With customers hungry for new digital experiences and a large unbanked population, Africa is shaping up as a bellwether of how banks can truly embrace the digital age and serve customers better.

Africa’s banking market is one of the fastest growing and most profitable in the world. According to a recent report on Growth and Innovation in African Retail Banking published by management consultants McKinsey, in the five years leading up to 2107, the number of ‘banked’ Africans almost doubled to 300 million, and is expected to rise to 450 million banking customers in the next five years.

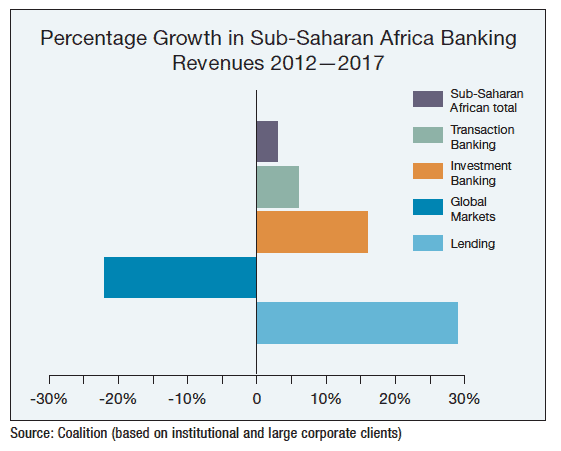

In the past five years globally, banks’ profit margins remained flat at 3.8%. But African banks increased their margins to 6.8%. And last year, they generated an average 14.9% return on equity—a level of profitability surpassed only in Latin America, and more than double the 6% achieved by banks in developed markets.

That outperformance is expected to continue, with banking revenues across the continent predicted to grow at 8.5% a year through to 2022, outstripping the developed world and most Asian markets. “Growth is sustainable,” says Mutsa Chironga, a partner in McKinsey’s Johannesburg office. “Most African economies are growing rapidly and there is extremely low market penetration and choice, especially in retail banking, where on average customers are offered just two distinct products.”

But there are huge differences between different regions and countries within Africa. At present, just five countries—South Africa, Nigeria, Egypt, Angola and Morocco—account for more than two-thirds of all banking revenue across the continent. That is expected to change over the next five years, with a shift away from Southern Africa toward North Africa, East Africa and West Africa.

Banking on Digital

Reaching a mass market of potential customers who earn less than $6,000 a year is the ‘next frontier’ for African banking. The mass market will account for just 13% of Africa’s retail banking revenue growth through to 2025, says McKinsey, but it is still the fastest growing market segment. “Banks looking to expand in the mass market need a different approach,” says Chironga, “with lower costs to match lower revenues per client.“

”They must be open to lending into Africa’s huge informal economy, which means that many potential customers generate regular cash flows, rather than a fixed monthly income, by starting with smaller loans and using data such as mobile-payment patterns to gauge creditworthiness,” Chironga added.

The current limitations of credit scoring in Africa will be helped by advances in digital technologies, says Richard Ladbrook, portfolio manager at Cape Town–based Investec Asset Management. “By generating more information about customers’ behavior and cash flows, banks will be more confident in lending to lower-income customers,” he says.

Chironga notes that fintechs like Jumo, which combines data with technology to provide more ‘progressive’ savings and lending products, are already aggregating social media and other data to help build credit-scoring models for major banks, including Barclays Africa and Old Mutual.

Mobile phones and digitization are key to opening new markets. Some 40% of African banking customers surveyed by McKinsey said that they preferred to use digital channels for transactions, with roughly the same share still favoring bricks-and-mortar branches. But in some of the continent’s major banking markets, customers’ appetite for digital banking is much greater. In Kenya, for instance, the share of sales and transactions via digital channels at Equity Bank has increased more than 60%, creating opportunities for both new product sales and substantial cost savings.

In some parts of Africa, partnerships between telecom companies and banks are bearing fruit. Chironga points to M-Shwari, a new banking product for customers of Kenyan mobile phone–based money-transfer service M-PESA, which enables them to save and borrow money through their phone.

In Nigeria, he says the partnership between Diamond Bank and dominant telco MTN, which resulted in the Diamond Yello account, has effectively tripled the bank’s customer base. In most cases, those banks that have partnered with telcos or fintechs are able to deliver an admittedly limited range of banking services, but at a much lower cost than what was possible via a traditional branch network.

Winners and Losers

Until now, the profitability of many African banks has largely rested on their ability to charge much higher interest rates than anywhere else in the world. But that may soon change, as increased competition pressures margins in the years ahead. “We expect net-interest margins to shrink,” says Ladbrook, “so banks need to grow volumes and develop new revenue streams, mainly from transaction fees, to support revenue growth.”

They also need to become more efficient. Africa’s banks have the second-highest cost-to-asset ratio in the world, and recent years have seen worsening cost-to-income ratios, which many see as unsustainable.

“There is massive room to improve productivity,” says Chironga. “In many branches, you’ll find long queues, even though staff numbers are high because of all the paperwork needed to complete transactions, while at headquarters there are too many levels of management. More of their employees need to be directed to generating revenue.”

Ladbrook: Advances in digital technologies will help overcome credit-scoring challenges. |

With fast-growing demand for banking services and only limited access through traditional branch networks, Africa can leapfrog the legacy banking models of more developed markets and embrace the digital age. But it is not yet clear who will gain the most from this digital transformation—digital-only start-ups, existing players that follow Nigeria’s Wema Bank by launching a fully digital bank, or incumbents that can use their scale to create favorable partnerships with telcos and fintechs.

While Ladbrook believes the upside from increasing digitization “is probably greater in Africa than elsewhere,” he expects incumbent banks to adapt to this successfully rather than being disrupted by newcomers.

And across the continent, he sees dominant local banks winning out over the super-regionals, largely because they are trusted brands and have the scale and operational leverage to offer competitive products. Regional banks usually lack scale in each of their markets, where they run into different regulatory, operational and credit-quality issues. But with so many disruptors appearing in their home markets, not even the biggest players can relax.