndication of SCF programs and introduced trade receivables discounting.

Commercial Bank of Dubai partnered with UK-based SCF solutions provider Demica to provide its Middle East customer base with a fully integrated digital platform for managing their payables and receivables and accessing working capital. CBD says the digital supply chain finance platform is the first of its kind in the region and that it will help corporates improve their supply chain management.

Another of this year’s innovators, Singapore’s Global eTrade Services put SMEs at the heart of its CALISTA Finance solution, which uses blockchain; optical character recognition for reading documents; and a machine-learning-based credit engine, which is fed trade data so it can better assess the credit needs of SMEs that lack strong financial documentation. Using CALISTA Finance, loans are typically approved within 72 hours versus the weeks it used to take using traditional know-your-customer and credit assessments.

UK-based Tradeteq took a slightly different approach to plugging the trade finance gap for SMEs. It is increasing the pool of available trade liquidity by automating the distribution of core trade assets (letters of credit, guarantees and trade loans) between banks. Its Tradeteq Connect solution replaces spreadsheets with an electronic platform featuring an information-rich dashboard that can be easily connected to existing trade workflows using APIs. By automating the flow of assets, Tradeteq hopes to make trade finance accessible to a wider pool of investors, beyond banks.

Letters of credit have been used for hundreds of years in trade finance. But during the pandemic, the time it took to physically exchange and verify them often stretched into weeks. This forced the Eastern and Southern African Trade and Development Bank (TDB) to devise an innovative solution to keep intra-African trade and supply chains moving.

Using blockchain, the TDB was able to significantly reduce the time it took to confirm letters of credit—less than two hours in most cases. Instead of physically moving documents between suppliers, they are uploaded, edited and validated on the blockchain.

With its green trade finance solution, French bank Societe Generale is also reimagining the humble letter of credit and trade guarantees—not just for the digital age, but as an instrument linked to sustainability goals, such as clean energy, that can help companies transition from carbon-intensive activities to more-sustainable business models.

To ensure supply chains keep moving, DBS Bank’s ODeX ecosystem partnership saw the bank extend lending and payment services to one of the biggest online communities of carriers, yards, port terminals, forwarders and shippers. Using APIs and analytics, DBS devised a lending program for ODeX’s users that allows them to easily make payments to shipping lines connected to the ODeX platform. The real-time flow of information between DBS and ODeX’s platform means customers can automatically trigger financing requests.

Innovation isn’t always about building something from scratch. It can also come from a meeting of minds or solutions, which is certainly the case for Pole Star and global trading network Marco Polo. In 2020, Pole Star, which monitors global maritime trade, partnered with TradeIX to bring its PurpleTRAC regulatory solution to Marco Polo’s global trade network. The combination of PurpleTRAC’s vessel-tracking capabilities with Marco Polo’s Payment Commitment digital trade settlement instrument made it easier for shipping operators to secure and manage payments for transiting the Panama and Suez canals and for high cargo operations.

“This year has the potential to mark the end for paper-based processes in the maritime and trade financing industries,” says Simon Ring, Pole Star’s global head of maritime trade technologies and ESG. “By moving to digitized processes, with access to faster, cheaper and more-efficient payment solutions, the industry will be future-proofed to better withstand shocks.” With maritime trade facing increased regulatory scrutiny, and few financing options currently working well for both buyers and suppliers, Ring says Pole Star’s and Marco Polo’s joint solution allows both to access new working capital programs tailored to their unique transaction requirements.

Aside from digitalization, another theme running through this year’s innovations in trade finance is use of data to strengthen supply chains. Take multibank supply chain finance platform PrimeRevenue’s customized data analytics and insights for its SCiMap. The upgraded solution, which was launched in the fourth quarter of last year with eight pilot customers, will be rolled out to a wider customer base in the second half of this year. It enriches supply chain data, providing buyers with insights into payment terms by supplier industry, credit scores and cash needs by supplier, to help them make better-informed procurement- and credit-optimization decisions.

|

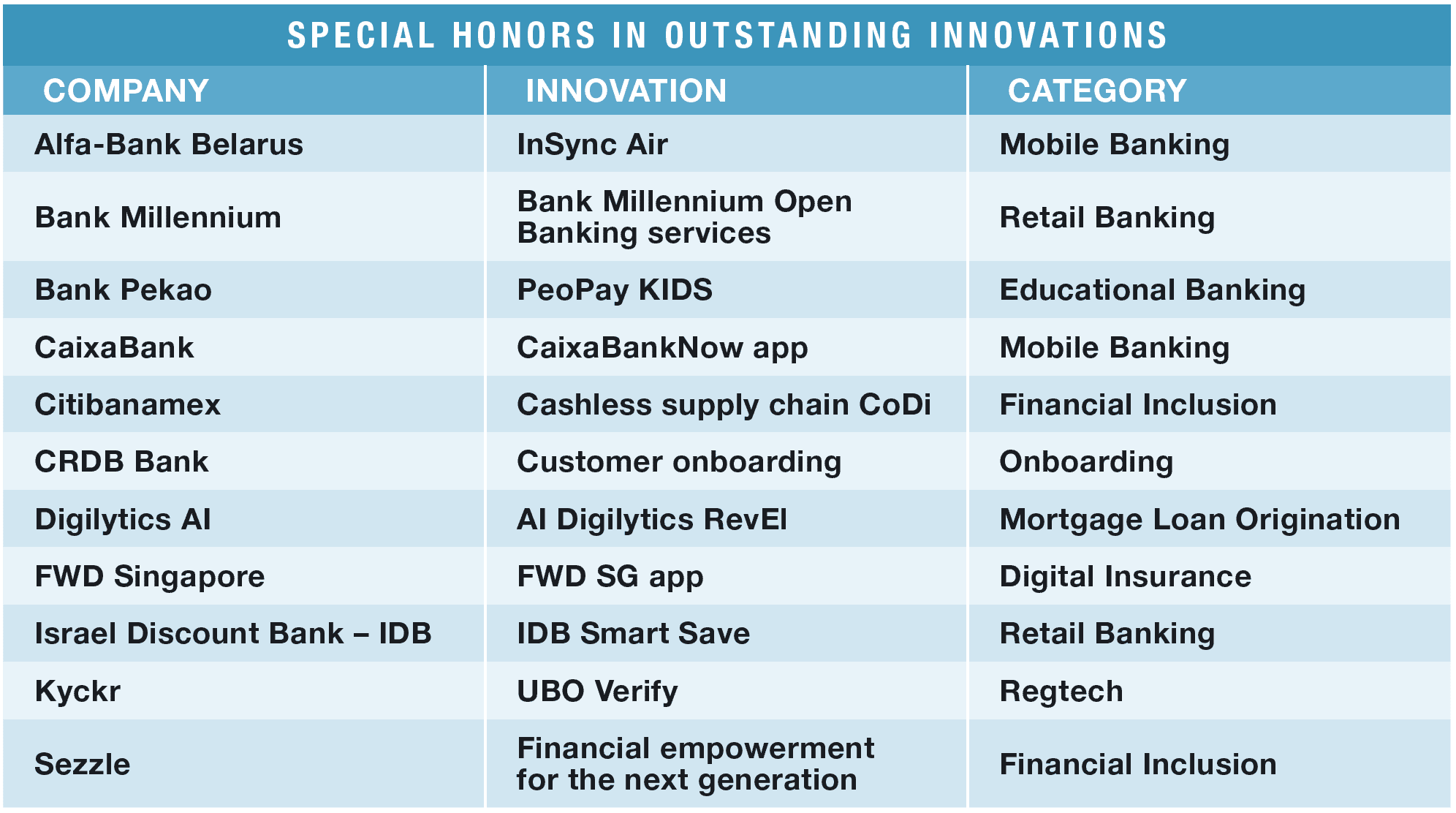

SPECIAL HONORS INNOVATIONS 2021 |

|---|

Blurring banking with being ever present in people’s lives is fueling a raft of lifestyle banking options as banks take advantage of technology and data to provide value added services that go above and beyond a focus on transactions. With greater access to data and the technologies that help you understand it, such as analytics, AI and machine learning, financial institutions can better comprehend customers and deliver better services and products.

Alfa-Bank Belarus introduced a whole ecosystem that combines a line of “Smart Family” banking packages. The InSync Air solution allows customers to log into the InSync mobile app and share an account with family members and close friends. Once a person invited to the account agrees to the InSync app terms and conditions they can immediately begin using the accoun

Similarly, family focused Bank Pekao launched an educational mobile app, PeoPay KIDS, linked with bank accounts for children aged 6-13. While there is a parents’ panel, enabling parents to exercise discreet supervision over a child’s finances, Bank Pekao hopes to educate children about saving money and explain the intricacies of the world of finance through a series of virtual training guides.

CaixaBank has made a series of improvements to its CaixaBankNow app that rely on open banking to deliver improvements to customers. “The integration of third-party services within our digital banking service, CaixaBankNow, allows us to offer the advantages of nonfinancial services and products,” explains Jordi Nicolau, director of retail banking and customer experience at CaixaBank. “For example, we can highlight our ‘travel service’ for retail clients, created with the integration of third-party market leaders, as well as partnerships on city mobility and the strengthening of our entertainment- and leisure-services portfolio.”

Bank Millennium has also made use of open banking to deliver customer benefits. In January 2020, the Polish Bank launched the Finance 360° service, enabling customers to aggregate their accounts at other institutions into the Bank Millennium mobile app and online banking. This was extended in March to allow customers to initiate a payment from an aggregated account via online banking. In May, the bank launched an income verification product for loan applications that is used to streamline customer applications for cash loans. Finally, in October 2020, the launch of identity verification for business banking applications capped a year of plentiful open banking options for clients.

A partnership with Personetics helped Israel Discount Bank (IDB) deliver Israel’s first-ever automated digital savings tool and provide additional value to its customers. IDB Smart Save is an AI-based feature, embedded within a customer’s banking app. Twice a week, the tool analyzes monthly expenditures—including future forecasted expenses—and then spots available money in the checking account, automatically transferring the funds into a designated saving account.

The highest-rated buy-now-pay-later offer in the market is provided by Sezzle, whose stated mission is financially empowering the next generation. Sezzle Up was launched in December 2020 and helps customers get access to credit, build their credit score and increase their financial education. By making payments on time, users can increase their credit score.

Citibanamex is also playing its part in increasing financial inclusion. A tripartite alliance between the bank, a large distributor and a microfinance company provides microcredits to shopkeepers. The shopkeeper, via Citibanamex’s Transfer App, has another payment option through a QR code (CoDi) enabling safe digital payments and is able to make payments under the same CoDi platform to the seller of the large distributor.

In Mexico, 95% of payments are made with cash. “For many years, big retail distributors have carried out operations with cash, which represents an expense in their different collection channels; therefore, today they are looking for digital solutions that allow them to optimize their resources and innovate their channels,” states Rodrigo Kuri, CEO, Global Consumer Bank, Citibanamex. “One of the biggest retail distributors needed a solution for exactly that: reducing their cash flow in collection, decreasing commissions, optimizing resources and giving more security to their sellers.”

“What we did was to create this model that promotes financial inclusion through digital tools that allow shopkeepers to have an easy, fast and secure access to banking services,” says Kuri. “The solution that we created allows the big distributor to be able to collect through digital accounts that help them reduce the use of cash, robbery losses or loss of cash and most importantly, improve the security and control of their resources.”

This year’s remaining special award innovators have all made tasks easier with technology. Digilytics AI’s RevEl improves mortgage loan origination through AI by achieving 95%+ accuracy in extracting and validating data from mortgage documents, with one-shot learning in real time and at scale for first time-right applications.

FWD Singapore’s app enables customers to easily submit insurance claims, access their policy documents and manage their policies, anytime and anywhere.

Tanzania’s CRDB Bank improved customer onboarding with customer verification enabled by scanned fingerprints using a low-end smart camera, a first in the country.

Ultimate beneficial owner (UBO) investigations are both lengthy and labor intensive, and Kyckr’s unique, proprietary registry network UBO Verify enables shareholder information to be extracted in real time from the respective corporate registry—returning accurate, current and legally authoritative information at every search.

Whether it’s lifestyle banking that suits customer needs rather than a bank’s products or finding time-saving solutions to previously laborious processes, technology continues to provide ways to make life better.