In the past century, gains in productivity and living standards were made as a result of advances in technology. But where can we expect gains to come from in this century—and are they likely to be gradual or dramatic? The answer depends on whether you believe the optimists or the pessimists.

Many factors contribute to higher national incomes and standards of living, but if you had to use a single measure, it would be increases in productivity. An average yearly increase in productivity of 2.5% doubles national income over a 30-year period. In the last century, productivity grew at an unprecedented rate of almost 3%. More recently, that growth has lagged. Yet given the advances being made in robotics, artificial intelligence and Big Data analytics, there is room for hope.

Sixty years ago, washing machines freed us from the daunting task of washing clothes by hand, giving us time for more productive activities. The extra hours made available gave our ancestors an edge. Most of our grandmothers started working away from home; others spent more time studying or educating their children. Along with washing machines, their generation enjoyed a deluge of other inventions, which transformed their lives and made it possible to double and triple standards

of living. The question now is, will robots help our sons and daughters as much as washing machines helped our grandparents?

Most Western economies face long-term economic headwinds: an aging population, growing debt levels and, often, unbalanced income distribution. To compensate for these effects, it would be necessary, every year, to bake a larger pie to improve standards of living while at the same time support the elderly and repay debt. But baking a larger pie is not possible without the yeast of higher productivity.

Jaana Remes, an economist and partner at the McKinsey Global Institute (MGI) believes productivity needs to become the central focus of the debate on economic policy. “Productivity is the key to make our children and their children better off,” she explains. “You cannot overemphasize the importance that productivity has. [It] will become even more important with an aging population.”

Yet, since 2005, the growth of total-factor productivity (TFP)—the measure of efficiency of all inputs (labor and capital combined) to the production process—in the United States has halved from 1.75% in the period 1996–2004. The Conference Board, a nonprofit research group, published its Total Economy Database in May 2015, with data showing that the growth rate of TFP stayed around zero for the third year in a row, compared with an average rate of more than 1% from 1999–2006 and 0.5% from 2007–2012. Developed economies like the US, the eurozone and Japan showed near zero or even negative TFP growth. China, a productivity superstar until 2006, also entered a contraction phase, with TFP declining 0.1% in 2014. Both Brazil and Mexico recorded negative TFP growth over the past three years of available data.

THE PESSIMISTS WEIGH IN

Growth in TFP can be attributed to many factors, but it is heavily influenced by advances in technology. The debate raging among an army of economists is whether productivity is facing a temporary decline or the world has entered a new phase where productivity stagnates, or in the best-case scenario, expands very little. When it comes to future productivity growth, economist Robert Gordon, a professor at Northwestern University, is the pessimists’ standard-bearer. He says that until 1870, productivity rose by a modest 0.2% per year. From 1870 to 1970 productivity picked up. Since the 1970s though, he says innovations were not as effective or as numerous as they had been in the past and that this explains why the speedy improvements in productivity of the past century are over.

In the postwar era, 1948 to 1970, US productivity grew, on average, 2.7% per year, whereas at the time of the dot.com revolution, between 1994 and 2004, it rose by 2.26% per year. “Productivity slowed despite the innovations we had, and I expect [that trend] to continue,” says Gordon. “There will be only evolutionary change, not revolutionary change.” Robots are still clumsy and driverless cars still need humans for safety reasons. They are not innovations as far-reaching as the steam engine or running water in the home. Gordon expects US productivity to actually improve from the recent past, but at a rate of around 1.2% per year from now until 2040.

PUTTING INNOVATION TO WORK

Most economists are critical of the way productivity is measured and recognize that past productivity swings have taken them by surprise. In the 1990s, for example, US productivity overall expanded at rapid rates because of improvements in specific and large employment industries—not just the dot.com industry, but also wholesale and retail, which have a large weight in the economy as a whole, says Remes at MGI. Large sectors in the US could be on the verge of a jump in productivity, she says, pointing to the health and public sectors as examples. “We do not see any structural reason why we could not face a quick turnaround of productivity growth in several sectors,” she says.

Since the financial crisis of 2008–2009, a high level of uncertainty—due to concerns about global security, future consumer demand and international trade—has blocked or delayed investments that may have been essential for boosting productivity. “Economics is, after all, a business of animal spirits and global appetite for investments,” says Remes. “[Now is] a time when the overall pessimism regarding the future has been a big barrier for companies to decide about new investment.”

More than a lack of inventions, the economy is suffering from a lack of ways to put these inventions to work. A boost of confidence in the economy can trigger a new productivity burst, not only by raising efficiency but also by creating new products.

“We have never seen a technology innovation pipeline as robust as the one we have now,” says Remes. “It is not just computers and IT, but also bioengineering, new materials, the ‘Internet of Things’ and Big Data.” Remes says the speed of innovation and the opportunities for additional productivity growth have never been broader and deeper than they are today.

The financial crisis of 2008–2009 froze new investments everywhere, but in some regions, like Southern Europe, for example, access to the capital markets has remained blocked. Marcel Fratzscher, president of the German Institute for Economic Research (DIW Berlin) says the US responded in a much better way to the global financial crisis by closing down banks, forcing them to recapitalize and merge at a time when they had a strong monetary and fiscal stimulus. “Productivity,” he says, “is not something God-given. It is largely under the control of the governments, which, in my view, did not implement the right policies over the last few years.”

FRONTIER FIRMS

Kyoji Fukao, a professor at The Institute of Economic Research, Hitotsubashi University, Tokyo, notes that while in the 2000s Japan fixed some financial issues—nonperforming loans and damaged balance sheets—that put a drag on businesses, productivity has lost two decades of growth. “In the manufacturing sector, the TFP growth of small and medium-size firms (SMEs) lagged behind, while the TFP of larger firms has actually accelerated,” says Fukao, offering a possible explanation. “Large assemblers like Toyota used to have technological spillovers towards smaller suppliers. The link got lost when these large assemblers started to change suppliers more often or moved their factories abroad.”

A dual productivity speed trend, with a few advanced firms leading the way and the remainders lagging behind, is common to several countries: from Mexico to Turkey and India. The Organization for Economic Cooperation and Development published a book in 2015 focused on “frontier firms” and how they behave across 19 countries. “What we show is that this gap between global frontier firms and the others has actually increased over time,” says Dan Andrews, senior economist, structural policy analysis division, policy studies branch at the OECD in Paris. “We know that productivity at the aggregate level has slowed down, but what is interesting here is that the most productive firms are still doing well. It is the rest of the firms in the economy which present a problem.”

The most productive companies grow more in some countries than in others. Their size depends on how markets are organized, says Andrews, citing Italy, where there are a few, very efficient firms in the textile industry. These firms are small, though, so their impact on the country’s global productivity is minimal.

“Instead, if you look at the US, the most productive firms are much larger and have a much bigger impact on global productivity,” he says.

According to studies conducted by John Van Reenen, director at the Centre for Economic Performance at the London School of Economics and Political Science, differences in productivity between other countries and the US can be explained, on average, by a better quality of management.

“I grew up in Britain in the 1970s, and there was British Leyland, a state-run company with terrible management practices,” says Van Reenen. “In the 1980s, Japanese companies came in setting up new car factories in Britain, famously Nissan in Sunderland, and people did not believe at the time they could have done something different. But they did, bringing a different management style.”

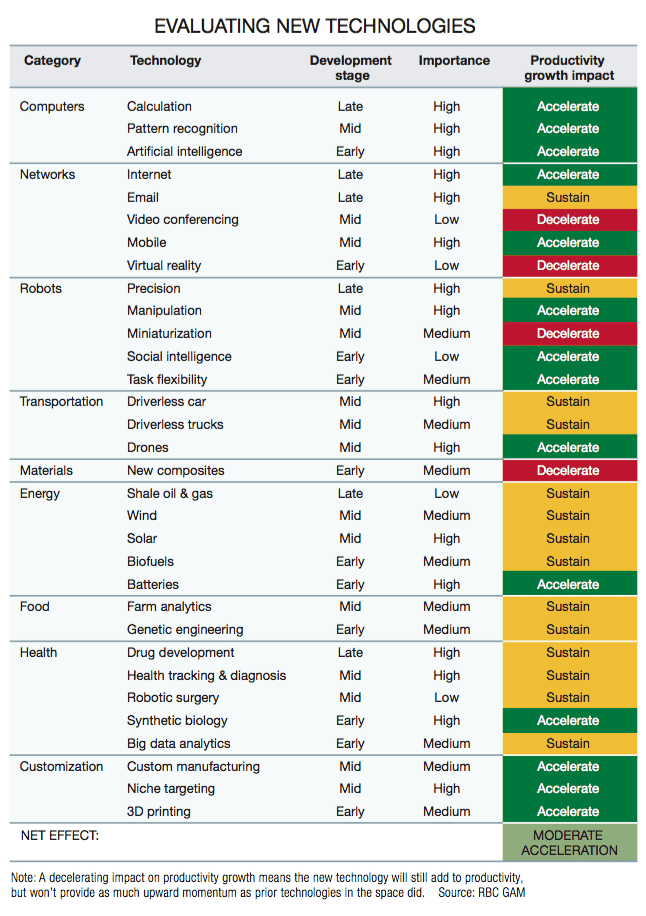

There are economists who predict that productivity growth will resume both for developed and emerging countries. Eric Lascelles, chief economist at RBC Global Asset Management, says the computer revolution is still paying dividends, and that we’re still in the middle of the networking revolution. Robotics is also at an early stage. “Then we have to cross our fingers and hope that the new inventions will come along, but I do not see why they should not.” Lascelles sees future productivity increasing by an average of 1.8% per year in developed countries and 4.7% in emerging markets.

Whether the pessimists or the optimists are right will have a big impact on the standards of living of the next generation. One thing that is clear, however, is that governments should pay much more attention to the issue, doing whatever they can to remove any obstacles to productivity growth.