Markets are known to be risky, but what if you could design insurance that would protect against losses?

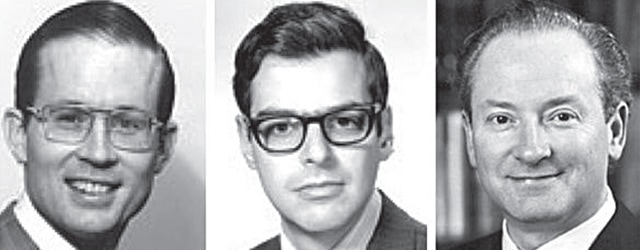

That’s the problem Robert Merton, Myron Scholes and the late Fisher Black solved by developing the Black-Scholes model, which provides investors with a recipe for manufacturing insurance on any security. The model prices stock options and provides information about how to hedge effectively. The underlying methodology won Myron Scholes and Robert Merton the Nobel Memorial Prize in Economic Sciences in 1997, with the late Fisher Black posthumously mentioned by the Nobel committee.

Black, Merton and Scholes, who started their work in the late 1960s, didn’t work as a threesome, but were very collaborative and slightly competitive with each other. Black and Scholes published their paper jointly in 1973, as did Merton separately. That year, the US entered a recession, with double-digit inflation and interest rates. The stock market fell 50% in real terms from mid-1973 to 1974.

Also that year, the Chicago Board of Trade established the Chicago Board Options Exchange (CBOE), making options, previously traded over the counter between firms, into an exchange-traded product with guarantees and standardized contracts. The new exchange—alongside the spread of computers—transformed the options business. Traders could now price options in real time, and the number of call option contracts that changed hands at the CBOE went from 911 on opening day in 1973 to more than 20,000 by mid-1974 to 100,000 in 1977, wrote Peter Bernstein in Capital Ideas: The Improbable Origins of Modern Wall Street.

“On the academic side, you’ve got a new model; and in the real world, you have a real exchange for pricing them,” says Stephen Figlewski, professor of finance at the Stern School of Business at New York University. “What the model really gives us is it tells us how to hedge and manage the risk of options.”

What exactly does this model do? The Black-Scholes formula calculates the number of options needed to offset price movements in a stock and the associated cost to make the option. “It’s not what people can trade at, but what it costs to make; and that’s useful information when judging a price,” says Robert Merton, now distinguished professor of finance at the MIT Sloan School of Management. Changes in price require active management to maintain the hedge. “It’s called dynamic pricing, and that’s what makes options pricing complex,” Merton explains. “We worked out how to change that risk.”

Algorithmic trading got another boost in 2001 when US markets shifted from fractions to decimals, which created smaller gaps between bid and offer prices. The underlying methodology used in the Black-Scholes model has been applied to a wide swathe of financial securities and now, turbocharged by increasing computing power, mathematical formulae drive stock markets as never before. In the early 2000s, for example, David X. Li, then at J.P. Morgan, developed application of Gaussian copula models for pricing collateralized debt obligations. In the aftermath of the 2008 financial crisis, some observers blamed him for “killing Wall Street,” even though Li himself was ringing alarm bells as early as 2005.