President Jokowi is a radical departure from Indonesia’s political and military elite, which perhaps explains why he is such a populist leader at home. But foreign investors find him difficult to read.

With Chinese demand for commodities at its lowest ebb in five years and a looming fiscal challenge caused by eroding revenues and increases in much-needed infrastructure spend and social programs, investors are watching the administration of president Joko Widodo (widely known as Jokowi) closely. They hope the negative cycle of slowing growth and currency devaluation will be firmly addressed.

In March there were some signs that their concerns were being heeded. “China is slowing; we are working hard to see what we can do to maintain growth or mitigate the downside,” a Finance Ministry spokesman stated.

Planned changes include lifting personal nontaxable income by 50%, to 54 million rupiah ($4,000) per year. This comes on the back of a more than doubling of the income tax threshold in 2015, a key agenda item for this populist president. It is anticipated that the resulting tax shortfall will be offset by a growth in median incomes: Household consumption has held up well to date, increasing by plus 5%, year-on-year, versus 5.2% year-on-year in 2014.

Early in his tenure Widodo cut fuel subsidies by 9%, allowing for a reduction in aggregate distribution costs of 3%. Fuel subsidies, which cost up to 30% of budgeted expenditure and encouraged a parallel market in illegal fuel exports, were a political hot potato, and Widodo’s decisive move augured well.

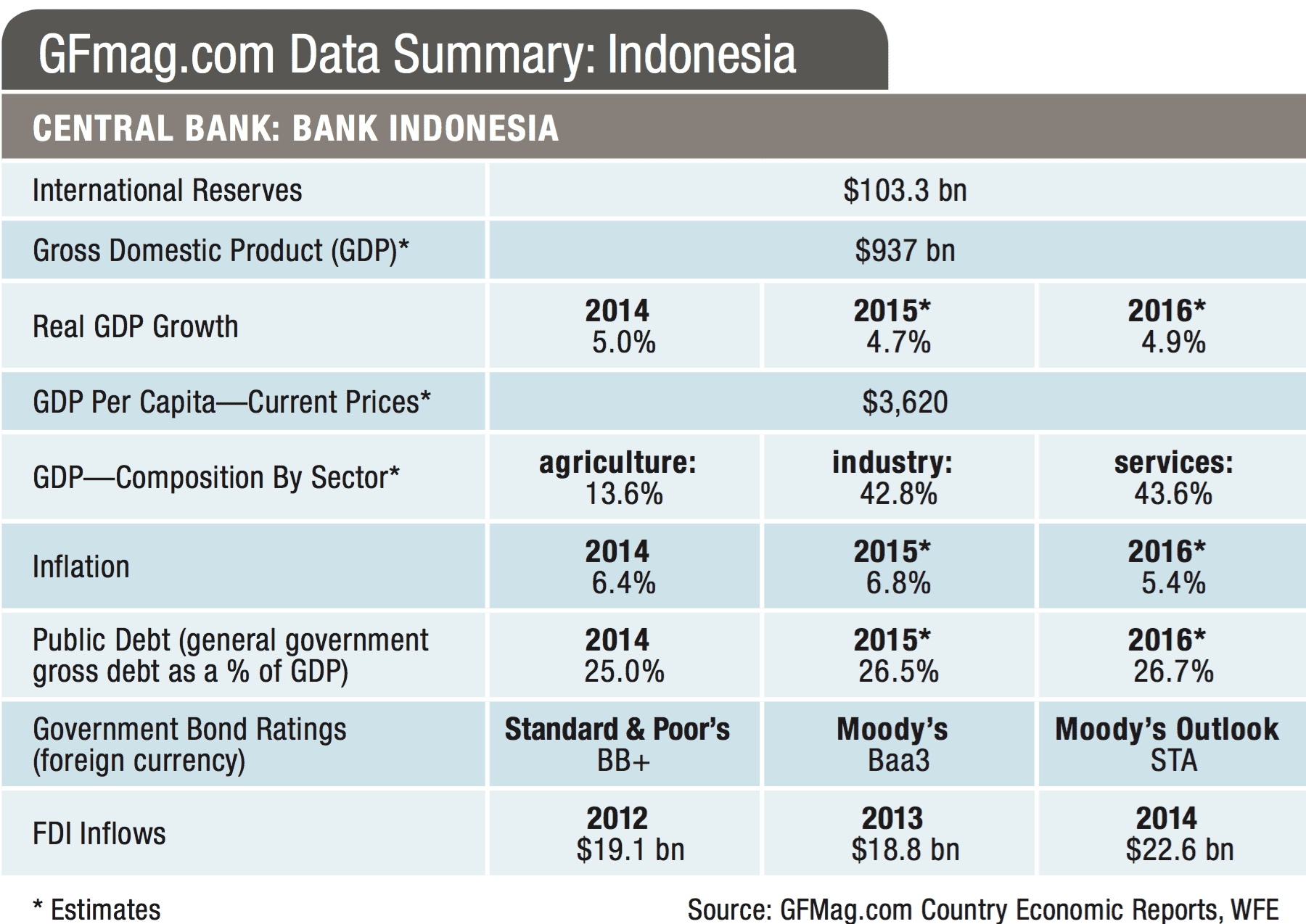

Confidence Grows, But Growth Slows

On the face of it, this country of 255 million people has everything going for it. The larger cities, especially the Jabodetabek (the urban areas surrounding the capital Jakarta), boast a growing middle class that likes to spend. The Consumer Confidence Index, which is a good indicator of retail sales and household consumption, has been on a firm upward trend since October 2015, thanks in part to benign inflation. Lower taxes should catalyze consumption in the near term, with a firmer consumption recovery by the second half of this year.

Consumer staples and retail and telco sales are expected to benefit from a recovery in consumption. But growth has been sluggish and continues to be hampered by an urgent need for external investment in infrastructure.

Almost alone among Asia’s leading cities, Jakarta lacks a subway. This sprawling capital is prone to massive flooding as a result of overdevelopment and a drainage system that harks back to the Dutch colonial era.

“You can’t have an Asian strategy without including Indonesia” says Seng Wun Song, CEO and regional economist at CIMB-GK Research in Singapore. “But investors need to understand the special conditions that prevail here. On the plus side, the banks are not overleveraged and interest rates are coming down. Indonesia has evolved politically and is more effectively balancing China against effective engagement with the West.”

Song also points to orderly political change. Since the government of longtime strongman president Suharto fell, there have been five democratically elected presidents. “There is also a clear effort to define an Indonesian identity which is democratic, embraces religious freedom and encourages tolerance, albeit with a strong Islamic component,” explains Song, adding that Widodo made a point of consulting interfaith groups after recent terrorist attacks.

Widodo Still Hard To Figure

Elected in 2014, Joko Widodo was a radical departure from previous Indonesian leaders, as he belonged neither to a dynasty nor to the army. As a consequence, he lacked a strong party base in parliament. As a former mayor of Surukarta, a city in Central Java, he enjoys strong local affiliations, but he came to office lacking foreign policy depth. Like all Indonesian politicians, Widodo is strongly nationalistic, and the independence rhetoric of the Sukarno era persists in today’s politics. The government’s seemingly contradictory messages must be processed through the filter of this nationalism.

For example, Widodo alarmed Western countries by resuming executions of foreign criminals—including a number of women, one over 70—despite the fact that executions were stayed under his predecessor, Susilo Yudhoyono. The executions were thought to be a sign of a populist leader showing that foreigners could no longer expect favoritism.

In a worrying echo of Malaysia’s Bumiputera system of economic favoritism toward indigenous Malays, recent regulations also require noncontributing local partners to be given equity in any new company. There are also revised limits on foreign investment in many sectors, including telecoms, minerals and manufacturing.

The Waiting Continues

“Foreign investment is essential for economic growth,” says Song. “Yet the messages to investors are far from clear.” Capital will not deliver high-quality infrastructure if rules and regulations allowing for a reasonable level of return on projects are absent. “Here Indonesia has, if anything, gotten worse under Widodo,” explains Song. “You often hear that Indonesia follows India.”

As a massive producer of crude oil, Indonesia lacks refining capacity. The failure of multiple putative partners over decades ever to break ground on much-needed refineries is a persistent indictment of Indonesia’s inconsistent message to investors.

Song says Widodo’s effectiveness suffers as factions fight one another for the riches of Indonesia. “A Javanese ambivalence about foreign involvement in the Indonesian economy is visible at the heart of what observers see as the key investor conundrum—‘Do they want us or not?’”

The hope is that the Asian Infrastructure Investment Bank, launched by China, will kick-start the development of critical infrastructure, including a high-speed rail link between Jakarta and Bandung, a Jakarta subway and key regional airports. Yet observers note that Indonesia’s Transport minister did not show up for inaugural AIIB announcements.

“Without political will there will be more corruption, local resistance over eminent domain, and a host of licensing difficulties,” says Song. “There is already evidence of Chinese interest switching to Vietnam.”