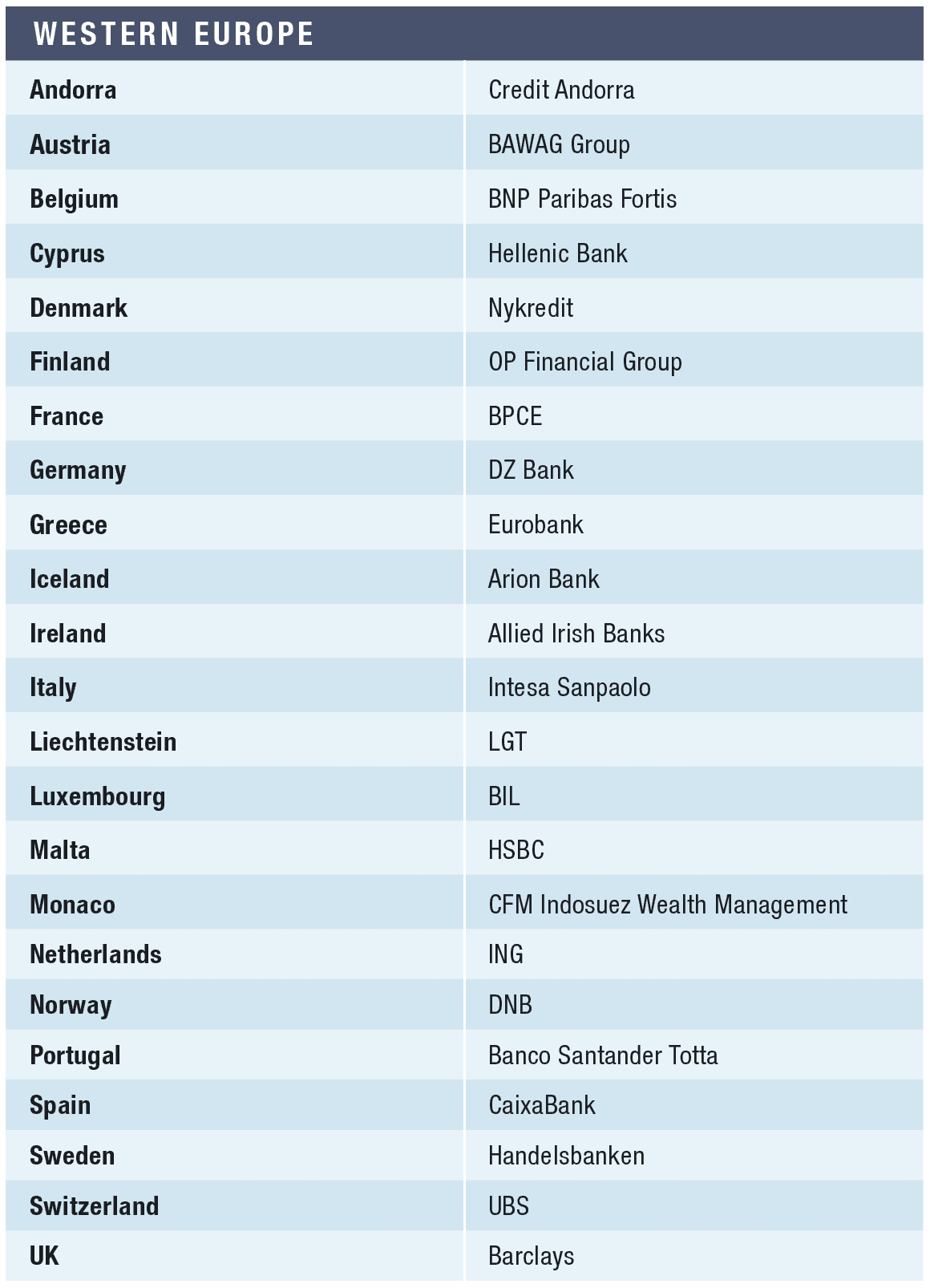

2021’s Best Banks in Western Europe lead in service and innovation.

The main challenges facing European banks as they entered 2020 were relatively slow economic growth coupled with ultralow interest rates, while strong competition in growing market segments such as mortgages led to margin compression. The arrival of the pandemic raised completely new challenges–adapting branches to meet health guidelines and business models to home-working and greater reliance on digital channels. Banks also had to respond rapidly to the economic impacts of lockdowns on their customers, through payment holidays, loan restructurings and by providing liquidity to businesses that were most seriously affected.

The speed and efficiency with which most banks–including our winners–adapted to the “new normal” is remarkable. The more successful had already invested heavily in digitization and, since the pandemic acted as an accelerator to the migration of customers to digital channels, these banks were also able to accelerate the rationalization of their branch networks, thereby reducing their cost base over the long term.

Most European banks anticipated impairments to loans–especially in the travel, hospitality and physical retail sectors–early on, and provisions against future loan losses severely dented banks’ headline profits in 2020. Their underlying operating performance has generally been much better and they have strengthened their capital buffers, partly due to regulatory restrictions on paying dividends, which resulted in more retained capital.

CaixaBank is again Global Finance’s Best Bank in Western Europe on the strength of its rapid response to the Covid-19 crisis, its innovatory and customer-focused strategy on digitization, and for further consolidating its position as the leading retail bank in the Iberian region both through organic growth and by acquiring former rival lender Bankia.

Gonazalo Gortázar, CEO of CaixaBank, notes that “during the year CaixaBank provided an extensive Covid-19 response to support clients and society. We approved close to 400,000 loan moratoria; advanced payments on pensions, unemployment and furlough benefits; and provided liquidity and credit to those sectors most in need of them.”

“At the same time, we were able to report a profit of €1.4 billion on flat core revenues and a 4% cost decline, while also paying a dividend and ending the year with a Common Equity Tier (CET) 1 ratio of 13.6%–up 1.6% over the year.” This was achieved despite CaixaBank’s raising provisions against impaired loans–many of them pandemic-related–to €1.25 billion and investing a further €936 million in technology and development.

Gortázar says the key drivers of the bank’s performance were “sustained market share and volume growth throughout the year, generating operating leverage and improving efficiency, while further reinforcing our strong balance sheet. All these achievements were made possible by our consolidated leadership in retail banking, both physical and online, the dedication of thousands of committed top-quality professionals, a strong financial position, and a tradition of responsible banking that spans more than 115 years.”

CaixaBank is also our Best Bank in Spain, where the merger with Bankia makes the combined entity the clear market leader, with €660 billion of assets and some 13.4 million customers. “The merger,” says Gortázar, “created the undisputed leader in the Spanish financial services sector and was a landmark transaction in the European banking consolidation process.

“This transformational deal is not only crucial for us to adapt to an environment that is characterized by difficult macroeconomic conditions and technological upheaval, but will also reinforce our ability to continue providing support to businesses, the self-employed, families and society as a whole.”

Our winner in Portugal, Banco Santander Totta, continued to benefit from its digital transformation strategy during 2020. The number of digital customers grew by 20% compared with a 4.3% overall increase in clients. Deposits grew by 2.3% and the bank increased its loans to customers by 6.8% over the year.

Pedro Castro e Almeida, chief executive and chairman, observed that “our priority remains intact: supporting households, companies and society in Portugal. Our clients’ trust is also reflected in the positive evolution of deposits, of credit granted, and the growing use of our digital platforms–representing 42% of sales–which accompanies a change in client behavior as they are increasingly demanding and looking for better, more effective and more efficient services that facilitate their day-to-day activities.” At year end, the bank’s CET1 ratio stood at 20.6%, an increase of 3.6% compared to December 2019.

Crèdit Andorrà, our winner in the independent principality lodged between Spain and France, maintained its market leadership in the key wealth management, sector with nearly a third of all assets under management while generating more than 40% of all profits in the banking sector. The bank’s solvency ratio of 16.8% is more than double the legal minimum in Andorra. Crèdit Andorrà’s business hyperacceleration program, Scale Lab Andorra, evaluated over 350 companies in its first year of existence, leading to investments in four companies.

BPCE is our Best Bank in France having had a strong year despite difficulties arising from the pandemic. Chairman Laurent Mignon says, “The Group’s results are solid, fully demonstrating the effectiveness of our decentralized and diversified business model. The Group has also a robust financial position, prudent regarding forthcoming risks and fully capable of facing the challenges that lie ahead.”

Retail banking and insurance revenues were up 2.6% for the year and gross operating income increased by 6.7%, with a strong improvement in the fourth quarter due to a higher level of business activity. Strict cost controls resulted in a 2.9% reduction in operating expenses over the year. Corporate and investment banking returned to growth in the fourth quarter with a 2% year-on-year increase in net revenues. At year end, BPCE’s CET1 ratio stood at 16.0%.

Our winner in Monaco, CFM Indosuez Wealth Management, will next year celebrate a century of operating in the principality. A subsidiary of Crédit Agricole, CFM Indosuez Wealth held total assets of more than 6 billion, maintains the largest branch network and is the leading local employer in banking. Wealth management provides by far the largest income stream, and CFM opened the first trading room in the principality and the Côte d’Azur. The bank recently introduced its mobile app, My Indosuez, which offers clients continuous tracking of their assets anywhere in the world.

Our Best Bank once again in Belgium, BNP Paribas Fortis, benefited from an increase in retail banking activity during 2020. Loans grew by 3.5%, driven mainly by growth in new mortgages, while deposits rose by 5.3% fueled by a strong increase in individual customer deposits. Operating expenses were down 2.9% on 2019 thanks to effective cost saving measures and ongoing branch network optimization. Customers use of digital tools continued to accelerate, with more than 1.5 million active customers on mobile apps, up 12.2% compared to the fourth quarter 2019 and an average of more than 45 million monthly connections, an improvement of nearly a third compared to the fourth quarter of 2019.

Near the end of last year, BNP Paribas and bpost (the Belgian postal group) announced a new partnership model and this April signed an agreement whereby BNP Paribas Fortis will acquire bpost’s 50% holding in bpost bank to become its sole shareholder. A seven-year partnership was agreed upon, in which bpost will continue to provide a wide range of financial services across its post office network.

Our Best Bank in the Netherlands, ING, grew its primary customer base by 578,000 in 2020 to 13.9 million clients. While the pandemic and lockdowns resulted in a softening of loan demand, which led to a reduction in core lending of €2.5 billion over the year, customer deposits grew by €41.4 billion. ING’s successful digitization strategy led to the number of mobile card payments doubling to 563 million from 232 million in 2019.

CEO Steven van Rijswijk says, “We continue to see a healthy demand for mortgages. We also observed people spending less in lockdown, which resulted in an increase in savings. Considerably more customers are choosing ING as their bank for investment products, which has resulted in healthy growth of fee and commission income. Risk costs, though higher for the full year, dropped 51% in the fourth quarter compared to the year-earlier period, while operational expenses remained under control. Our capital position strengthened further to 15.5%.”

In Luxembourg, this year’s winner, Banque Internationale à Luxembourg (BIL), is the oldest privately owned bank in the Grand Duchy, where it ranks second or third place in market share across all key banking segments. BIL has been majority owned since 2018 by the Chinese investment group Legend Holdings, with the Luxembourg state retaining a 10% stake. Legend Holdings intends to maintain and invest further in the development of the BIL brand in Luxembourg, Europe and internationally. As of end June 2020, BIL’s core operating income was up 6%. Customer deposits increased by 0.7% to €19.1 billion and customer loans were up by 3.3% to €15.2 billion, strengthening the bank’s market shares by 13.5% and 14.5% respectively. The CET1 capital ratio stood at 12.8%.

In its home market of Switzerland, our winner UBS saw profit before tax in personal and corporate banking increase by 4% to Swiss francs 318 million ($345 million) for the fourth quarter of 2020 on the back of a 3% rise in operating income to CHF896 million, reflecting higher transaction-based revenues. For UBS Group as a whole, profit before tax leapt by 47% to more than $8.2 billion, mainly due to a surge in investment banking and fund management activities.

The bank’s new CEO, Ralph Hamers, commented: “Group revenues were up 12%, and we generated a strong return on CET1 capital at 17.6%. We met or exceeded every single one of our growth and returns targets. As significant to me, though, is that every single business division and region played a role in this success. Global Wealth Management and Asset Management recorded double-digit profit before tax growth, while the Investment Bank achieved a 20% return on attributed equity… Our universal bank in Switzerland benefited from a resilient economy, supported by effective government-backed lending programs in partnership with the banks.” At year end the group’s CET1 capital ratio was 13.8%.

During 2020, our repeat winner in Germany, DZ Bank, met its original earnings target of €1.5 billion, with business volumes growing at a faster rate than the overall market in nearly all divisions. DZ Bank also strengthened its capital base so that its CET1 ratio rose above 15% for the first time.

Dr. Cornelius Riese, Co-CEO of DZ Bank, commented that “in spite of all the challenges and uncertainties that the Covid-19 pandemic created for us last year, we achieved a very satisfying profit before taxes that met the target that we had set before the pandemic. In the wake of the dramatic economic downturn in the spring, our target initially looked difficult to achieve. However, our optimism grew over the course of the year in view of our healthy business performance and the positive trend in the capital markets. Once again, therefore, the DZ Bank Group demonstrated its resilience, diversification and earnings power. With a CET1capital ratio of 15.2%, the DZ Bank Group has a healthy capital base and is emerging from the challenges of 2020 with renewed strength.”

In Austria, our winner BAWAG Group once again delivered a solid operating performance. Core revenues increased by 1% to nearly €1.2 million, net interest income rose by 4%, customer loans increased by 5% compared to December 2019, while operating expenses decreased by 6% due to ongoing efficiency measures and at year end the NPL ratio stood at 1.5%. The bank affirmed its goal of maintaining a strong balance sheet and solid capitalization levels and the CET1 ratio was 16.3% prior to any distribution of dividends.

CEO Anas Abuzaakouk commented “Our solid operating performance was a result of having transformed our business over the years and entering into the crisis as one of the most efficient banking platforms. This allowed us to offset Covid-19 related headwinds and generate pre-provision profits of € 653 million.”

Our best bank in Liechtenstein, LGT, is the world’s largest private banking and asset management group owned by a single family, the Princely House of Liechtenstein. It is also the largest bank in Liechtenstein with approximately CHF96 billion assets under administration and more than a thousand employees. Last year saw another strong performance, with net asset inflows up 5% for the year totalling CHF11.6 billion, while assets under management increased 6% to CHF240.7 billion. LGT Group’s total operating income increased 2% to CHF1.85 billion, largely due to higher income from the brokerage business and portfolio management mandates. The bank’s CET1 ratio is a healthy 21.4%.

Despite the considerable economic downturn in Sweden, our winner Handelsbanken put in a good performance in its home market. Operating profits were up 11% for the year and net interest income rose 4% due to increased volumes in both lending and deposits. Net fee and commission income grew by 6% and Handelsbanken received the largest inflow of savings among fund managers in Sweden, with new savings in its mutual funds totaling Swedish krona 34.9 billion ($4.1 billion), giving the bank a market share of 46%.

CEO Carina Åkerström commented, “The bank is delivering on the target of a higher return on equity than the average of its peers and the cost trend in the group shows clear signs of a positive and sustainable trend.” Handelsbanken’s CET1 ratio increased to 20.3%.

OP Financial Group, our best bank in Finland, increased net interest income by 4% while total expenses were down 3%. The Group’s loan portfolio grew by 2% and deposits increased by 11% to €71 billion, while revenue from its important insurance businesses grew by 36% to €572 million.

Over the course of the year, OP Financial Group invested €282 million in business development and improving customer experience. Chief Executive Officer Timo Ritakallio noted “the exceptional year 2020 changed customer behavior. Cash withdrawals decreased by more than 20% from the previous year. The use of OP-mobile and OP Business mobile shows strong growth. In 2020, logins to OP-mobile increased by 34% and those to OP Business mobile by as much as 50%. We are expecting the same trend to continue as well as a further decline in visits to branches.” The Group’s CET1 ratio was 18.9% at the year’s close.

In Denmark our winner Nykredit put in a robust performance with better-than-expected results, assets under management rising by near 10%. As CEO Michael Rasmussen acknowledged: “The full-year results are highly satisfactory and exceed the guidance we provided before the corona crisis outbreak.” Lending was up 9% and net interest, net fee and wealth management income all increased compared with 2019. With 41 customer centres across the country, Nykredit provides 43.6% of all mortgage lending and is Denmark’s largest credit provider with more than one million customers. The CET1 ratio was 20.5% at year end.

DNB, our Best Bank in Norway, ended 2020 with its capital base stronger than ever before, its CET1 ratio rising to 18.7%. CEO Kjerstin Braathen commented that “unlike many other European banks, DNB is emerging strengthened from the pandemic, with healthy growth, good results and a record-high level of customer satisfaction.” The bank saw high levels of customer activity, with growth in loans to personal customers up 2.8% and loans to small and midsize enterprises increasing by 8.3%. Deposits by corporate and personal customers were up 19.5% and 8.1%, respectively, and 97% of all new savings agreements were sold through digital channels.

Arion Bank, our winner in Iceland, put in an exceptional performance during 2020. Total assets increased 8% on the back of strong growth in deposits–up 15% over the year–while loans to customers were up by 6% due to increased mortgage lending. Fourth-quarter results were especially strong, with an increase in core revenues of 8.2% and net earnings from continuing operations up by over 50%, generating a return on equity of 11.8% (compared to a negative 5.8% ROE a year earlier).

CEO Benedikt Gíslason commented: “The bank’s financial results improved substantially between years, in both net earnings and earnings from continuing operations, illustrating that the organizational changes and shifts in focus made at the end of the third quarter of 2019 have had the desired effect.” The bank’s overall capital ratio was 27.0% and its CET1 ratio stood at 22.3% at the end of the year.

Our winner once again in Italy, Intesa SanPaolo established itself as the dominant player in Italy through its acquisition of UBI Banca. During Italy’s Covid-19 crisis the bank provided support to the real economy, granting loans of €77 billion (or €95 billion including recently acquired UBI Banca), of which around €63 billion went to households and SMEs. Intesa SanPaolo also facilitated the return from non-performing to performing status of around 11,500 Italian companies, thereby safeguarding around 57,000 jobs. The bank maintains a strong liquidity position and funding capability, with liquid assets of €243 billion, and a solid capital position, with a CET1 ratio of 15.4% at year end. The bank’s credit quality improved, with NPLs down 34.6% compared to 2019.

CEO Carlo Messina commented: “In 2020 we exceeded our target of achieving a stand-alone net income of €3.1 billion, when excluding the accounting impact of the combination with UBI Banca, the goodwill impairment related to Banca dei Territori, and the five-month contribution from UBI Banca’s activities. Adding the five-month contribution from UBI Banca, the normalized net income reached €3.5 billion.”

Intesa SanPaolo clients benefit from its strong digital offering, with around 10.3 million multichannel customers already signed up (over 12 million, including customers from recently acquired UBI Banca), and around 6.5 million of them are now using the Intesa SanPaolo app.

HSBC, our winner in Malta, consolidated its already strong capital base with the CET1 ratio rising to 18.0% from 16.4% at the end of 2019. The bank’s liquidity position remains solid, with its advances to deposits ratio standing at 62%, and business fundamentals remain good despite broadly flat revenues and declining profits during the pandemic year. Customer deposits and loans were both up, and there was a significant improvement in the cost base due to rigorous cost management and sustainable savings from the restructuring program announced in 2019.

Eurobank, our winner in Greece, supported its clients through the pandemic with new loan disbursements, moratoria and other support measures while turning in a good financial performance. CEO Fokion Karavias commented, “Eurobank is moving forward with a plan to complete the cleanup of the balance sheet and become the first bank in Greece to bring the NPE ratio to single digit, within 2021.”

At the year end, Eurobank’s NPE ratio had come down to 14.0%–currently the lowest in the Greek banking system–while performing loans saw an organic increase of €2.1 billion. Net profits more than doubled to €544 million and deposits grew by €2.4 billion over the year. Operating expenses were cut by 6.0% in Greece (3.6% at group level), the cost to income ratio of 40% being a sharp improvement. The group CET1 ratio stood at 13.9% at year end.

Our winner in Cyprus, Hellenic Bank also weathered a difficult year well from a strong capital position, with a CAR of 22.5% and ample liquidity, the bank’s liquidity coverage ratio standing at 454%, with Cypriot deposits accounting for 85% of the total, while the ratio of net loans to deposits was a healthy 42.5%. The bank generated a €40 million net profit during the first nine months of 2020 despite impairment losses remaining high. Both organic and non-organic efforts to resolve NPEs continue, with the bank’s NPE-to-total assets ratio hovering around at 3%, while a CET1 ratio of 20.1% reflects adequate capital buffers.

Our Best Bank in the United Kingdom is Barclays which benefited from its diversified income streams, especially investment banking, enabling it to increase group income to £21.8 billion.

Corporate and investment banking turned in a stellar performance, gaining market share amid buoyant trading conditions to deliver a £12.5 billion contribution, an improvement of 22% over the previous year. The UK bank faced economic headwinds arising from both Covid-19 and Brexit, resulting in a 14% decline in income to £6.3 billion, while Barclays’ credit cards and payments reported a 22% drop due to lower credit card balances and reduced payments activity.

In response to the pandemic Barclays extended more than 680,000 payment holidays and some £27 billion in support of UK businesses. “Throughout the pandemic we focussed on preserving the financial and operational integrity of the firm so that we can maximise our support for clients and customers, for colleagues, and for the communities in which we live and work,” says CEO Jes Staley.

Barclays increased its provisions against credit impairment to £4.8 billion, nearly half of which is reserved for anticipated future customer stress, thereby raising its NPL coverage ratios across portfolios. Pandemic-related costs nudged the cost/income ratio up one percentage point to 64% while retained profits helped strengthen the Bank’s capital base, its Tier 1 capital ratio rising by 130 bps to 15.1% at the year end.

The Republic of Ireland has been harder hit by Brexit than any other EU member country, and the combined impacts of this and Covid-19 led to a sharp downturn in economic activity. Our winner, Allied Irish Banks (AIB), weathered the storm better than its competitors, with operating profits down from €1.1 billion to €729 million before prudent provisioning of nearly €1.5 billion caused the bank to report a substantial net loss.

Commenting on the results, CEO Colin Hunt says that “the fundamentals of our business remain robust, sustainable and strong. We entered this crisis in a position of capital strength which, enabled by our leading digital technology, allowed us to deliver unprecedented levels of support to our customers, communities and the economy when it mattered most.”

Deposits grew by 14% over the year as new lending fell by 27%, mainly due to lower volumes of mortgages. AIB maintained strong liquidity ratios, and at the year end its CET1 capital adequacy ratio stood at 15.6%.