With a possible slowdown looming and the promises of data insight, treasurers are keeping an especially close eye on their cash.

The aim of cash management for corporate treasuries is making the most efficient use of cash and getting the best return on cash assets. This has always been true, but it is even more critical during periods of political and economic turmoil. With inflation and higher interest rates impacting both the cost of supply and the prices companies can charge, treasurers need to understand trends and keep a close eye on their liquidity if they are to manage financial risks and take advantage of opportunities in the year ahead.

“Liquidity is the lifeblood of every business, and they need to have a good understanding of where the liquidity is in the company,” says Edi Poloniato, head of working capital at Kyriba.

Deloitte’s Global Treasury Survey 2022 finds liquidity risk management as the top mandate for treasurers. A survey of CFOs and treasurers published by PNC Bank and GTreasury in December, meanwhile, sees financial executives name improved risk management, increased cash visibility and automation of treasury functions as key areas required to fuel growth, while recommending treasury technology to unlock financial opportunities and help navigate through uncertainties.

The rise in instant payments—fueled by e-business models, marketplaces and platforms—drives a trend to manage liquidity in real time. There are currently some 55 instant payments schemes globally; and efforts that accelerate the speed of cross-border payments—such as Swift’s global payments initiative—are pushing corporates to spread their cash across multiple banks and shift toward multibank cash-pooling solutions, providing the necessary visibility to optimize liquidity.

API And Corporate Treasury

An important next step toward the goal of real-time or near-real-time liquidity is the use of application programming interfaces (APIs), which bring new functionalities and convenience to treasurers. By enabling disparate technology platforms to talk to each other, APIs allow banks to open back-end data functions to their clients and share data with other banks—equipping them to offer their own clients multibank target balancing and reporting.

Citi offers a real-time liquidity-sharing capability that automates and optimizes the use of net available balances dispersed across multiple entities and accounts. It also offers virtual lending and borrowing between pool accounts via a single global platform with automated liquidity controls and other limit-setting capacities.

The CitiDirect BE Cash Concentration portal allows users to perform a wide range of adjustments to their pooling structures themselves—making it easier to respond quickly to changes in business models or cash flow forecasts. Clients can modify target-balancing parameters, suspending or reactivating sweep pairs and amending interest reallocation rates—marking a strategic shift toward on-demand liquidity management.

BBVA is enabling more-agile cash flow by allowing API integration between the bank and the client’s enterprise resource planning (ERP) systems. “BBVA’s cash flow APIs provide a new and more efficient communication channel with the bank,” explains Carmen Cuesta, senior manager, enterprise solutions strategy at BBVA. “This can be integrated into the company’s internal processes.”

APIs also enable banks to offer third-party treasury services, accelerate their “go to market” efforts, create additional revenue streams and improve client experience. “It’s not the banks’ objective to replace what they have, but to go beyond what they tend to offer,” Poloniato explains. “We don’t come and replace their core or control—for example, a corporate bond tool. We integrate through APIs to what they have already—providing additional tools in terms of cash forecasting and cash management within their portal—helping them to be closer to their clients.”

Toward the end of 2021, Societe Generale, in partnership with Kyriba, launched Global Treasury—an open banking initiative that will provide French SMEs with a cash and payment cloud-based treasury management system. Global Treasury enables real-time monitoring of treasury positions and provisional management of liquidity flows, payment automation for remittances, banking delegation and mandate management, enhanced fraud management, multibank connectivity with ERPs, payment validation, workflow management and more.

Delivering With Data

Just as open banking and APIs have brought greater efficiencies and innovations to treasury and cash management services, ISO 20022 promises to reduce payments friction. ISO 20022 migration is scheduled to begin on March 20, 2023, and supports the inclusion of richer, better-structured transaction data in payments messages. This has benefits for both banks and corporates. For banks, it presents more-accurate compliance processes, higher resilience and improved fraud-prevention measures, while providing opportunities to finally leverage and monetize the vast data their payments business offers. By helping corporates and their banks reconcile more efficiently, it will deliver a better customer experience that requires less manual intervention, in the process helping to unlock real-time payments for corporates.

Carl Slabicki, co-head of global payments at BNY Mellon’s Treasury Services, foresees a future in which banks can leverage cross-network data, such as Swift data, real-time payments data, Automated Clearing House data, etc., to improve fraud analytics and provide more value to client services. “There’s a lot of analytics we can give them to, for example, look at investment options based on monthly cash flow patterns, or if we spot suspicious things happening with certain types of payments to certain individuals,” he says. “So, there are things we can give clients to make proper decisions to protect themselves and be more efficient with their working capital.”

Thanks to the ability it gives banks to leverage data in a much more structured way, ISO 20022 brings greater standardization and paves the way for intelligent payment and smarter treasury operations.

Automation and cloud-based systems are also assisting smarter treasury practices and reducing workloads—freeing up a treasurers’ time for more strategic thinking. While computers take over the heavy lifting of repetitive manual tasks, meaningful data will greatly enable treasurers to concentrate on strategic issues. The 2022 AFP Strategic Role of Treasury Survey found that in addition to core functions—cash management, liquidity and improving payment processes—treasurers are increasingly supporting nontraditional areas, including business continuity planning, M&A and enterprise risk management.

On top of this, treasury can also be a driver for an organization’s environmental, social and governance (ESG) initiatives. As financial shepherds, treasurers can invest excess cash in assets that are consistent with overall ESG objectives, ensure the integrity of ESG reporting and how it may influence credit availability and pricing, leverage capital markets to raise funds for ESG-linked activities, leverage supply chain finance programs to incentivize improved ESG performance from suppliers and choose banks who align with the company’s ESG priorities.

With such a wide remit, treasury teams will increasingly need to adopt digitization and technologies such as AI and blockchain to meet modern treasury challenges, and they will be looking for financial partners who can best support them.

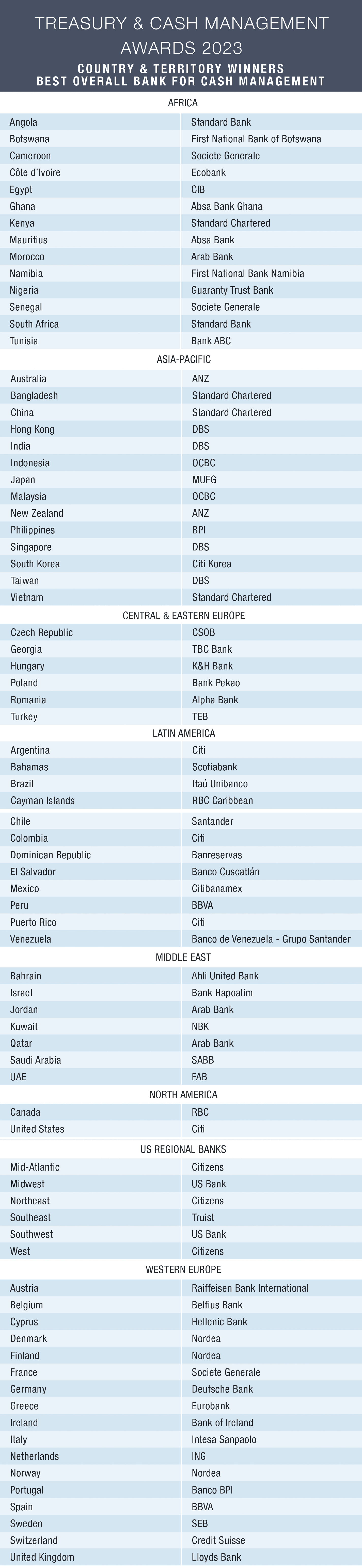

Methodology: Behind the Rankings

Global Finance editors select the winners for the Best Treasury & Cash Management Awards with input from industry analysts, corporate executives and technology experts. The editors also use entries submitted by financial services providers, as well as independent research, to evaluate a series of objective and subjective factors. It is not necessary to enter in order to win, but experience shows that the additional information supplied in an entry can increase the chances of success. In many cases, entrants are able to present details and insights that may not be readily available to the editors of Global Finance.

This year’s ratings are based on the period from January 1, 2022, to December 31, 2022. (Companies with different fiscal year reporting have the option to submit data from the fourth quarter of 2021 through the third quarter of 2022.)

Global Finance uses a proprietary algorithm with criteria—such as knowledge of local conditions and corporate customer needs, quality of product and service offerings, financial strength and safety, market standing, compliance and excellent customer service—weighted for relative importance. The algorithm incorporates various ratings into a single numerical score, with 100 equivalent to perfection. In cases where more than one institution earns the same score, we favor local providers over global institutions, and privately owned banks over government-owned ones.

The winners are those financial services providers that best meet the specialized needs of corporations engaged in global business. These top-notch finance institutions are not always the biggest, but rather the best—those with qualities that companies should look for when choosing a provider.